The objective of IAS 19 is to prescribe the accounting and disclosure for ’employee benefits’.

IAS 19 requires an entity to recognize:

- A Liability when an employee has provided service in exchange for employee benefits to be paid in the future; and

- An Expense when the entity consumes the economic benefit arising from a service provided by an employee in exchange for employee benefits.

International Accounting Standard

IAS 19 – Employee Benefits

A definitive reference for accountants, finance professionals, and IFRS practitioners on recognition, measurement, presentation, and disclosure of all employee benefits under IAS 19.

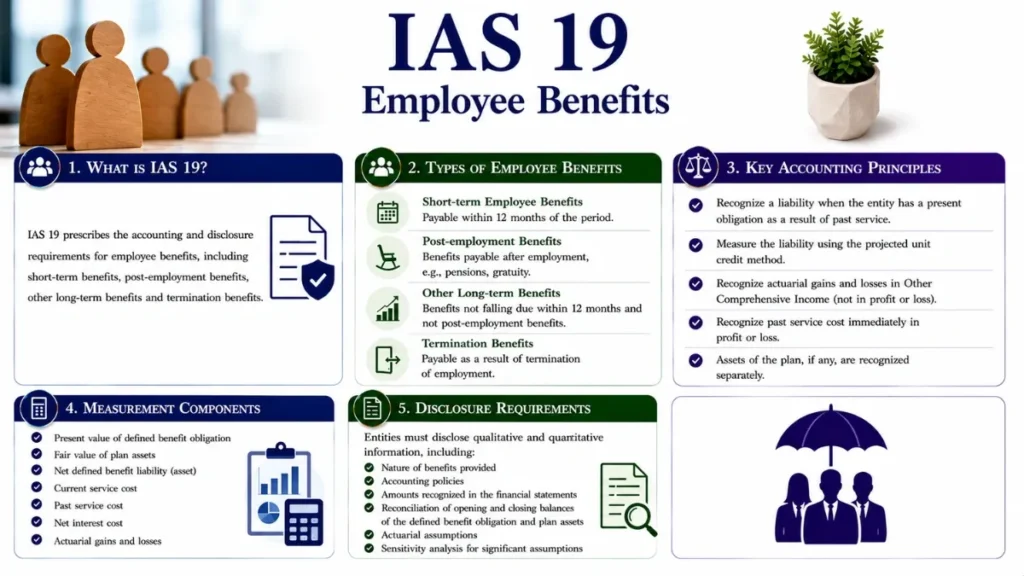

What Is IAS 19? (Objective and Scope)

IAS 19 Employee Benefits is the International Accounting Standard issued by the International Accounting Standards Board (IASB) that prescribes how entities account for and disclose obligations arising from employment relationships. It applies to all employee benefits, whether provided through formal plans, legal obligations, or constructive obligations arising from established custom.

The standard covers all forms of consideration given by an entity in exchange for services rendered by employees or for the termination of employment. This broad scope captures cash compensation, non-cash perquisites, retirement pensions, post-employment healthcare, long-service leave, and redundancy payments alike.

Scope Exclusion

IAS 19 does not apply to share-based payment transactions within the scope of IFRS 2 Share-based Payment, nor to employee benefit plans accounted for under IAS 26 Accounting and Reporting by Retirement Benefit Plans.

The standard applies to all entities reporting under International Financial Reporting Standards (IFRS). It distinguishes sharply between obligations whose ultimate cost can be determined with certainty at the time of contribution (defined contribution) and those that depend on future variables such as salary growth, inflation, and employee longevity (defined benefit).

Four Categories of Employee Benefits Under IAS 19

IAS 19 organises all employee benefits into four distinct categories, each with its own recognition and measurement model. Understanding which category applies is the first and most consequential step in IAS 19 compliance.

| Category | Examples | Key Measurement Basis |

|---|---|---|

| Short-Term Employee Benefits | Wages, paid leave, bonuses, non-monetary benefits | Undiscounted amount expected to be paid |

| Post-Employment Benefits | Pensions, gratuities, post-retirement healthcare | DC: contribution paid; DB: Projected Unit Credit |

| Other Long-Term Employee Benefits | Long-service leave, disability benefits, profit-sharing settled >12 months | Net defined benefit liability/asset (simplified) |

| Termination Benefits | Redundancy pay, early-retirement packages | Undiscounted (or discounted if >12 months after reporting date) |

- Employee

- Includes full-time, part-time, permanent, casual, and agency-supplied workers; does not require a formal employment contract.

- Constructive Obligation

- An obligation arising from established practice, published policy, or a sufficiently specific past pattern of behaviour that creates a valid expectation.

- Vested Benefits

- Benefits that are not conditional on future employment; they have been earned and cannot be forfeited even if the employee leaves.

- Actuarial Gains & Losses

- Changes in the present value of the defined benefit obligation arising from differences between previous actuarial assumptions and actual outcomes.

Short-Term Employee Benefits

Short-term employee benefits are those expected to be settled in full within twelve months after the end of the annual reporting period in which the employees render the related service. Because settlement is imminent, IAS 19 requires no discounting i.e. the simplest measurement basis in the standard.

Recognition Principle

An entity recognises the undiscounted amount of short-term employee benefits expected to be paid in exchange for services rendered as a liability (accrued expense) after deducting any amounts already paid, and as an expense unless another IFRS standard permits or requires its inclusion in the cost of an asset (e.g. IAS 2 Inventories, IAS 16 Property, Plant and Equipment).

Short-Term Compensated Absences

IAS 19 distinguishes between two types of compensated absences, and their accrual treatment differs accordingly:

- Accumulating absences such as annual leave that can be carried forward are accrued as the employee renders service that increases entitlement.

- Non-accumulating absences such as maternity leave or sick leave that lapses if not used are recognised only when the absence occurs.

Profit-Sharing and Bonus Plans

An entity recognises the expected cost of profit-sharing and bonus payments when, and only when, it has a present legal or constructive obligation to make such payments and a reliable estimate can be made. A past practice of paying bonuses may create a constructive obligation even in the absence of a formal plan.

Post-Employment Benefits

Post-employment benefits are formal or informal arrangements under which an entity provides benefits after employment has ended. They represent the most complex and financially significant category under IAS 19. The standard divides all post-employment arrangements into two fundamentally different plan types.

| Feature | Defined Contribution Plans (DC) | Defined Benefit Plans (DB) |

|---|---|---|

| Entity’s obligation | Limited to agreed contributions | To provide the agreed benefits |

| Risk borne by | Employee (actuarial + investment) | Entity (actuarial + investment) |

| Balance sheet liability | Contribution due but unpaid only | Net present value of unfunded obligation |

| P&L charge | Contribution due for the period | Service cost + net interest |

| OCI component | None | Remeasurements (actuarial gains/losses) |

| Actuarial complexity | None required | Annual actuarial valuation typically required |

Defined Contribution Plans: Accounting

Accounting for a defined contribution plan is straightforward: the entity recognises as an expense the contribution payable for the period. If contributions are not expected to be settled wholly within twelve months, they are discounted to present value. No balance sheet liability arises beyond contributions that are due but unpaid.

“The entity’s obligation in a defined contribution plan is limited to the amount it agrees to contribute to the fund. The amount of post-employment benefits received by the employee is determined by the amount of contributions paid by the entity and the investment returns arising from those contributions.” — IAS 19 Basis for Conclusions, IASB

Defined Benefit Plans: Accounting

Defined benefit plans are the most complex area of IAS 19 and often the source of the most material liabilities on an entity’s balance sheet. Unlike defined contribution plans, the entity retains the actuarial risk (that benefits will cost more than expected) and the investment risk (that assets set aside will be insufficient to fund benefits).

The Projected Unit Credit (PUC) Method

IAS 19 mandates the use of the Projected Unit Credit method to determine the present value of the defined benefit obligation (DBO) and the related current service cost. The method attributes benefit entitlement to each period of employee service, treating each period as giving rise to one additional unit of benefit entitlement, and measures each unit separately.

Project future benefits: Estimate the benefits that employees will have earned by retirement, using assumptions about future salary growth, employee turnover, mortality, and inflation.

Attribute benefits to service: Under the plan’s benefit formula, allocate a unit of benefit to each year of past and current service. If a plan provides materially higher benefits in later years, the attribution is adjusted accordingly.

Discount to present value: Apply the discount rate (high-quality corporate bond yield) to calculate the present value of all projected benefit units.

Determine net position: Deduct the fair value of any plan assets from the present value of the DBO to arrive at the net defined benefit liability (or asset).

Test asset ceiling: If a net defined benefit asset arises, apply the asset ceiling, the surplus is limited to the present value of future economic benefits available as refunds or reductions in future contributions.

Asset Ceiling – IFRIC 14

Where a plan is in surplus, IFRIC 14 governs the limit on the recognised net defined benefit asset. The asset is capped at the present value of economic benefits available to the entity through refunds from the plan or reductions in future contributions. Entities must carefully assess the legal or regulatory framework governing their plans to determine whether a right to a refund or reduced contributions exists.

Actuarial Assumptions Under IAS 19

The present value of a defined benefit obligation is highly sensitive to the assumptions embedded within the actuarial model. IAS 19 requires that all actuarial assumptions be unbiased and mutually compatible. They must reflect the best estimate of the variables that will determine the ultimate cost of the benefit.

Financial Assumptions

Financial assumptions reflect economic conditions at the balance sheet date and include:

Discount Rate

The discount rate is arguably the single most influential actuarial assumption. IAS 19 paragraph 83 requires it to be determined by reference to market yields at the end of the reporting period on high-quality corporate bonds. In countries where no deep market for such bonds exists (common in emerging markets), the market yield on government bonds is used instead. The currency and term of the bonds must be consistent with the currency and estimated term of the obligation.

Expected Future Salary Increases

Salaries must be projected to the estimated date of payment. The assumption should reflect future salary levels, incorporating inflation, seniority progression, and any contractual agreements. Because pensions are often salary-linked, even modest changes in the salary growth assumption can significantly affect the DBO.

Inflation

Where benefits are indexed to inflation (e.g. CPI-linked pensions), the future inflation rate is a key input. Consistency with the discount rate is essential: if the discount rate is derived from nominal bond yields, the inflation assumption embedded within it must be consistent with the price inflation assumption.

Demographic Assumptions

Demographic assumptions relate to the future characteristics of employees and former employees. They include:

- Mortality both pre-retirement and post-retirement mortality (longevity). Entities typically use national or industry mortality tables, adjusted for entity-specific experience where significant.

- Employee turnover / withdrawal rates the probability that employees leave before retirement and forfeit unvested benefits.

- Disability rates where ill-health retirement or disability benefits are provided.

- Retirement age the assumed date on which employees will draw their benefits, which may differ from the contractual normal retirement date.

- Medical cost trend rates for post-employment medical plans, the rate of increase in healthcare costs.

Plan Assets Under IAS 19

Plan assets are assets held by a long-term employee benefit fund, or qualifying insurance policies, that meet the criteria for offset against the defined benefit obligation. Their measurement and the determination of what qualifies as a plan asset is strictly defined in IAS 19 to prevent off-balance-sheet manipulation of the net position.

Qualifying Criteria for Plan Assets

An asset qualifies as a plan asset only if it is held by an entity (the fund) that:

- Is legally separate from the reporting entity;

- Exists solely to pay or fund employee benefits;

- Is not available to the reporting entity’s own creditors (even in bankruptcy); and

- Cannot be returned to the reporting entity except when the fund assets exceed the obligations, or to reimburse already-paid benefits.

Measurement of Plan Assets

Plan assets are measured at fair value at the end of each reporting period. Fair value is typically the market price for quoted securities. For unquoted assets, fair value is estimated using appropriate valuation techniques, consistent with IFRS 13 Fair Value Measurement.

Expected Return on Plan Assets

Under the revised IAS 19 (effective 2013), the concept of an “expected return on plan assets” was abolished. Instead, the return on plan assets included in net interest is calculated using the same discount rate applied to the defined benefit obligation. Any actual return above or below this notional amount is treated as a remeasurement recognised in OCI.

Recognition in Profit or Loss and OCI

IAS 19 adopts a clean three-component presentation for defined benefit costs, segregating income statement charges from equity-level remeasurements. This architecture, introduced in the 2011 revision eliminates the corridor method and ensures full and immediate recognition.

| Component | Recognised In | Description |

|---|---|---|

| Current Service Cost | Profit or Loss | Increase in the present value of the DBO resulting from employee service in the current period. |

| Past Service Cost | Profit or Loss (immediately) | Change in DBO for employee service in prior periods resulting from plan amendment or curtailment. No longer deferred. |

| Net Interest | Profit or Loss | Unwinding of the discount on the net defined benefit liability (or asset): DBO × discount rate less plan assets × discount rate. |

| Remeasurements | Other Comprehensive Income | Actuarial gains/losses on DBO; return on plan assets excluding net interest; changes in asset ceiling effect. Never recycled to P&L. |

Elimination of the Corridor Method

Prior to the 2013 revision, IAS 19 permitted the “corridor method”, a smoothing mechanism that allowed actuarial gains and losses to be deferred and amortised over the expected average remaining working lives of employees. The IASB eliminated this option entirely. All actuarial gains and losses are now recognised in OCI immediately, improving transparency and comparability.

Curtailments and Settlements

A curtailment occurs when an entity significantly reduces the number of employees covered by a plan. A settlement occurs when an entity eliminates all further legal or constructive obligation for part or all of the benefits. Both are recognised immediately in profit or loss when they occur, and any related unrecognised past service cost is recognised at the same time.

Other Long-Term Employee Benefits

Other long-term employee benefits are those not expected to be settled wholly within twelve months after the end of the reporting period in which employees render the related service, and which do not arise from post-employment or termination arrangements. Common examples include long-service leave (sabbaticals), jubilee payments, long-term disability benefits, and profit-sharing plans settled beyond twelve months.

The accounting model for other long-term benefits is essentially a simplified version of the defined benefit model: the entity recognises a net defined benefit liability and measures it using the projected unit credit method. However, unlike for post-employment defined benefit plans, all changes including what would otherwise be remeasurements are recognised in profit or loss. There is no OCI component for other long-term benefits.

The IASB justified this simplified treatment on the grounds that, for these benefits, measurement uncertainty is typically lower, and the amounts involved are generally less material than for pensions.

Termination Benefits

Termination benefits are employee benefits provided in exchange for the termination of an employee’s employment, whether as a result of an entity’s decision to terminate employment before the normal retirement date, or an employee’s decision to accept an offer of benefits in exchange for termination.

Recognition

An entity recognises a liability and expense for termination benefits at the earlier of:

When the entity can no longer withdraw the offer of those benefits, which occurs when the entity has communicated to affected employees a termination plan meeting specific criteria; or

When the entity recognises costs for a restructuring within the scope of IAS 37 Provisions, Contingent Liabilities and Contingent Assets that involves the payment of termination benefits.

Measurement

Termination benefits expected to be settled wholly before twelve months after the balance sheet date are measured at their undiscounted amount. Benefits expected to be settled after twelve months are discounted to present value using the same discount rate as for defined benefit obligations.

Distinction from Short-Term Benefits

Termination benefits arise from the decision to terminate employment, not from services rendered. This distinguishes them categorically from all other IAS 19 benefits and determines both the timing of recognition and the measurement approach.

Disclosure Requirements

IAS 19 imposes extensive disclosure requirements, designed to help users of financial statements understand the nature, financial effect, and risks of defined benefit plans. Disclosures are primarily required for post-employment benefit plans, with abbreviated requirements for other categories.

Characteristics and Risks of Defined Benefit Plans

Entities must disclose qualitative and quantitative information about:

- The nature of the benefits provided and the regulatory framework governing the plan;

- The risks to which the plan exposes the entity, including unusual or entity-specific risks;

- Information about plan amendments, curtailments, and settlements;

- Multi-employer plan disclosures if applicable, including details of any deficit and planned contribution changes.

Amounts in the Financial Statements

Required quantitative disclosures include a reconciliation of the opening and closing balances of the:

- Net defined benefit liability (or asset);

- Present value of the defined benefit obligation;

- Fair value of plan assets;

- Effect of the asset ceiling.

Actuarial Assumptions and Sensitivity Analysis

Entities must disclose each significant actuarial assumption, expressed as an absolute value rather than a range. Crucially, a sensitivity analysis is required for each significant actuarial assumption as at the end of the reporting period, showing how the defined benefit obligation would have been affected by changes in the relevant actuarial assumption that were reasonably possible at that date. The sensitivity analysis must be based on the same method used to calculate the defined benefit liability.

Funding and Future Cash Flows

Disclosures about future cash flows include: a description of any funding arrangements and funding policy; the expected contributions to the plan for the next annual reporting period; and a maturity profile of the defined benefit obligation, showing the weighted average duration of the obligation and the amount of benefits expected to be paid in each of the next five years and then in the aggregate thereafter.

IAS 19 Amendments and Revisions

| Date | Amendment / Event | Key Change |

|---|---|---|

| 1998 | Original IAS 19 revised | Major overhaul; introduced corridor method option. |

| 2004 | IAS 19 Amendment | Introduced option to recognise actuarial gains/losses immediately in OCI (the “SORIE” option). |

| June 2011 | IAS 19 (Revised 2011) | Eliminated corridor method; mandated immediate OCI recognition; replaced expected return on assets with net interest concept. |

| 1 Jan 2013 | Effective Date (Revised) | Revised IAS 19 mandatory for periods beginning on or after this date. |

| Nov 2013 | Defined Benefit Plans: Employee Contributions (Amendments) | Simplified accounting for voluntary employee or third-party contributions to DB plans. |

| Feb 2018 | Plan Amendment, Curtailment or Settlement (Amendments) | Clarified how to determine current service cost and net interest when a plan amendment, curtailment, or settlement occurs during the reporting period. |

Frequently Asked Questions

What is the primary objective of IAS 19?

The objective of IAS 19 is to prescribe the accounting and disclosure requirements for employee benefits. It requires an entity to recognise a liability when an employee has provided service in exchange for benefits to be paid in the future, and an expense when the entity consumes the economic benefit arising from service provided by an employee.

How is the discount rate determined under IAS 19?

The discount rate is determined by reference to market yields at the end of the reporting period on high-quality corporate bonds. In countries where there is no deep market in such bonds, the market yields on government bonds are used instead. The currency and term of the bonds must be consistent with the currency and estimated term of the post-employment benefit obligation.

Can actuarial gains and losses be recycled from OCI to profit or loss?

No. Under the revised IAS 19 (effective 2013), remeasurements which include actuarial gains and losses on the defined benefit obligation and the return on plan assets excluding net interest are recognised in Other Comprehensive Income (OCI) and are permanently excluded from profit or loss. They are never subsequently reclassified to profit or loss (i.e. no recycling). This is a mandatory treatment; there is no accounting policy choice.

Is a sensitivity analysis required for all actuarial assumptions?

IAS 19 requires a sensitivity analysis for each significant actuarial assumption as at the end of the reporting period. Whether an assumption is “significant” requires judgement, but typically the discount rate, salary growth rate, and life expectancy (mortality) are always considered significant for pension plans. The sensitivity analysis must show the impact of reasonably possible changes in each assumption on the defined benefit obligation.

When are past service costs recognised under IAS 19?

Under the revised IAS 19, past service costs whether arising from vested or unvested benefits are recognised immediately in profit or loss. The old rule requiring unvested past service costs to be amortised over the vesting period has been abolished. The recognition date is the earlier of: the date of the plan amendment or curtailment, and the date the entity recognises related restructuring costs or termination benefits.

How does IAS 19 apply to multi-employer defined benefit plans?

Where an entity participates in a multi-employer defined benefit plan, it should account for its proportionate share of the defined benefit obligation, plan assets, and costs associated with the plan in the same way as for any other defined benefit plan. However, if sufficient information is not available to apply defined benefit accounting, the entity may account for the plan as if it were a defined contribution plan and provide additional disclosures about the nature of the plan and why defined benefit accounting is not possible.

(Qualified) Chartered Accountant – ICAP

Master of Commerce – HEC, Pakistan

Bachelor of Accounting (Honours) – AeU, Malaysia