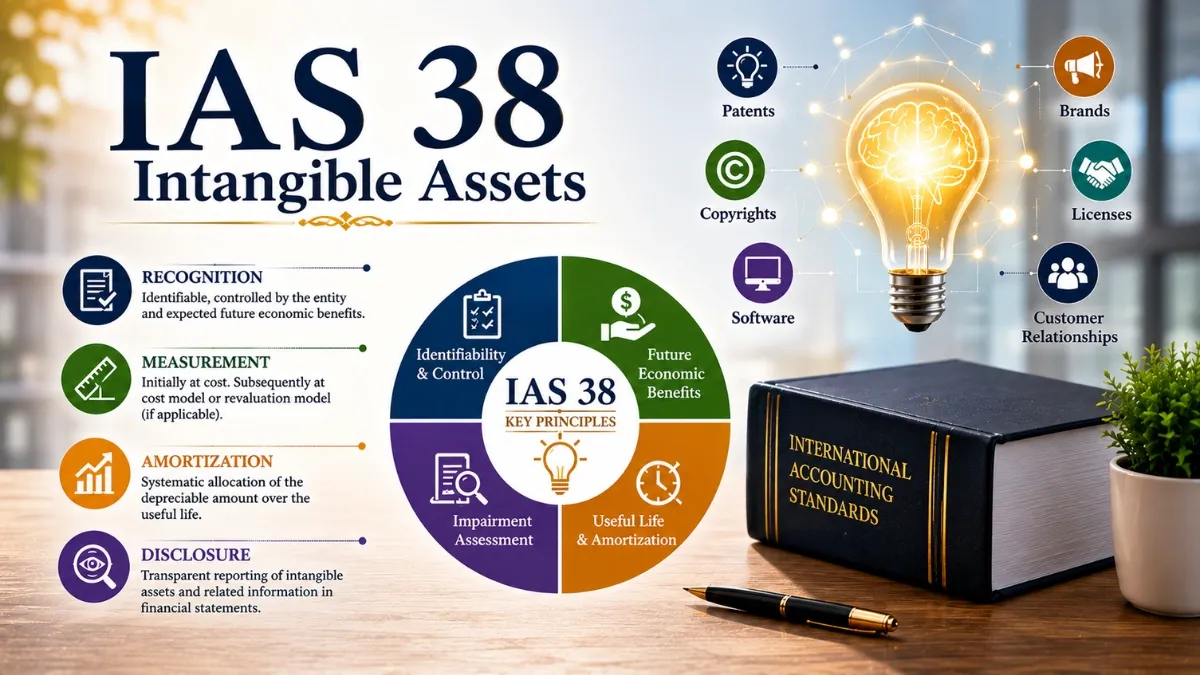

IAS 38 – Intangible Assets

IAS 38 explains the ‘accounting criteria‘ for intangible assets, which are non-monetary assets that are without physical substance and identifiable (either being separable or arising from contractual or other legal rights). IASB · IAS 38 · Intangible Assets CA Jhanzayb (ACA) Qualified Chartered Accountant · IFRS Specialist IAS 38 – Intangible … Read More