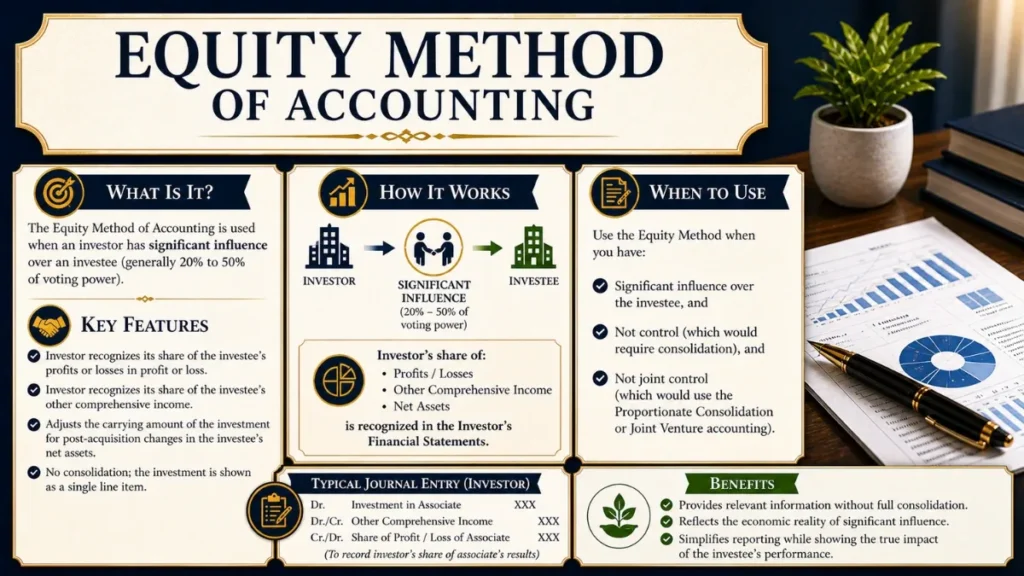

Equity method of accounting is used when the parent company owns between 20% and 50% of the outstanding shares of the entity (i.e. Associate). It is an accounting technique to consolidate financial statements of companies where one company has significant influence over another company.

Equity method allows the parent company to include the earnings and assets of the entity (i.e. Associate) in their consolidated financial statements as a ‘single entity’.

Equity Method of Accounting

A complete, authoritative guide to recognizing, measuring, and reporting equity method investments, covering US GAAP (ASC 323) and IFRS (IAS 28).

01What Is the Equity Method of Accounting?

The equity method is an accounting technique used by a company to record its proportionate share of another company’s net assets and earnings when it holds a significant, but non-controlling ownership stake.

Under the equity method of accounting, an investor recognizes its initial investment at cost, then adjusts the carrying value each period to reflect its proportionate share of the investee’s profits, losses, dividends, and other comprehensive income items.

Rather than simply recording dividends received as income (as under the cost method), the equity method treats the investor and investee as economically intertwined. When the investee earns profits, the investor’s balance sheet grows accordingly. When the investee pays dividends, the investor’s carrying value decreases, because cash has flowed out of the investee entity.

The equity method is the bridge between pure cost-basis accounting and full consolidation: it is required whenever an investor can exert significant influence over an investee but does not control it outright.

02When Is the Equity Method Required? (20%–50% Rule Explained)

The cornerstone concept is significant influence, the power to participate in the financial and operating policy decisions of an investee without controlling those decisions. Both US GAAP (ASC 323) and IFRS (IAS 28) use this concept of significant influence as the trigger.

A holding of 20%–50% of voting shares creates a rebuttable presumption of significant influence. Below 20% generally implies no significant influence; above 50% typically triggers consolidation.

Indicators of Significant Influence

The 20–50% threshold is not absolute. The following qualitative factors can confirm or rebut it:

Board Representation

The investor holds a seat on the investee’s board of directors or equivalent governing body.

Policy Participation

The investor participates in policy-making processes, including dividend and compensation decisions.

Material Transactions

Significant intercompany transactions exist between the investor and investee.

Interchange of Personnel

Managerial personnel are shared or exchanged between the two entities.

Essential Technology

The investor provides key technical information or proprietary technology to the investee.

Blocking Rights

The investor can veto significant financial or operating decisions even without majority votes.

The equity method is not applied to investments in consolidated subsidiaries (>50% ownership), investments held-for-sale under IFRS 5/ASC 360, interests in variable interest entities where consolidation is required, or when the investor loses significant influence.

03How the Equity Method of Accounting Works (Step-by-Step)

An equity method investment is initially recognized at cost, the total consideration paid, including transaction costs under US GAAP (transaction costs are expensed under IFRS).

Purchase Price Allocation

At acquisition, the investor must allocate any excess of cost over the proportionate share of the investee’s net book value to underlying assets and liabilities using a concept analogous to a purchase price allocation in a business combination:

Identify the Net Book Value

Calculate the investor’s percentage share of the investee’s recorded net assets at the acquisition date.

Allocate Excess to Identifiable Assets/Liabilities

Any cost over net book value is attributed first to identifiable assets and liabilities based on fair value differences (e.g., undervalued inventory, PP&E under IAS 16, intangibles as per IAS 38).

Attribute Remainder to Equity Method Goodwill

The residual excess is recognized as equity method goodwill, embedded in the investment carrying amount. It is not amortized under US GAAP but tested for impairment.

Recognize a Bargain Purchase Gain

If cost is below the proportionate fair value of net assets, a gain may be recognized in income in the period of acquisition.

04Journal Entries Under the Equity Method

Four recurring categories of entries drive equity method accounting throughout the life of the investment:

| Account | Dr / Cr | Amount |

|---|---|---|

| Investment in Associate | Dr | XXX |

| Cash / Payable | Cr | XXX |

| Account | Dr / Cr | Amount |

|---|---|---|

| Investment in Associate | Dr | XXX |

| Equity in Earnings of Associate (P&L) | Cr | XXX |

| Account | Dr / Cr | Amount |

|---|---|---|

| Cash / Dividend Receivable | Dr | XXX |

| Investment in Associate | Cr | XXX |

Dividends represent a return of capital from the investee, not a return on capital. Since income recognition has already occurred via Entry 2, recognizing dividends as income again would be double-counting. The carrying value therefore decreases when cash leaves the investee.

| Account | Dr / Cr | Amount |

|---|---|---|

| Equity in Losses of Associate (P&L) | Dr | XXX |

| Investment in Associate | Cr | XXX |

The investor stops recognizing losses once the carrying value reaches zero, unless the investor has guaranteed obligations or committed to provide further financial support. Any excess losses are tracked off-balance-sheet and resume when the investee returns to profitability.

05US GAAP vs IFRS Equity Method (ASC 323 vs IAS 28)

While both frameworks converge on the fundamental equity method mechanics, several important differences exist between ASC 323 (US GAAP) and IAS 28 (IFRS).

| Aspect | 🇺🇸 US GAAP (ASC 323) | 🌐 IFRS (IAS 28) |

|---|---|---|

| Threshold | 20–50% presumed significant influence | 20–50% presumed significant influence |

| Transaction Costs | Capitalized into investment cost | Expensed as incurred |

| Equity Method Goodwill | Embedded; not separately amortized; tested for impairment at investment level | Embedded; not separately tested; part of overall investment impairment test |

| Impairment Test | Other-than-temporary impairment (OTTI) model; fair value vs. carrying amount | IAS 36 single-step recoverable amount test (higher of FVLCD and VIU) |

| Reporting Lag | Up to 3-month lag permitted if investee’s financial statements are unavailable | Up to 3-month lag permitted |

| Intragroup Profit Elimination | Eliminate only investor’s proportionate share of upstream/downstream profits | Same – eliminate investor’s proportionate share |

| Fair Value Option | Available for eligible equity method investments (ASC 825) | Available for venture capital organizations and similar entities |

| Discontinuing the Method | Cease when significant influence is lost; retain carrying amount as new cost basis | Same treatment under IAS 28 |

06Impairment of Equity Method Investments

An equity method investment must be assessed for impairment whenever events or circumstances indicate that the carrying amount may not be recoverable.

Under US GAAP (Other-Than-Temporary Impairment)

ASC 323 requires an assessment of whether any decline in fair value below the carrying amount is other-than-temporary. Relevant factors include:

How far below cost is the fair value, and for how long?

Recurring losses, near-insolvency, or credit-rating downgrades.

Can the investor hold long enough to allow recovery of the unrealized loss?

Broad market declines versus investee-specific deterioration.

If impairment is other-than-temporary, the investment is written down to fair value, creating a new cost basis. The write-down is not reversible under US GAAP.

Under IFRS (IAS 36 Recoverable Amount)

IFRS uses a single-step test: compare the carrying amount to the recoverable amount, which is the higher of:

Fair Value Less Costs of Disposal (FVLCD) – the price obtainable in an arm’s-length transaction, minus disposal costs.

Value in Use (VIU) – the present value of future cash flows expected from continued use and ultimate disposal.

Unlike US GAAP, IFRS allows impairment reversals in subsequent periods if the recoverable amount increases, up to the previously impaired carrying amount.

07Equity Method of Accounting Example (With Calculations)

Investor Corp acquires a 30% stake in Associate Ltd.

Step 1 – Calculate Goodwill on Acquisition

| Purchase price | $5,000,000 | |

| Investor’s share of Associate’s net assets (30% × $3,000,000) | Less | ($900,000) |

| Equity Method Goodwill (embedded in investment) | $4,100,000 |

Step 2 – Year-End Adjustments

| Account | Dr / Cr | Amount |

|---|---|---|

| Investment in Associate Ltd. | Dr | $360,000 |

| Equity in Earnings of Associate (Income) | Cr | $360,000 |

| Account | Dr / Cr | Amount |

|---|---|---|

| Cash | Dr | $120,000 |

| Investment in Associate Ltd. | Cr | $120,000 |

| Opening carrying value | $5,000,000 | |

| + Share of net income (Entry A) | +$360,000 | |

| − Dividends received (Entry B) | −$120,000 | |

| Closing carrying value | $5,240,000 |

08Key Terms & Concepts in Equity Method

The power to participate in, but not control an investee’s financial and operating decisions.

An entity over which the investor has significant influence. The terms are used interchangeably in IFRS and US GAAP respectively.

The excess of acquisition cost over the proportionate fair value of the investee’s net identifiable assets; embedded within the investment carrying amount.

The balance sheet value of the investment, starting at cost and adjusted for the investor’s share of income, losses, and dividends.

A transaction where the investee sells assets to the investor; unrealized profit is eliminated from the investment balance.

A transaction where the investor sells assets to the investee; unrealized profit in the investor’s books is eliminated proportionally.

The investor also picks up its share of the investee’s other comprehensive income items, such as foreign currency translation and pension adjustments.

An irrevocable election to measure eligible equity method investments at fair value through earnings, available under both ASC 825 and IAS 28.

09Frequently Asked Questions

What happens when the investor’s ownership drops below 20%?

Can a company use the equity method for less than 20% ownership?

How does the equity method affect cash flow statements?

What is the difference between the equity method and consolidation?

Is equity method goodwill amortized?

Where is the equity method investment shown on the balance sheet?

Equity Method of Accounting – Key Takeaways

- The equity method applies when an investor holds 20–50% of voting shares and exerts significant influence over an investee.

- The investment is initially recorded at cost; thereafter adjusted for the investor’s proportionate share of income, losses, and dividends.

- Dividends reduce the carrying amount; they are a return of capital, not income, under this method.

- Losses reduce the carrying value to zero; further losses are suspended unless the investor has committed additional support.

- US GAAP (ASC 323) and IFRS (IAS 28) are broadly similar but differ on transaction cost capitalization, impairment models, and reversal of impairments.

- Equity method goodwill is not amortized but is embedded in the investment and subject to impairment testing.

- When significant influence is lost, the retained investment is remeasured to fair value and the equity method is discontinued.

(Qualified) Chartered Accountant – ICAP

Master of Commerce – HEC, Pakistan

Bachelor of Accounting (Honours) – AeU, Malaysia