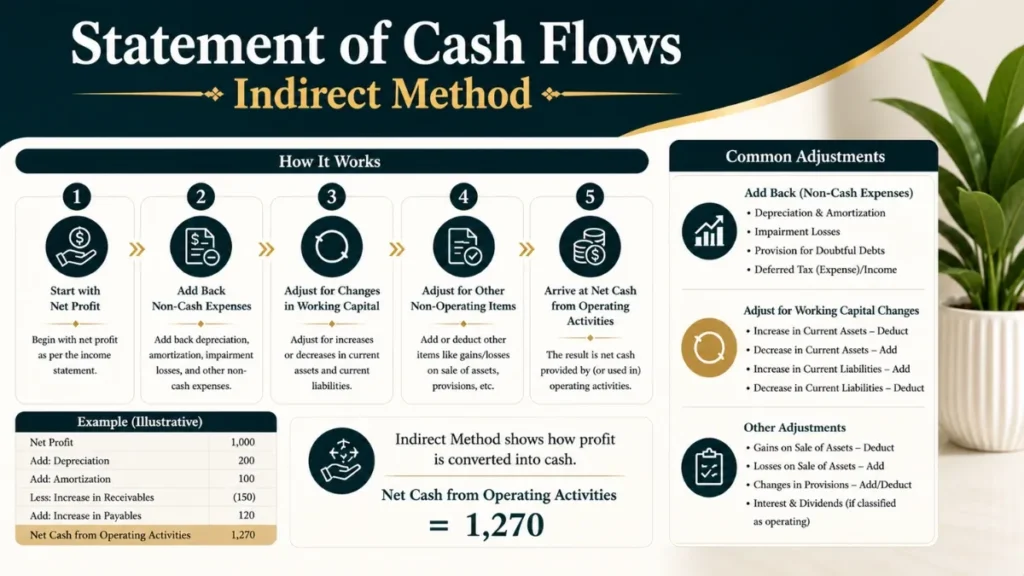

The statement of cash flows indirect method presents the SOCF beginning with net income or loss, with subsequent additions to or deductions from that amount for non-cash revenue and expense items, resulting in cash flow from operating activities.

International Accounting Standard (IAS 7) states that SOCF is a vital ‘financial statement‘ that provides insights into a company’s cash flows from operating, investing, and financing activities during a specific period. It highlights the sources and uses of cash, enabling investors, creditors, and other stakeholders to assess a company’s liquidity and financial health.

The Statement of Cash Flows using the Indirect Method reconciles a company’s net income to its net cash provided by operating activities by adjusting for non-cash items and changes in working capital. SOCF Indirect Method is the most widely used presentation format under both GAAP (ASC 230) and IFRS (IAS 7 – Statement of Cash Flows).

01 What Is Statement of Cash Flows?

The Statement of Cash Flows (also called the Cash Flow Statement) is one of the three core financial statements, alongside the Income Statement and the Balance Sheet. It reports the actual cash generated and used by a business over a specific accounting period.

Unlike the Income Statement, which is prepared on an accrual basis and can include revenues earned but not yet received, the cash flow statement reveals the hard reality: how much cash actually moved in and out of the company.

02 Why Is the Indirect Method Used in Cash Flow Statements?

The indirect method starts with net income from the income statement and works backward to arrive at cash from operations. It is preferred by the vast majority of publicly traded companies because:

- It is less costly to prepare, no need to separately classify every cash receipt and payment.

- It provides a clear reconciliation bridge between profitability and cash generation.

- It is required under U.S. GAAP as a supplemental disclosure even if the direct method is chosen.

- Analysts find it useful for spotting earnings quality issues.

03 Indirect Method vs Direct Method Cash Flow Statement

Both methods produce identical cash from operating activities totals. The difference lies entirely in how the operating section is presented.

| Feature | Indirect Method | Direct Method |

|---|---|---|

| Starting Point | Net Income | Cash received from customers |

| Approach | Adjustments to reconcile net income | Lists actual cash receipts & payments |

| Data Required | Income statement + balance sheet changes | Detailed cash transaction records |

| Ease of Preparation | Easier | More Complex |

| Industry Usage | ~95% of public companies | ~5% of public companies |

| Transparency | Shows reconciliation to net income | Shows gross cash flows directly |

| GAAP Required Supplemental? | No (it IS the primary presentation) | Yes (reconciliation still required) |

04 Format of Statement of Cash Flows Indirect Method

The statement is divided into three sections. Here is how each is structured:

Section A – Operating Activities

Begins with net income and adjusts for: (1) non-cash expenses such as depreciation and amortisation, (2) gains and losses on asset disposals, and (3) changes in current assets and current liabilities (working capital movements).

Section B – Investing Activities

Reports cash flows from the acquisition and disposal of long-term assets and investments. Purchases are cash outflows; proceeds from sales are inflows.

Section C – Financing Activities

Captures cash flows between the company and its capital providers — banks (loans) and shareholders (equity issuance and dividends).

05 How to Prepare Statement of Cash Flows Indirect Method (Step-by-Step)

06 Statement of Cash Flows Indirect Method Example

The following is a fully worked Statement of Cash Flows using the Indirect Method for a hypothetical company, Meridian Manufacturing Ltd., for the year ended December 31, 2025.

07 Indirect Method Cash Flow Statement Cheat Sheet (Adjustments)

Use this reference when preparing the operating section adjustments under the indirect method.

| Balance Sheet Item | Change | Cash Flow Effect | Reason |

|---|---|---|---|

| Accounts Receivable | ↑ Increase | Subtract | Revenue recognised but cash not yet received |

| Accounts Receivable | ↓ Decrease | Add | Prior period revenue collected in cash this period |

| Inventory | ↑ Increase | Subtract | Cash paid for goods not yet expensed |

| Inventory | ↓ Decrease | Add | Cost of goods sold exceeded purchases – cash conserved |

| Prepaid Expenses | ↑ Increase | Subtract | Cash paid for future expenses not yet on income statement |

| Prepaid Expenses | ↓ Decrease | Add | Prior cash payment now expensed – no new cash needed |

| Accounts Payable | ↑ Increase | Add | Expenses recognised but not yet paid in cash |

| Accounts Payable | ↓ Decrease | Subtract | Prior period liabilities paid in cash this period |

| Accrued Liabilities | ↑ Increase | Add | Expense accrued but not yet paid in cash |

| Accrued Liabilities | ↓ Decrease | Subtract | Cash disbursed to settle accruals |

| Deferred Revenue | ↑ Increase | Add | Cash collected before revenue is earned |

| Deferred Revenue | ↓ Decrease | Subtract | Revenue now earned from prior cash receipt |

| Depreciation & Amortisation | Expense on P&L | Always Add | Non-cash charge that reduced net income; no cash outflow |

| Gain on Asset Sale | On P&L | Always Subtract | Proceeds classified in investing; remove from operating |

| Loss on Asset Sale | On P&L | Always Add | Non-cash loss that reduced net income |

08Statement of Cash Flows Indirect Method – Quick Reference (Cash Inflows & Outflows)

- Collections from customers

- Proceeds from asset sales

- New loan proceeds

- Equity share issuance

- Receipt of dividends (GAAP: operating)

- Tax refunds received

- Payments to suppliers

- Salaries and wages paid

- Capital expenditures (CapEx)

- Loan and interest repayments

- Dividends paid to shareholders

- Income taxes paid

09 Frequently Asked Questions

What is the difference between the direct and indirect method of cash flow?

Both methods produce the same total for cash from operating activities. The indirect method starts with net income and adjusts for non-cash items and working capital changes. The direct method lists actual cash receipts and payments from customers, suppliers, and employees. The indirect method is far more commonly used in practice because it is simpler to prepare using standard financial statements.

Why is depreciation added back under the indirect method?

Depreciation is a non-cash expense, it reduces net income on the income statement but does not require any cash payment in the current period. Since we start with net income, which has already been reduced by depreciation, we must add it back to reflect the true cash generated by operations. The cash was paid when the asset was originally purchased, which is captured in investing activities.

How do you treat an increase in accounts receivable in the cash flow statement?

An increase in accounts receivable means the company recognised revenue on the income statement but has not yet collected the cash. Therefore, it is subtracted in the operating section. The revenue boosted net income, but no cash came in (so we reduce the cash figure to correct for this). Conversely, a decrease in receivables is added back because cash was collected on prior revenue.

Where does interest paid appear on the cash flow statement?

Under U.S. GAAP, interest paid is classified as an operating activity. Under IFRS (IAS 7), companies have the option to classify interest paid as either operating or financing activities, the choice must be applied consistently and disclosed. Most IFRS reporters use the operating classification, but financing is also acceptable and used by some entities.

Can a company be profitable but have negative operating cash flow?

Absolutely. This is one of the most important insights the cash flow statement provides. A company can report net income while consuming cash if, for example, it is growing rapidly and extending credit to customers (rising receivables) or building up inventory. Sustained negative operating cash flow despite positive net income is a red flag analysts watch closely as it may signal aggressive revenue recognition or working capital stress.

Are dividends received classified as operating or investing activities?

Under U.S. GAAP, dividends received are classified as operating activities. Under IFRS, they can be classified as either operating or investing. Dividends paid are classified as financing under GAAP, or optionally as operating or financing under IFRS.

(Qualified) Chartered Accountant – ICAP

Master of Commerce – HEC, Pakistan

Bachelor of Accounting (Honours) – AeU, Malaysia