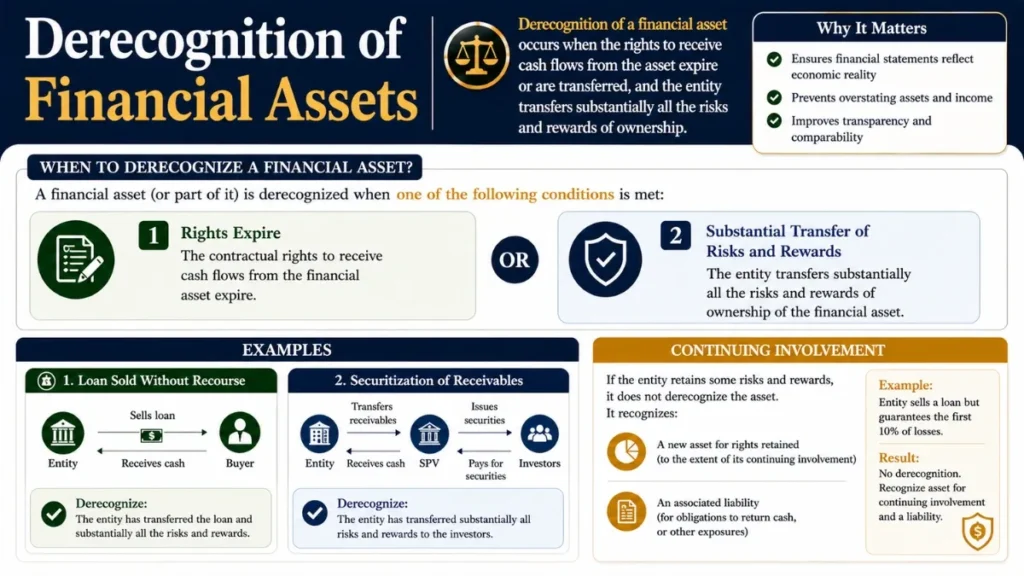

Derecognition of financial assets refers to removing a financial asset from the balance sheet when the contractual rights to cash flows expire or are transferred. Under IFRS 9, businesses must assess risks, rewards, and control before derecognition.

Derecognition of Financial Assets

A complete guide to removing financial assets from the balance sheet; criteria, decision framework, accounting treatment, and practical examples under IFRS 9.

What is Derecognition of Financial Assets?

Derecognition of financial assets refers to the removal of a previously recognised financial asset or part of a financial asset from an entity’s statement of financial position (balance sheet). Under IFRS 9 Financial Instruments (which replaced IAS 39 for most entities from 1 January 2018), derecognition is one of the most conceptually complex areas in financial instrument accounting.

The central question is: has the entity genuinely shed the economic substance of the asset, or does it still bear the risks and enjoy the rewards associated with it? If the answer is “still bears,” the asset remains on balance sheet despite any legal transfer.

IFRS 9 Derecognition Criteria for Financial Assets

Expiry of Contractual Rights

The contractual rights to the cash flows from the financial asset have expired. This is the simplest case (for example), a bond that has matured and been repaid in full.

Transfer + Risks & Rewards

The entity transfers the financial asset and substantially all the risks and rewards of ownership transfer to the buyer. Full derecognition applies.

Transfer + Control

The entity transfers the asset but neither transfers nor retains substantially all risks and rewards, it derecognises only if it has also transferred control.

IFRS 9 Derecognition Decision Tree

IFRS 9 Appendix B (paragraphs B3.2.1 – B3.2.17) sets out a step-by-step decision framework. Follow each question in sequence:

Transfer of Financial Assets

Under IFRS 9.3.2.4, an entity “transfers” a financial asset if, and only if, it either:

1 – Direct Transfer of Cash Flow Rights

The entity transfers its contractual rights to receive the cash flows of the financial asset to a third party. This is the most straightforward form of transfer, as seen in a standard outright sale of a loan portfolio or trade receivable.

2 – Pass-Through Arrangement

The entity retains the contractual rights to the cash flows but assumes a contractual obligation to pay those cash flows to one or more recipients (the “eventual recipients”), satisfying all three pass-through conditions (see Section 6).

Risks and Rewards Test in Derecognition

The risks and rewards test is the primary determinant of derecognition once a transfer has occurred. IFRS 9 does not define “substantially all” numerically, requiring professional judgement, though the standard does provide qualitative guidance.

| Outcome | Risk & Reward Position | Accounting Treatment |

|---|---|---|

| Full Derecognition | Substantially all transferred | Remove asset; recognise gain/loss |

| No Derecognition | Substantially all retained | Treat proceeds as secured borrowing |

| Continuing Involvement | Mixed – assess control | Recognise only to extent of continuing involvement |

Examples of Retained Risks and Rewards

The following arrangements are indicators that derecognition is NOT appropriate because the transferor retains substantially all risks and rewards:

- Sale and repurchase agreements at a fixed price (repo transactions)

- Securities lending agreements with a right and obligation to repurchase

- Sale of a financial asset with a total return swap retaining market risk

- Sale with a credit recourse obligation that covers all expected credit losses

- Sale with a put or call option that is deeply in the money

Pass-Through Arrangements Under IFRS 9

When an entity retains the legal cash flow rights but agrees to pass them on, it must satisfy all three of the following conditions under IFRS 9.3.2.5 to be treated as a “transfer” for derecognition purposes:

Condition 1: No Obligation to Pay Unless Collected

The entity has no obligation to pay amounts to the eventual recipients unless it collects equivalent amounts from the original asset. Short-term advances with the right of full recovery do not breach this condition.

Condition 2: No Selling or Pledging

The entity is prohibited from selling or pledging the original financial asset other than as collateral to the eventual recipients for the obligation to pay them cash flows.

Condition 3: No Material Delay

The entity has an obligation to remit any cash flows it collects on behalf of the eventual recipients without material delay. It may not reinvest those cash flows, except in cash or cash equivalents during the short settlement period.

Accounting Treatment for Derecognition of Financial Assets

When a financial asset is fully derecognised, IFRS 9.3.2.12 requires the following:

Gain or Loss on Derecognition

The difference between the carrying amount of the derecognised asset and the consideration received (including any new asset obtained less any new liability assumed) is recognised in profit or loss.

| Account | DR/CR | Amount | Notes |

|---|---|---|---|

| Cash / Receivable | DR | Sale proceeds | Consideration received |

| Financial Asset | CR | Carrying amount | FVTPL / amortised cost balance |

| Gain on Derecognition | CR | Difference | P&L – IFRS 9.3.2.12 |

OCI Recycling (FVOCI Assets)

For financial assets measured at Fair Value through Other Comprehensive Income (FVOCI) such as debt instruments under the hold-to-collect-and-sell business model, the cumulative gain or loss previously recognised in OCI is reclassified (recycled) to profit or loss on derecognition.

| Account | DR/CR | Amount |

|---|---|---|

| Cash | DR | Sale proceeds |

| Financial Asset (FVOCI) | CR | Fair value (= carrying amount) |

| OCI – Cumulative Fair Value Gain | DR | Recycled OCI balance |

| Gain on Derecognition (P&L) | CR | Total gain recognised |

Continuing Involvement Accounting Under IFRS 9

When neither fully transferred nor fully retained, the entity recognises the financial asset only to the extent of its continuing involvement. A corresponding liability is also recognised. The asset and liability are measured to reflect the rights and obligations retained by the entity.

| Type of Continuing Involvement | Asset Measurement | Liability Measurement |

|---|---|---|

| Guarantee over transferred asset | Lower of: original carrying amount or maximum guarantee amount | Guarantee amount + initial fair value of guarantee |

| Written call option retained by transferor | Lower of: fair value or option exercise price | Option exercise price + fair value of option |

| Purchased put option held by transferee | Fair value of transferred asset | Fair value of put option + present value of difference |

Derecognition of Financial Assets Examples

Factoring of Trade Receivables (Without Recourse)

Scenario: Entity A sells €5 million of trade receivables to a factor. The factor pays 90% upfront and assumes all credit risk. Entity A has no obligation to repurchase defaulted receivables.

Analysis: Substantially all risks (primarily credit risk) and rewards (primarily interest from early collection) have transferred to the factor. The pass-through conditions are not relevant here as rights were legally transferred outright.

Conclusion: ✅ Full derecognition. The receivables are removed from the balance sheet. A loss on derecognition (discount fee) is recognised in profit or loss.

Repo Transaction (Sale and Repurchase Agreement)

Scenario: Bank B “sells” government bonds with a carrying amount of £10 million to a counterparty for £9.8 million, with a contractual obligation to repurchase them in 30 days for £9.84 million (a fixed price).

Analysis: The repurchase at a fixed price means the bank retains substantially all of the price risk (rewards) and credit risk. This is economically a secured borrowing, not a sale.

Conclusion: ❌ No derecognition. Bonds remain on balance sheet. The £9.8 million received is recognised as a financial liability. The difference of £0.04 million is recognised as interest expense over 30 days.

Mortgage Securitisation with Subordinated Tranche Retained

Scenario: A bank transfers a £100 million mortgage portfolio to an SPV. It sells 90% senior notes to investors but retains 10% first-loss (subordinated) notes and also provides a liquidity facility.

Analysis: The retained subordinated notes and liquidity facility indicate the bank continues to absorb a significant portion of credit risk and variability of cash flows. The risks-and-rewards outcome is “mixed.” Control assessment: the SPV investors can sell their notes freely and do not need the bank’s consent → bank has lost control.

Conclusion: ⚠️ Continuing involvement – the bank derecognises 90% of the portfolio but retains 10% on balance sheet, with a corresponding liability for the liquidity facility.

Loan Participation (Funded Participation)

Scenario: Bank C originates a $20 million loan and sells a 60% participation to Bank D. Bank D bears credit risk pro-rata. Bank C retains the legal title and administers the loan.

Analysis: 60% of the risks and rewards have transferred. Bank C retains 40% of credit risk and interest income. The transfer is partial – “mixed” outcome. Can Bank D sell its participation? Yes, freely in the secondary market.

Conclusion: ⚠️ Partial derecognition of 60%; Bank C retains $8 million on balance sheet and derecognises $12 million. Proceeds and gain/loss are allocated proportionally.

Partial Derecognition of Financial Assets

IFRS 9.3.2.2 allows derecognition of a part of a financial asset, but only in strictly defined circumstances. Partial derecognition is permitted when the part being transferred is one of the following:

| Type of “Part” | Example | Permitted? |

|---|---|---|

| Specifically identified cash flows | Only the interest cash flows from a bond (stripped coupon) | ✅ Yes |

| Fully proportionate share of cash flows | 60% pro-rata share of all cash flows from a loan | ✅ Yes |

| Fully proportionate share of specifically identified cash flows | 60% of the interest cash flows from a bond | ✅ Yes |

| Non-proportionate or non-specific residual | First £1m of cash flows from a £5m loan | ❌ No – assess entire asset |

IFRS 7 Disclosure Requirements for Derecognition

IFRS 7 Financial Instruments: Disclosures (paragraphs 13 – 14E) requires extensive disclosures when financial assets are transferred. The objective is to allow users of financial statements to evaluate the nature of the risks retained and the financial effect.

Disclosures for Transferred Assets (Fully Derecognised)

If the entity has transferred assets that are fully derecognised but continues to have any form of involvement, it must disclose: the nature of the involvement, the carrying amount of assets and liabilities relating to that involvement, maximum exposure to loss, undiscounted cash flows to repurchase, maturity analysis, and any gain or loss on derecognition.

Disclosures for Transferred Assets Not Fully Derecognised

When financial assets fail derecognition, entities must disclose: the nature of the assets, the nature of risks and rewards retained, when there is continuing involvement, the carrying amounts of the asset and associated liability on a gross basis and the net exposure.

Common Derecognition Mistakes Under IFRS 9

Frequently Asked Questions

Key Takeaways

Derecognition of financial assets is a critical area requiring careful application of the IFRS 9 decision framework. Here are the essential points:

- Derecognition is triggered by expiry of rights, transfer + risks/rewards, or transfer + loss of control.

- A legal transfer alone is insufficient, economic substance governs the outcome.

- Pass-through arrangements must satisfy all three conditions to count as a transfer.

- “Substantially all” risks and rewards is a judgemental assessment, not a bright-line test.

- Partial derecognition is only permitted for qualifying “parts” under IFRS 9.3.2.2.

- FVOCI debt instruments require OCI recycling to P&L on derecognition; equity FVOCI instruments do not.

- IFRS 7 disclosures are extensive, document the derecognition assessment thoroughly.

(Qualified) Chartered Accountant – ICAP

Master of Commerce – HEC, Pakistan

Bachelor of Accounting (Honours) – AeU, Malaysia