IAS 16 states that property, plant and equipment (PPE) is initially measured at its cost, subsequently measured either using a cost or revaluation model, and depreciated so that its depreciable amount is allocated on a systematic basis over its useful life.

International Accounting Standard

IAS 16 – Property, Plant

and Equipment

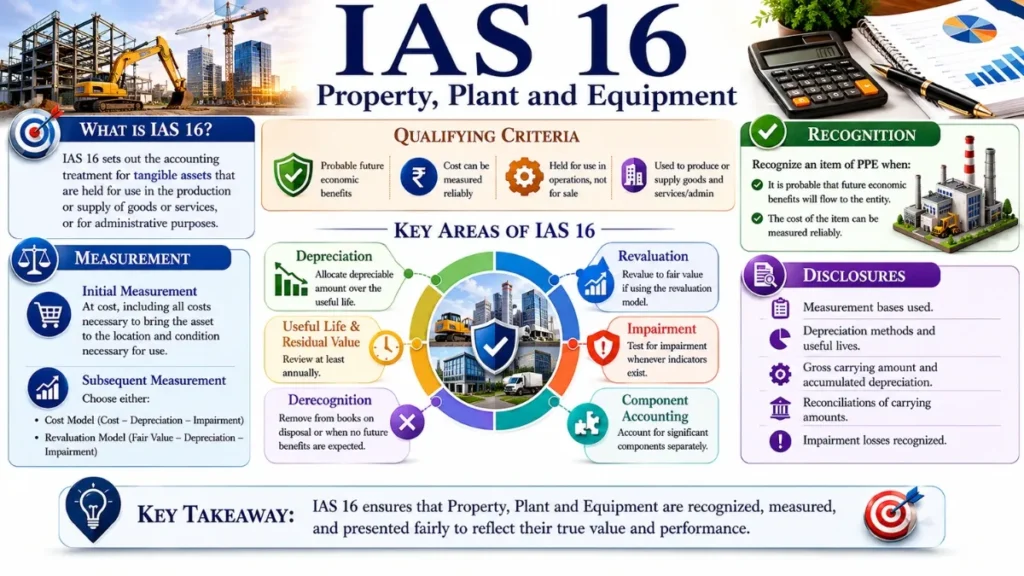

What Is IAS 16?

IAS 16 is the core IFRS standard governing how entities recognise, measure, and disclose tangible long-lived assets. It ensures that stakeholders receive transparent, comparable, and reliable information about an entity’s physical asset base.

Property, plant and equipment (PPE) are tangible items held for use in the production or supply of goods or services, for rental to others, or for administrative purposes and expected to be used over more than one reporting period. Unlike inventory, PPE is not held for sale in the ordinary course of business.

IAS 16 – Property, Plant and Equipment was originally issued by the International Accounting Standards Committee in December 1993, adopted by the IASB in April 2001, and substantially revised in December 2003. Subsequent amendments have refined its scope to include bearer plants (2014), clarify acceptable depreciation methods (2014), address pre-use proceeds (2020), and align with IFRS 18 – Presentation and Disclosure in Financial Statements (2024).

Core Objective

IAS 16 establishes principles for recognising PPE as assets, measuring their carrying amounts, and measuring the depreciation charges and impairment losses to be recognised in relation to them (IAS 16.1).

Scope & Exclusions

IAS 16 applies to all PPE. However, certain categories of assets are excluded from its scope and instead governed by specialist standards:

Scope Exclusions – IAS 16.3

Assets classified as held for sale (IFRS 5), biological assets other than bearer plants (IAS 41), mineral rights and reserves such as oil and gas, and exploration and evaluation assets (IFRS 6) are all outside the scope of IAS 16.

IAS 16 does, however, apply to PPE used to develop or maintain assets that fall outside its scope (for example), machinery used in the extraction of mineral reserves is within scope even though the reserves themselves are not.

IAS 16 Recognition Criteria

An item of PPE is recognised as an asset when both of the following criteria are satisfied (IAS 16.7):

Probable Future Economic Benefits

It is probable that future economic benefits associated with the item will flow to the entity. Management must assess the probability based on available evidence at the time of initial recognition.

Reliable Measurement of Cost

The cost of the item can be measured reliably. In most cases, the transaction price provides a reliable measure of cost at the acquisition date.

Component Accounting Under IAS 16

IAS 16 requires a component approach each major component of an item of PPE with a cost that is significant relative to the total cost must be depreciated separately (IAS 16.43). This reflects the economic reality that different parts of a complex asset may have different useful lives.

Practical Example – Component Accounting

An aircraft body may have a useful life of 25 years, its engines 15 years, and its interior fittings 8 years. Each component is depreciated separately over its respective useful life rather than depreciating the entire aircraft uniformly.

Subsequent Costs

Day-to-day servicing (repairs and maintenance) is recognised immediately in profit or loss because such expenditure merely maintains rather than enhances an asset’s capacity to generate economic benefits (IAS 16.12). However, replacement of major components is capitalised and the carrying amount of the replaced part is derecognised.

Safety-critical or environment-related assets that do not directly generate future economic benefits may nonetheless be capitalised if they are necessary to enable other assets to generate economic benefits (IAS 16.11) for example, a water treatment plant required for a chemical production process.

Initial Measurement Under IAS 16 (Measuring PPE at Cost)

An item of PPE that qualifies for recognition is initially measured at its cost (IAS 16.15). The cost includes all expenditure necessary to bring the asset to the location and condition required for its intended use.

| Cost Component | Status | Explanation |

|---|---|---|

| Purchase price (net of trade discounts) | Include | Including import duties and non-refundable purchase taxes (IAS 16.16a) |

| Site preparation costs | Include | Directly attributable costs to bring asset to required location and condition |

| Professional fees (architects, engineers) | Include | If directly attributable to the acquisition or construction of the asset |

| Installation and assembly costs | Include | Necessary to make asset operational in the manner intended by management |

| Initial delivery and handling | Include | Costs incurred to transport the asset to its intended location |

| Dismantling and restoration costs | Include | Initial estimate per IAS 37; unwinding of discount recognised as finance cost |

| General overheads and admin costs | Exclude | Not directly attributable; recognised as period expenses when incurred |

| Abnormal waste and rework costs | Exclude | Cannot capitalise costs arising from errors in construction |

| Proceeds from pre-use sales (since 2022) | Exclude | Amendment: proceeds from items produced before intended use recognised in P&L |

| Staff training costs | Exclude | Expensed as incurred; not part of the asset’s cost |

Deferred Payment

Where payment is deferred beyond normal credit terms, the asset is recorded at the cash price equivalent at the date of recognition. The difference between that amount and the total payments made is recognised as interest expense over the credit period (IAS 16.23).

Asset Exchanges

When an asset is acquired through exchange of a non-monetary asset, the cost is measured at the fair value of the asset given up (or received if more clearly evident), unless the transaction lacks commercial substance, in which case cost equals the carrying amount of the asset surrendered (IAS 16.24–26).

Subsequent Measurement (Cost Model vs Revaluation Model)

After initial recognition, an entity must choose one of two measurement policies, applied consistently to each class of PPE (IAS 16.29):

- Carrying amount = cost minus accumulated depreciation minus accumulated impairment losses

- Simpler to apply; no need for external valuations

- Historical cost basis; asset not marked to market

- Impairment tested under IAS 36 when indicators exist

- Most commonly used in practice

- Carrying amount = fair value at revaluation date, less subsequent depreciation and impairment

- Revaluations must be regular enough to ensure carrying amount ≈ fair value

- Entire class of PPE must be revalued simultaneously

- Revaluation surplus credited to Other Comprehensive Income (OCI)

- Revaluation deficit generally charged to profit or loss

Accounting for Revaluation Movements

A revaluation increase is credited to Other Comprehensive Income and accumulated in a revaluation surplus in equity, unless it reverses a revaluation decrease previously recognised in profit or loss, in which case the reversal goes to profit or loss.

A revaluation decrease is charged directly to profit or loss unless the asset has an existing revaluation surplus, in which case the decrease is first set against the surplus in OCI.

Revaluation Surplus Transfer

The revaluation surplus may be transferred directly to retained earnings as the asset is used (depreciation) or on derecognition. This is a transfer within equity and does not pass through profit or loss.

Depreciation of Property, Plant & Equipment Under IAS 16

Depreciation is the systematic allocation of a depreciable amount over the useful life of an asset. Each significant component of an item of PPE must be depreciated separately, the component approach in action.

Key Concepts

The depreciable amount is the cost (or revalued amount) of an asset minus its residual value, the estimated amount an entity would receive from disposing of the asset at the end of its useful life, in similar condition to its current age.

Useful life is either the period over which the asset is expected to be available for use, or the number of production units expected to be obtained. This is an entity-specific estimate, not a statutory life.

Depreciation commences when the asset is available for use not when it is actually put in service and ceases at the earlier of the date the asset is classified as held for sale or the date it is derecognised.

Straight-Line Method

A constant charge over the useful life of the asset. Best suited when an asset provides uniform benefits over time.

Annual Charge = (Cost − Residual Value) ÷ Useful LifeDiminishing Balance

A decreasing charge over the useful life. Appropriate when an asset provides greater benefits in earlier years (e.g. technology assets).

Charge = Carrying Amount × Depreciation Rate %Units of Production

Charge based on actual output or usage. Ideal for assets whose consumption is better measured by activity than by time (e.g. mining equipment).

Charge = (Cost − RV) ÷ Total Units × Units ProducedRevenue-Based Methods Prohibited

Since the 2014 amendment, IAS 16 explicitly prohibits the use of revenue-based depreciation methods. Revenue reflects factors beyond the consumption of the economic benefits embedded in the asset (e.g. selling price and sales volume) and is therefore inappropriate as a basis for depreciation.

Land and Buildings

Land and buildings are separable assets and accounted for separately. Land generally has an indefinite useful life and is therefore not depreciated (unless it is a quarry or landfill site with a finite life). Buildings are depreciated over their estimated useful lives.

Review of Useful Life and Residual Value

The residual value, useful life, and depreciation method must all be reviewed at least at each financial year-end. Any changes are treated as changes in accounting estimate, applied prospectively under IAS 8 (not retrospectively as an error or policy change).

IAS 16 Illustrative Examples

Initial Recognition – Manufacturing Plant

A manufacturing entity acquires a production facility. The following costs are incurred:

| Item | Amount (USD) | Treatment |

|---|---|---|

| Purchase price | 4,800,000 | Capitalise |

| Import duties | 120,000 | Capitalise |

| Site preparation | 85,000 | Capitalise |

| Installation costs | 65,000 | Capitalise |

| Staff training | 30,000 | Expense |

| Admin overhead allocated | 20,000 | Expense |

Initial cost recognised = USD 5,070,000 (4,800,000 + 120,000 + 85,000 + 65,000)

| Account | DR (USD) | CR (USD) |

|---|---|---|

| Property, Plant & Equipment | 5,070,000 | — |

| Training Expense | 30,000 | — |

| Admin Overhead Expense | 20,000 | — |

| Cash / Payables | — | 5,120,000 |

Straight-Line Depreciation – 20 Year Asset

Facility cost: $5,000,000 · Useful life: 20 years · Residual value: $200,000

| Account | DR (USD) | CR (USD) |

|---|---|---|

| Depreciation Expense | 240,000 | — |

| Accumulated Depreciation – PPE | — | 240,000 |

After Year 5: Carrying amount = $5,000,000 − (5 × $240,000) = $3,800,000

Revaluation Model – Upward Revaluation

An entity applies the revaluation model. An asset with a cost of $3,000,000 and accumulated depreciation of $600,000 (carrying amount $2,400,000) is revalued to fair value of $2,900,000.

Revaluation surplus = $2,900,000 − $2,400,000 = $500,000 (recognised in OCI)

| Account | DR (USD) | CR (USD) |

|---|---|---|

| Accumulated Depreciation | 600,000 | — |

| PPE (Gross) | — | 100,000 |

| OCI – Revaluation Surplus (Equity) | — | 500,000 |

Note: The gross carrying amount is restated; accumulated depreciation is eliminated against it.

Impairment of Property, Plant & Equipment

IAS 16 does not itself specify impairment testing, this is governed by IAS 36 – Impairment of Assets. However, IAS 16 requires that impairment losses and reversals of impairment be applied to reduce or restore the asset’s carrying amount.

Under IAS 36, an entity assesses at each reporting date whether there is any indication that an asset may be impaired. If such an indication exists, the entity estimates the asset’s recoverable amount the higher of:

Fair Value Less Costs of Disposal

The price that would be received to sell the asset in an orderly transaction between market participants, net of disposal costs.

Value in Use

The present value of estimated future cash flows expected to arise from the asset’s continued use and ultimate disposal.

If the carrying amount exceeds the recoverable amount, an impairment loss is recognised immediately in profit or loss (or against revaluation surplus to the extent of any existing surplus for that asset).

Derecognition of PPE

An item of PPE is derecognised (removed from the statement of financial position) when (IAS 16.67):

Disposed Of

The asset has been sold, donated, or otherwise transferred, and the entity no longer controls it.

No Future Economic Benefits

No future economic benefits are expected from the asset’s use or disposal (for example), an asset that has been abandoned or scrapped.

Gain on Disposal ≠ Revenue

Gains and losses on derecognition of PPE are included in profit or loss when the item is derecognised, but they must not be classified as revenue, since disposal of PPE is not in the ordinary course of business (IAS 16.68).

IAS 16 Disclosure Requirements

IAS 16 mandates extensive disclosures for each class of PPE (IAS 16.73–79). Key required disclosures include:

- Measurement basis used for determining gross carrying amount (cost or revaluation)

- Depreciation methods applied to each class of PPE

- Useful lives or depreciation rates used

- Gross carrying amount and accumulated depreciation (including impairment losses) at beginning and end of period

- Reconciliation of the carrying amount at beginning and end of the period: additions, disposals, acquisitions through business combinations, revaluations, impairments, depreciation, and foreign exchange differences

- Restrictions on title or assets pledged as security for liabilities

- Expenditure recognised during construction of self-constructed assets

- Contractual commitments for the acquisition of PPE

- Compensation received from third parties for impaired, lost or given-up PPE included in profit or loss

Additional Revaluation Disclosures

Where the revaluation model is applied, entities must also disclose: the effective date of the revaluation; whether an independent valuer was involved; the methods and significant assumptions used to estimate fair value; the carrying amount that would have been recognised under the cost model; and the revaluation surplus, including changes during the period and any restrictions on distribution.

Key Amendments to IAS 16

Frequently Asked Questions

IAS 16 governs owned property, plant and equipment – tangible assets an entity holds as its own. IFRS 16 Leases – governs assets held under lease arrangements, where the entity has a right-of-use asset rather than outright ownership. A right-of-use asset under IFRS 16 may be measured and presented similarly to owned PPE but arises from a different set of contractual arrangements and is depreciated over the shorter of the lease term or the asset’s useful life.

Yes. A change from the cost model to the revaluation model is a change in accounting policy under IAS 8. However, IAS 8.17 includes a specific exemption: a change from cost to revaluation is permitted when it provides more reliable and relevant information. When switching, the entity does not restate prior periods, the revaluation is applied prospectively from the date of the policy change.

Depreciation begins when the asset is available for use i.e. when it is in the location and condition necessary for it to operate in the manner intended by management. It does not wait for actual use to commence. Depreciation ceases at the earlier of the date the asset is classified as held for sale (or included in a disposal group) under IFRS 5, or the date the asset is derecognised.

No. Property held to earn rental income or for capital appreciation (or both) is investment property and is accounted for under IAS 40 – Investment Property. However, owner-occupied property (used in the production of goods and services or for administrative purposes) is within the scope of IAS 16. If an owner-occupied property changes use and becomes investment property, it is transferred to IAS 40 at its carrying amount at the date of transfer (cost model) or at fair value (revaluation model, with any fair value increase to OCI).

Bearer plants such as grapevines, oil palm trees, and rubber trees are living plants used in the production of agricultural produce over more than one period. Since the 2014 amendment, bearer plants are within the scope of IAS 16 (not IAS 41) because their biological transformation is not the primary value driver; they function like manufacturing equipment. The produce growing on bearer plants remains within IAS 41.

Government grants relating to the purchase of PPE are accounted for under IAS 20 – Accounting for Government Grants, not IAS 16 itself. An entity may present such grants either by deducting the grant from the asset’s carrying amount (thereby reducing future depreciation) or by recording the grant separately as deferred income to be recognised in profit or loss over the asset’s useful life.

(Qualified) Chartered Accountant – ICAP

Master of Commerce – HEC, Pakistan

Bachelor of Accounting (Honours) – AeU, Malaysia