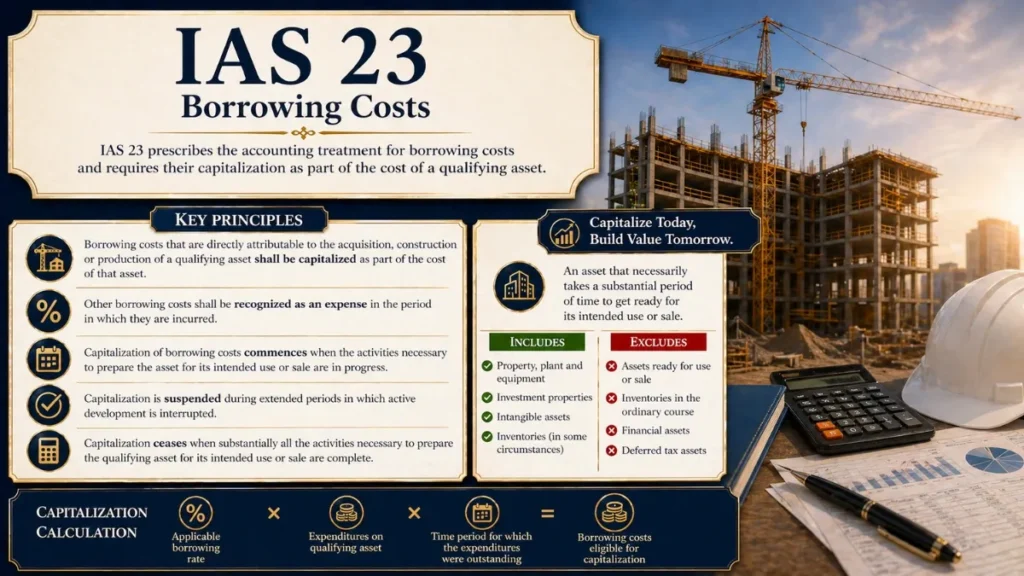

IAS 23 requires that borrowing costs directly attributable to the acquisition, construction or production of a ‘qualifying asset’ (one that necessarily takes a substantial period of time to get ready for its intended use or sale) are included in the cost of the asset.

Other borrowing costs are recognized as an expense in the profit or loss (P&L).

Borrowing Costs

Recognition, Capitalization & Measurement under International Accounting Standards

What is IAS 23?

IAS 23 – Borrowing Costs is the International Financial Reporting Standard that governs how entities account for the costs they incur in connection with borrowing funds. The central question the standard addresses is straightforward yet consequential: should borrowing costs be expensed immediately in the period they are incurred, or should they be capitalized as part of the cost of an asset?

IAS 23 current version of the standard, revised by the International Accounting Standards Board (IASB) in 2007 and effective from 1 January 2009, takes a clear position: borrowing costs that are directly attributable to the acquisition, construction, or production of a qualifying asset must be capitalized as part of that asset’s cost. All other borrowing costs are expensed in the period incurred.

An entity shall capitalize borrowing costs that are directly attributable to the acquisition, construction or production of a qualifying asset as part of the cost of that asset. An entity shall recognize other borrowing costs as an expense in the period in which they are incurred.

Objective and Scope of IAS 23

Objective

The objective of IAS 23 is to prescribe the accounting treatment for borrowing costs. The standard requires entities to capitalize borrowing costs directly attributable to the acquisition, construction, or production of a qualifying asset as part of that asset’s cost.

Scope

IAS 23 applies to all borrowing costs. However, the standard does not apply to:

Qualifying Assets at Fair Value

Assets measured at fair value, such as biological assets within the scope of IAS 41.

Inventories – Short Cycle

Inventories that are manufactured or produced in large quantities on a repetitive basis and do not require a substantial period of time.

Specific Exclusions

Any asset that is ready for its intended use or sale when acquired, since no substantial period is required.

The scope is intentionally broad, IAS 23 captures borrowing costs related to any qualifying asset regardless of whether it is a tangible asset, intangible asset, or investment property.

Key Definitions in IAS 23

IAS 23 provides precise definitions that underpin the correct application of the standard.

| Term | Definition |

|---|---|

| Borrowing Costs | Interest and other costs that an entity incurs in connection with the borrowing of funds. |

| Qualifying Asset | An asset that necessarily takes a substantial period of time to get ready for its intended use or sale. |

| Effective Interest Rate | The rate that exactly discounts estimated future cash payments through the expected life of the financial instrument. |

What Constitutes a Borrowing Cost?

The standard provides a non-exhaustive list of borrowing costs, which include:

Interest Expense

Interest calculated using the effective interest method as described in IFRS 9.

Finance Charges

Finance charges in respect of lease liabilities recognised in accordance with IFRS 16.

Exchange Differences

Exchange differences arising from foreign currency borrowings to the extent they are regarded as an adjustment to interest costs.

Amortization of Costs

Amortization of ancillary costs incurred in connection with the arrangement of borrowings.

Qualifying Assets Explained with Examples

The concept of a qualifying asset is central to IAS 23. A qualifying asset is one that necessarily takes a substantial period of time to get ready for its intended use or sale. The determination of what constitutes a “substantial period of time” requires judgment (in practice), a period of 12 months or more is generally considered substantial, although this threshold is not mandated by the standard.

Examples of Qualifying Assets

Manufacturing Plants

Large-scale production facilities requiring extended construction periods.

Power Generation Facilities

Power stations, wind farms, and energy infrastructure projects.

Investment Properties

Real estate constructed or developed for leasing or capital appreciation.

Intangible Assets

Internally developed intangible assets requiring a substantial development period.

Ships & Aircraft

Vessels and aircraft under construction or long-term order.

Infrastructure

Bridges, roads, dams, and other civil infrastructure projects.

Assets that are ready for use when acquired, financial assets, inventories produced in large quantities on a repetitive basis over short cycles, and assets measured at fair value do not qualify under IAS 23.

“The mere fact that an entity takes time to undertake an activity does not necessarily mean the asset is a qualifying asset. The time taken must be necessary to get the asset ready for its intended use or sale.” – IAS 23 Application Guidance

Recognition Principle of Borrowing Costs

IAS 23 mandates a single accounting treatment, there is no longer a choice between capitalization and expensing (the option to expense was eliminated in the 2007 revision). An entity must capitalize borrowing costs directly attributable to a qualifying asset.

The Directly Attributable Test

Borrowing costs are directly attributable to a qualifying asset when they would have been avoided if the expenditure on the qualifying asset had not been made. This requires distinguishing between two scenarios:

Specific Borrowings

When an entity borrows specifically to fund a qualifying asset, the borrowing costs eligible for capitalization are the actual borrowing costs incurred on that borrowing less any investment income from temporarily investing those borrowings.

General Borrowings

When an entity uses general borrowings to fund a qualifying asset, the amount eligible for capitalization is determined by applying a capitalization rate to the expenditures on that asset. The capitalization rate is the weighted average of borrowing costs applicable to the entity’s outstanding borrowings during the period.

Upper Limit

The total borrowing costs capitalized during a period must not exceed the total borrowing costs incurred during that period. This prevents entities from capitalizing more than they actually paid.

Commencement, Suspension and Cessation of Capitalization

When Does Capitalization Commence?

An entity begins capitalizing borrowing costs only when all three of the following conditions are met simultaneously:

Expenditures are being incurred

The entity is making expenditures on the qualifying asset including cash payments, transfers of other assets, or assumption of interest-bearing liabilities.

Borrowing costs are being incurred

The entity is actually incurring borrowing costs related to, or capable of being attributed to, the qualifying asset.

Activities are in progress

The activities necessary to prepare the asset for its intended use or sale are in progress, this includes more than just physical construction; it includes technical and administrative work.

Suspension of Capitalization

An entity must suspend capitalization during extended periods in which active development is interrupted. However, capitalization is not suspended when a temporary delay is a necessary part of getting an asset ready for use (e.g., a period of high water levels preventing construction of a bridge).

When Does Capitalization Cease?

Capitalization of borrowing costs ceases when substantially all the activities necessary to prepare the qualifying asset for its intended use or sale are complete. The asset does not need to be 100% finished, if only minor customization or decoration remains, the asset is typically considered substantially complete.

When construction of an asset is completed in parts, and each part is capable of being used while construction of other parts continues, capitalization of borrowing costs ceases for that part when substantially all activities to prepare it are complete.

Capitalization Rate Calculation Under IAS 23

When an entity uses general borrowings (i.e., funds drawn from a general pool rather than borrowed specifically for one asset), it must compute a capitalization rate to determine how much of its borrowing costs can be attributed to, and therefore capitalized on, a qualifying asset.

The borrowing costs capitalized in any period shall not exceed the total borrowing costs incurred in that period. This is the absolute upper limit regardless of the formula result.

IAS 23 Illustrative Example

The following example illustrates the application of the capitalization rate approach for general borrowings.

Scenario: BuildCo Ltd is constructing a new manufacturing plant (a qualifying asset). During the year ending 31 December 20X1, the entity incurs the following expenditures on the plant. The entity does not use specific borrowings for this project; instead, it relies on its general pool of debt.

STEP 1: Expenditure on Qualifying Asset

| Date | Expenditure | Months Outstanding | Weighted Amount |

|---|---|---|---|

| 1 Jan 20X1 | $2,000,000 | 12/12 | $2,000,000 |

| 1 Apr 20X1 | $3,000,000 | 9/12 | $2,250,000 |

| 1 Oct 20X1 | $1,500,000 | 3/12 | $375,000 |

| Weighted Average Expenditure | $4,625,000 | ||

STEP 2: Outstanding Borrowings & Weighted Average Rate

| Loan | Principal | Interest Rate | Annual Interest |

|---|---|---|---|

| Loan A (fixed) | $5,000,000 | 7.0% | $350,000 |

| Loan B (variable) | $3,000,000 | 9.0% | $270,000 |

| Loan C (bond) | $2,000,000 | 6.5% | $130,000 |

| Total | Avg: 7.5% | $750,000 | |

STEP 3: Capitalization Calculation

| Capitalization Rate | $750,000 / $10,000,000 = 7.5% |

| Borrowing Costs Eligible for Capitalization | $4,625,000 × 7.5% = $346,875 |

| Total Borrowing Costs Incurred (Upper Limit) | $750,000 |

| Amount Capitalized | $346,875 ✓ (within limit) |

IAS 23 Disclosure Requirements

IAS 23 requires entities to disclose the following in their financial statements:

Amount of Borrowing Costs Capitalized

The total amount of borrowing costs capitalized during the period, reported as part of the cost of qualifying assets.

Capitalization Rate Applied

The capitalization rate used to determine the borrowing costs eligible for capitalization in respect of general borrowings.

Additional disclosures under IAS 1 and IFRS 7 (Financial Instruments: Disclosures) regarding interest expense and the nature of financial liabilities typically complement the IAS 23 disclosures in practice.

History & Amendments

Original IAS 23 Issued

The original standard allowed borrowing costs to be expensed or capitalized, a free choice for preparers.

First Revision

IAS 23 was reformatted in 1993. The benchmark treatment remained expensing, with capitalization as an allowed alternative.

Major Revision by IASB

The IASB eliminated the option to expense borrowing costs, mandating capitalization for qualifying assets. This aligned IAS 23 with US GAAP (ASC 835-20) and removed the “benchmark vs. allowed alternative” dichotomy.

Revised Standard Effective

The 2007 revision became effective for annual periods beginning on or after 1 January 2009, with early adoption permitted.

IASB Annual Improvements

Minor clarifications were issued as part of IASB’s annual improvements cycle, particularly regarding the interaction with IFRS 16 lease liabilities and the treatment of foreign currency borrowing costs.

IAS 23 vs US GAAP (ASC 835-20)

Both IAS 23 and US GAAP’s ASC 835-20 require capitalization of borrowing costs for qualifying assets, but there are important differences in how they are applied.

| Feature | IAS 23 (IFRS) | ASC 835-20 (US GAAP) |

|---|---|---|

| Capitalization required? | Yes – mandatory | Yes – mandatory |

| Exchange differences included? | Yes – to limited extent | No |

| Lease finance charges included? | Yes (IFRS 16) | Context-dependent |

| Investment income offset? | Yes – specific borrowings only | No offset required |

| Definition of “substantial period” | Judgment-based | Judgment-based |

| Avoidable cost notion | Directly attributable | Avoidable interest concept |

| Consolidated group borrowings | Weighted average rate | May use parent rate |

Frequently Asked Questions

(Qualified) Chartered Accountant – ICAP

Master of Commerce – HEC, Pakistan

Bachelor of Accounting (Honours) – AeU, Malaysia