The concept provision vs contingent liability explains that ‘Provision‘ is a liability that is recognized in the financial statements when a company has a probable obligation or a present obligation and ‘Contingent Liability‘ is a potential liability that may arise from past events but is uncertain in terms of its timing or amount.

Provision vs Contingent Liability

In financial reporting, the way a company accounts for obligations that are uncertain in timing or amount has a significant impact on its balance sheet, profit and loss, and the trust of investors. The concept provision vs contingent liability explains the underlying challenge under IAS 37.

While both provision and contingent liabilities deal with uncertainty about future outflows, they are treated very differently under accounting standard IAS 37 Provisions, Contingent Liabilities and Contingent Assets issued by the International Accounting Standards Board (IASB).

What Is a Provision in Accounting and Contingent Liability?

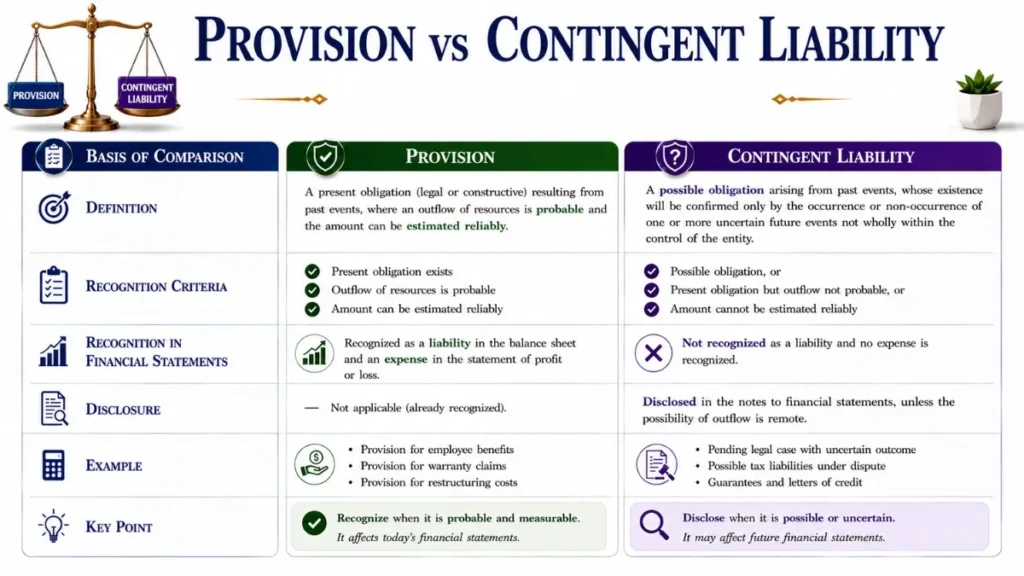

A provision is a liability of uncertain timing or amount. It is recognised on the balance sheet when: (1) there is a present obligation arising from a past event, (2) it is probable that an outflow of economic resources will be required to settle it, and (3) a reliable estimate can be made of the amount.

A contingent liability is either (a) a possible obligation whose existence depends on uncertain future events outside the entity’s control, or (b) a present obligation that is not recognised because an outflow of resources is not probable, or the amount cannot be measured reliably. It is not recognised on the balance sheet, only disclosed in notes.

“A provision is a liability of uncertain timing or amount. A contingent liability is a possible obligation or a present obligation that does not meet the recognition criteria.” — IAS 37, Paragraphs 10 & 27

IAS 37 Recognition Criteria Explained

When Should a Provision Be Recognized?

Under IAS 37, paragraph 14, all three conditions below must be met simultaneously:

-

✓Present obligation from a past event

The entity has a legal or constructive obligation that has arisen as a result of a past event (the “obligating event”). The entity has no realistic alternative to settling it. -

✓Probable outflow of economic resources

“Probable” means more likely than not i.e., a greater than 50% probability that the obligation will result in an outflow. Under US GAAP this threshold is “probable” but interpretation differs. -

✓Reliable estimate can be made

The amount of the obligation can be estimated with reasonable accuracy. IAS 37 notes it will only be in extremely rare cases that a reliable estimate cannot be made.

When Is a Contingent Liability Disclosed?

-

✗Only a possible (not present) obligation exists

The existence of the obligation will only be confirmed by future events not wholly within the entity’s control. -

✗Outflow is not probable

Even if a present obligation exists, if the probability of an outflow is ≤50%, it is treated as a contingent liability. -

✗Amount cannot be reliably estimated

In very rare circumstances, even a probable obligation may not meet the recognition threshold if no reliable estimate is possible.

Difference Between Provision and Contingent Liability

| Criteria | Provision | Contingent Liability |

|---|---|---|

| Nature of obligation | Present obligation (legal or constructive) | Possible obligation or present obligation failing criteria |

| Probability of outflow | Probable (>50%) | Not probable (≤50%) |

| Reliable estimate | Yes – can be estimated | No – or not reliably measurable |

| Balance sheet recognition | ✓ Recognised as a liability | ✗ Not recognised |

| P&L impact | Yes – charge to income statement | No – direct charge (unless it becomes probable) |

| Disclosure in notes | Disclosed (description, amount, uncertainty) | Disclosed unless outflow is remote |

| If outflow is remote | N/A | No disclosure required at all |

| Standard reference | IAS 37, Para 14–26 | IAS 37, Para 27–30 |

| Examples | Warranty obligations, legal claims (probable), restructuring costs | Pending lawsuits (possible), guarantees (possible) |

Decision Framework: Provision vs Contingent Liability

Use this three-step decision flow to classify any uncertain obligation correctly:

Measurement & Accounting Treatment of Provisions and Contingent Liabilities Under IAS 37

Measuring a Provision

IAS 37 requires a provision to be measured at the best estimate of the expenditure required to settle the present obligation at the end of the reporting period. Where material, provisions should be discounted to present value using a pre-tax discount rate reflecting current market assessments of the time value of money.

For a single obligation, the most likely outcome may be used. For a large population of items (e.g., warranties), the expected value method (probability-weighted average) is more appropriate.

Journal Entry for a Provision

Dr. Expense / Loss Account [Income Statement]

Cr. Provision Account [Balance Sheet – Liability]

When the liability is eventually settled, the provision is debited and cash or payables are credited. If the provision exceeds the actual payment, the surplus is released back to the income statement.

Contingent Liability – No Journal Entry

A contingent liability generates no journal entry. It does not appear on the face of the balance sheet. The accountant’s only action is to prepare an adequate note disclosure (unless the possibility is remote).

If circumstances change and the outflow becomes probable, the contingent liability is reclassified as a provision and recognised on the balance sheet at that point.

Real-World Examples of Provisions and Contingent Liabilities

Product Warranty Obligation

A manufacturer offers a 2-year warranty on products. Past data shows 5% of products need repair costing £200 each. The company provisions £10 per unit sold; it is a present obligation, probable, and reliably estimated.

Pending Lawsuit (Possible Loss)

A company is sued for patent infringement. Legal counsel advises a 30% chance of losing. Since it is not probable (<50%), no provision is made, it is disclosed as a contingent liability in the notes.

Restructuring Costs

Management formally announces a plant closure, creating a constructive obligation. The costs are probable and can be estimated. A restructuring provision is recognised immediately after the announcement.

Environmental Guarantee

A company guarantees an affiliate’s loan. The affiliate is currently financially healthy. The possibility of outflow exists but is not probable, this is disclosed as a contingent liability.

Decommissioning Costs

An oil company has a legal obligation to decommission a rig at the end of its life. This present obligation arises when the rig is constructed. A discounted provision is recognised immediately.

Tax Dispute (Uncertain Outcome)

A company is in dispute with tax authorities over £5m of back taxes. The outcome is uncertain, legal advice places the risk at 40% against. Disclosed as contingent; no provision is raised.

Disclosure Requirements Under IAS 37

Provision Disclosures (IAS 37, Para 84–85)

For each class of provision, an entity must disclose:

- Carrying amount at opening and closing of the period

- Additional provisions made, including increases to existing provisions

- Amounts used (incurred and charged against the provision)

- Unused amounts reversed during the period

- Unwinding of discount / effect of changes in discount rate

- A description of the nature of the obligation and expected timing

- Any uncertainties about amount or timing; assumptions about future events

Contingent Liability Disclosures (IAS 37, Para 86)

For each class of contingent liability (unless remote), disclose:

- A brief description of the nature of the contingent liability

- An estimate of its financial effect (where practicable)

- An indication of the uncertainties relating to amount or timing

- The possibility of any reimbursement

Key Rule: If the possibility of an outflow is remote, no disclosure at all is required for a contingent liability. “Remote” generally means a very small probability, typically below 5–10%, though IAS 37 does not specify a percentage.

IAS 37 at a Glance

IAS 37 – Provisions, Contingent Liabilities and Contingent Assets is the International Accounting Standard that governs these items. It was issued by the International Accounting Standards Board (IASB) and applies to all entities preparing financial statements under IFRS.

The core objective of IAS 37 is to ensure that appropriate recognition criteria and measurement bases are applied to provisions and contingencies, and that sufficient information is disclosed in the notes so that users can understand their nature, timing, and amount.

The standard explicitly excludes from its scope: provisions covered by other standards (e.g. tax under IAS 12, leases under IFRS 16, insurance under IFRS 17), and executory contracts (except onerous contracts).

“An entity shall not recognise a contingent liability. An entity shall disclose a contingent liability, unless the possibility of an outflow of resources embodying economic benefits is remote.” — IAS 37, Paragraph 27

Frequently Asked Questions

(Qualified) Chartered Accountant – ICAP

Master of Commerce – HEC, Pakistan

Bachelor of Accounting (Honours) – AeU, Malaysia