Provision in accounting a Concept as per IAS 37 represent a company’s estimated liabilities or obligations, which are recognized in financial statements as an expense and liability.

Provisions are typically created when there is uncertainty about the amount or timing of a liability, but the company has a legal or constructive obligation to settle that liability.

Provision in Accounting

A complete, authoritative guide to understanding provisions; what they are, how they work, and why they matter for accurate financial reporting.

What is Provision in Accounting?

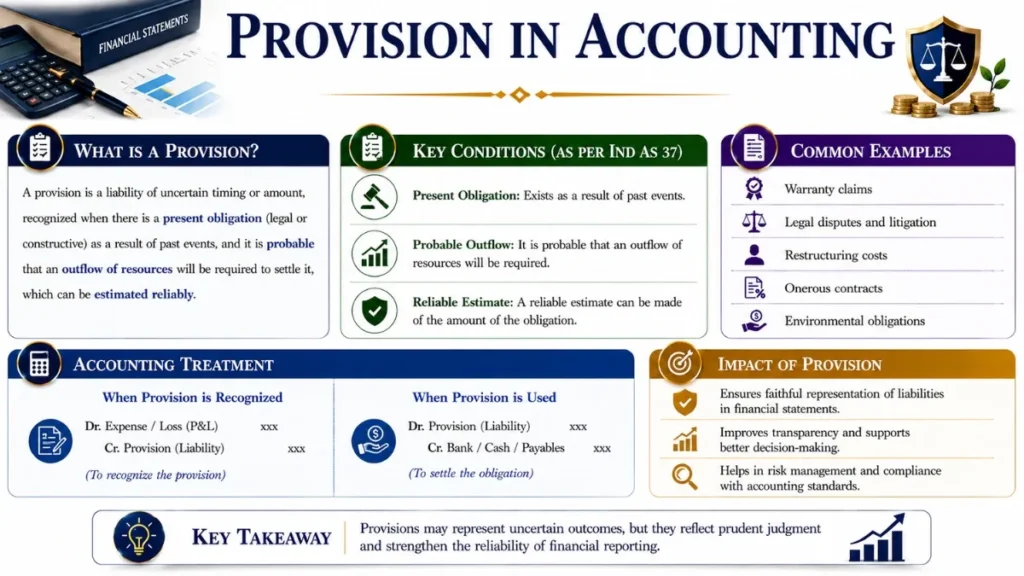

In accounting, a provision is a recognised liability of uncertain timing or amount. It represents an amount set aside out of profits to cover an anticipated future expense or loss, even when the exact amount or timing is not precisely known at the time of recording.

“A provision is a liability of uncertain timing or amount. A liability is a present obligation of the entity arising from past events, the settlement of which is expected to result in an outflow of economic benefits.”

Provisions are a critical component of the accrual basis of accounting, which requires that expenses be recognised in the period they are incurred, regardless of when cash is paid. This ensures financial statements give a true and fair view of a company’s financial position.

Common examples include: setting aside funds for expected bad debts, warranty claims, legal disputes, or employee benefits such as pensions and leave entitlements.

Key point: A provision is not a “rainy day fund” or discretionary saving, it is a formal accounting obligation recognised because a liability is probable and can be reliably estimated.

Recognition Criteria for Provision Under IAS 37

Under IAS 37 (Provisions, Contingent Liabilities and Contingent Assets) issued by the International Accounting Standards Board (IASB), a provision must be recognised only when all three of the following conditions are met:

- 01Present Obligation The entity has a present obligation (legal or constructive) as a result of a past event.

- 02Probable Outflow of Resources It is probable (more likely than not) that an outflow of economic resources will be required to settle the obligation.

- 03Reliable Estimate Possible A reliable estimate can be made of the amount of the obligation. If no estimate is possible, it is disclosed as a contingent liability instead.

Important: If any one of these three criteria is not met, no provision should be recognised. Instead, the item may need to be disclosed as a contingent liability in the notes to the financial statements.

Types of Provision in Accounting

There are several commonly recognised types of provisions, each addressing a different category of anticipated future liability:

Provision for Doubtful/Bad Debts

An estimate of the amount of trade receivables that may not be collected. Reduces the carrying value of debtors on the balance sheet.

Provision for Depreciation

Accumulated reduction in the value of fixed assets over time due to wear, tear, and obsolescence. Applied using straight-line or reducing balance methods.

Provision for Taxation

An amount set aside for expected income tax liability for the current financial year, before the final tax assessment is received.

Provision for Warranty

Estimated cost of honouring warranties on goods sold. Common in manufacturing, electronics, and automotive industries.

Provision for Legal Claims

Funds set aside for ongoing or expected litigation where an unfavourable outcome is probable and the amount can be estimated.

Provision for Restructuring

Recognised when a company has a detailed formal plan to restructure and has raised a valid expectation among affected parties.

Accounting Treatment of Provision – Journal Entries

Creating and utilising a provision involves two stages: the initial recognition (creation) and the subsequent use or reversal. Below are the standard double-entry bookkeeping entries:

1. Creating a Provision (e.g., Provision for Doubtful/Bad Debts)

| Account | Dr / Cr | Amount | Notes |

|---|---|---|---|

| Bad Debts Expense | Dr | $5,000 | Income statement – reduces profit |

| Provision for Doubtful/Bad Debts | Cr | $5,000 | Balance sheet – contra-asset |

2. Utilising a Provision (writing off a Doubtful/Bad debt)

| Account | Dr / Cr | Amount | Notes |

|---|---|---|---|

| Provision for Doubtful/Bad Debts | Dr | $2,000 | Reduces the provision balance |

| Trade Receivables | Cr | $2,000 | Removes the irrecoverable debt |

3. Reversing an Unused Provision

| Account | Dr / Cr | Amount | Notes |

|---|---|---|---|

| Provision for Doubtful/Bad Debts | Dr | $3,000 | Removes the unused provision |

| Bad Debts Expense (reversal) | Cr | $3,000 | Increases profit in current period |

Golden rule: Provisions should only be used for the purpose for which they were originally created. Using a provision to absorb unrelated expenses is not permitted under IFRS or GAAP.

Real-World Examples of Accounting Provisions

Scenario: TechPro Ltd sells 10,000 smartphones for $500 each. Based on historical data, 3% of units will require warranty repairs costing an average of $80 each.

Calculation: 10,000 × 3% × $80 = $24,000 provision

TechPro records a $24,000 warranty provision in the period of sale, matching the expense to the revenue generated, consistent with the matching principle.

Scenario: BuildCorp is being sued by a former employee for wrongful dismissal. Legal counsel advises that it is probable BuildCorp will lose the case, with the most likely settlement at $150,000.

Action: BuildCorp recognises a provision of $150,000 in the current financial year’s accounts.

If the likelihood were only “possible” (not probable), it would be disclosed as a contingent liability with no balance sheet entry.

Scenario: RetailMax has total trade receivables of $200,000. Based on an ageing analysis, it estimates that 5% ($10,000) is unlikely to be collected.

Action: A provision for bad debts of $10,000 is created. Trade receivables appear on the balance sheet at their net realisable value of $190,000.

Provision vs Reserve – Key Differences

Provisions and reserves are frequently confused but are fundamentally different in nature, purpose, and accounting treatment.

| Basis | Provision | Reserve |

|---|---|---|

| Nature | A charge against profit (expense) | An appropriation of profit |

| Purpose | Cover a known liability or loss | Strengthen financial position |

| Profit Impact | Reduces profit for the period | Does not affect profit or loss |

| Mandatory? | Yes, if IAS 37 criteria are met | Discretionary (management decision) |

| Balance Sheet | Liability or contra-asset | Equity section |

| Example | Provision for bad debts, warranty | General reserve, capital reserve |

Provision vs Contingent Liability

The distinction between a provision and a contingent liability depends on the probability of the outflow of resources:

Record on the balance sheet as a liability and charge the expense to the income statement.

Do not recognise on the balance sheet. Disclose in the notes to the accounts, describing the nature and estimated amount.

No recognition or disclosure is needed unless management considers it useful for users of the financial statements.

IFRS vs US GAAP Provision Accounting

While the fundamental concept is the same, there are important differences in how provisions are treated under IFRS (IAS 37 – Provisions, Contingent Liabilities and Contingent Assets) and US GAAP (ASC 450):

| Aspect | IFRS (IAS 37) | US GAAP (ASC 450) |

|---|---|---|

| Terminology | “Provision” | “Accrued liability” / “loss contingency” |

| Recognition Threshold | Probable (>50%) | Probable (similar, less defined) |

| Measurement | Best estimate or expected value | Minimum of range if no best estimate |

| Discounting | Required for long-term provisions | Permitted but not required |

| Restructuring | Constructive obligation required | More specific criteria apply |

Note: Under US GAAP, the term “provision” is also used to refer to income tax expense (e.g., “provision for income taxes”), which is distinct from the IFRS usage. Context is important when reading US financial statements.

How to Calculate a Provision

The method of calculating a provision depends on its type. Here are the most common approaches:

Specific Provision (Identified Debts)

A provision is created for a specific debtor known to be in financial difficulty. The full amount owed by that debtor (or the estimated irrecoverable portion) is provisioned individually.

General Provision (Portfolio Approach)

Applied to a pool of receivables or obligations. Typically calculated as a percentage based on historical default rates:

Provision Amount = Total Portfolio Value × Expected Loss Rate (%)

Expected Value Method (Warranty / Legal)

Uses probability-weighted outcomes when there are multiple possible amounts:

Provision = Σ (Possible Outcome × Probability of That Outcome)

Discounted / Present Value Method

For long-term provisions (e.g., decommissioning costs), the future obligation is discounted back to its present value using a risk-free or pre-tax discount rate. This is required under IFRS when the time value of money is material.

Provision in Accounting – Key Takeaways

- A provision is a liability of uncertain timing or amount, recognised on the balance sheet.

- Three conditions must all be met: present obligation, probable outflow, and reliable estimate.

- Creating a provision reduces profit (debit expense, credit provision).

- Provisions are governed by IAS 37 under IFRS and ASC 450 under US GAAP.

- Provisions differ from reserves, provisions are charges; reserves are appropriations of profit.

- Provisions must only be used for the purpose for which they were originally created.

- If an obligation is possible but not probable, disclose as a contingent liability instead.

- Long-term provisions should be discounted to present value when the time value of money is material.

Frequently Asked Questions

(Qualified) Chartered Accountant – ICAP

Master of Commerce – HEC, Pakistan

Bachelor of Accounting (Honours) – AeU, Malaysia