A basic earnings per share calculator helps investors and businesses quickly ‘measure profitability’ on a per-share basis.

By dividing net income by the weighted average number of outstanding shares, this tool provides a clear view of financial performance. It’s essential for comparing companies and making informed investment decisions.

Financial Analysis Tools – Entrepreneurial Hub

Basic Earnings Per Share Calculator

How to Use the Basic Earnings Per Share Calculator

Enter values below, results appear instantly

Total net profit from the income statement

Dividends paid to preferred shareholders (enter 0 if none)

Time-weighted average number of common shares during the reporting period

Basic Earnings Per Share

$0.00

What Is Basic Earnings Per Share (EPS)?

Basic Earnings Per Share (Basic EPS) is a fundamental financial metric that quantifies the amount of a company’s net profit allocated to each outstanding share of common stock. It is one of the most widely referenced figures in equity analysis, reported prominently in income statements and earnings releases, and used extensively by investors, analysts, and regulators to evaluate a company’s profitability on a per-share basis.

Under ASC 260 – Earnings Per Share by Financial Accounting Standards Board (FASB) and IAS 33 – Earnings Per Share issued by the International Accounting Standards Board (IASB), publicly traded companies are required to disclose both basic and diluted EPS on the face of the income statement. Basic EPS is the simpler of the two figures, it considers only the actual shares currently outstanding and does not account for any potentially dilutive securities such as stock options, warrants, or convertible bonds.

Profitability Signal

Higher EPS generally indicates greater profitability and is a key driver of a stock’s market price and valuation multiples like the Price-to-Earnings (P/E) ratio.

Standardized Comparison

EPS converts absolute profit figures into a per-share metric, enabling meaningful comparisons across companies of different sizes and capital structures.

Regulatory Requirement

GAAP (ASC 260) and IFRS (IAS 33) mandate EPS disclosure for all publicly traded entities, making it a standardized figure across global financial markets.

Investor Benchmark

Analysts compare reported EPS against consensus estimates. Beats and misses relative to expectations can cause significant share price movements on earnings announcement days.

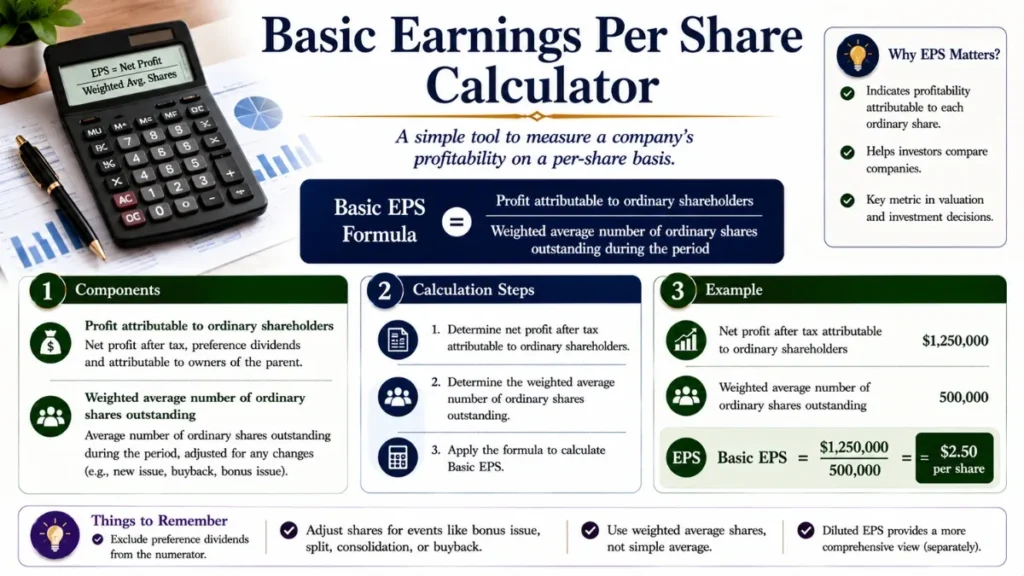

Basic Earnings Per Share Formula Explained

Our basic earnings per share calculator uses the following basic EPS formula which is straightforward, yet each component carries specific accounting definitions that must be correctly applied to arrive at an accurate figure:

Basic EPS = (Net Income − Preferred Dividends) ÷ Weighted Average Common Shares Outstanding

- Net Income

- The bottom-line profit after all expenses, taxes, and interest are deducted. Sourced directly from the income statement.

- Preferred Dividends

- Declared dividends on cumulative preferred stock, or paid dividends on non-cumulative preferred stock, subtracted to isolate earnings available to common shareholders.

- Earnings Available to Common

- The numerator of the formula, net income after removing preferred shareholders’ claim. This is the profit pool distributable to common equity holders.

- Weighted Average Shares

- Common shares outstanding time-weighted by the portion of the year they were in existence. Accounts for share issuances, buybacks, and splits during the period.

How to Calculate Basic Earnings Per Share: Step-by-Step

Simply use the basic earnings per share calculator above, or follow these four steps to compute basic earnings per share accurately, whether you are analyzing a company’s annual report or building a financial model:

Identify Net Income

Locate the net income figure on the company’s income statement. This is the profit remaining after deducting cost of goods sold, operating expenses, depreciation, interest expense, and income taxes. For the purpose of EPS, use the net income attributable to the parent company (excluding non-controlling interest portions where applicable under IFRS).

Subtract Preferred Dividends

Determine the preferred dividends to be subtracted. For cumulative preferred stock, deduct dividends earned during the period even if not declared or paid. For non-cumulative preferred stock, only deduct dividends actually declared in the period. If a company has no preferred stock, this value is zero.

Compute Weighted Average Common Shares Outstanding

Calculate the weighted average shares by multiplying each tranche of shares outstanding by the fraction of the year they were outstanding, then summing the results. For example, if a company had 1,000,000 shares for the first half and issued 200,000 more shares midway through the year, the weighted average would be 1,000,000 × 0.5 + 1,200,000 × 0.5 = 1,100,000 shares. Stock splits and stock dividends are applied retrospectively to all prior periods presented.

Divide to Get Basic EPS

Divide the earnings available to common shareholders (Step 1 minus Step 2) by the weighted average common shares outstanding (Step 3). The result, expressed as a dollar amount per share, is Basic EPS. A positive figure means the company was profitable; a negative figure (a loss per share) indicates a net loss during the period.

Basic Earnings Per Share Calculation Example

Consider a fictional publicly traded company, Meridian Industries Inc., reporting the following data for its fiscal year:

| Item | Value | Notes |

|---|---|---|

| Net Income | $8,500,000 | From the consolidated income statement |

| Preferred Dividends | $350,000 | Cumulative Series A preferred, declared during the year |

| Earnings Available to Common | $8,150,000 | $8,500,000 − $350,000 |

| Common Shares – Jan 1 to Jun 30 | 3,000,000 | Shares outstanding for first half of year |

| New Shares Issued – Jul 1 | +400,000 | Secondary offering on July 1 |

| Common Shares – Jul 1 to Dec 31 | 3,400,000 | Shares outstanding for second half of year |

| Weighted Average Shares | 3,200,000 | (3,000,000 × 0.5) + (3,400,000 × 0.5) |

| Basic EPS | $2.55 | $8,150,000 ÷ 3,200,000 Profitable |

Basic EPS vs Diluted EPS: Key Differences

While basic EPS uses only shares actually outstanding, diluted EPS incorporates all potential shares that could be created if all dilutive securities were converted or exercised. This gives a more conservative and arguably more complete picture of per-share earnings.

| Feature | Basic EPS | Diluted EPS |

|---|---|---|

| Share Base | Actual common shares outstanding | Common shares + all dilutive potential shares |

| Complexity | Simple, straightforward | Requires treasury stock method, if-converted method |

| Dilutive Securities Included | None | Stock options, warrants, convertible bonds, convertible preferred |

| Value Relationship | Always ≥ Diluted EPS | Always ≤ Basic EPS |

| Investor Use | Historical profitability baseline | Worst-case per-share dilution scenario |

| GAAP/IFRS Requirement | Required | Required (public companies) |

When the gap between basic and diluted EPS is large, it signals significant potential dilution, a risk factor worth scrutinizing carefully, particularly for technology companies and startups that grant substantial equity compensation.

Limitations of Basic EPS

Despite its ubiquity, basic EPS has several important limitations that analysts and investors should keep in mind:

Ignores Dilution Risk

Basic EPS does not reflect the impact of stock options, warrants, or convertible instruments that could reduce per-share earnings if exercised or converted.

Sensitive to Accounting Choices

Net income can be influenced by non-cash items, one-time charges, and management’s accounting judgments, making EPS susceptible to manipulation or distortion.

Ignores Capital Structure

EPS does not account for how a company is financed. Two companies with identical EPS may have very different levels of financial leverage and associated risk.

No Cash Flow Insight

Earnings can diverge significantly from cash flow due to accruals. A company with high EPS may still face liquidity problems if it does not generate sufficient operating cash flow.

Frequently Asked Questions About Basic Basic Earnings Per Share

What is a good Basic EPS value?

There is no universal “good” EPS threshold, what constitutes a strong EPS depends heavily on the industry, company size, growth stage, and historical trend. A mature utility company may have a high, stable EPS, while a high-growth technology company might report a near-zero or negative EPS while still commanding a premium valuation based on future earnings potential.

Investors typically assess EPS in context: relative to analyst consensus estimates, year-over-year growth rate, and in comparison to industry peers. A rising EPS trend over multiple periods is generally more meaningful than any single quarter’s figure in isolation.

Can Basic EPS be negative?

Yes. A negative Basic EPS commonly referred to as a loss per share occurs when a company’s net loss exceeds any preferred dividends during the reporting period. This means the company consumed more resources than it generated in revenue after accounting for all costs. Negative EPS is common among early-stage companies, startups, and firms undergoing major restructuring. It is reported as a negative figure (e.g., −$1.45 per share) on the income statement.

How does a stock buyback affect Basic EPS?

Share repurchases (buybacks) reduce the number of shares outstanding, which lowers the denominator in the EPS formula. Assuming net income remains constant, fewer shares outstanding means each remaining share claims a larger slice of earnings, resulting in a higher Basic EPS. This is one reason companies use buybacks as an earnings management tool, often to meet or beat EPS-based executive compensation targets. Analysts scrutinize whether EPS growth is driven by genuine profit improvement or purely by share count reduction.

Why is the weighted average used instead of year-end share count?

Using the weighted average reflects the economic reality that shares outstanding can change throughout the year due to new issuances, buybacks, or conversions. If a company doubled its share count on December 31, using year-end shares would misrepresent the earnings base that shareholders participated in for most of the year. The weighted average method time-weights each tranche of shares, producing a figure that best matches the share structure present during the earnings-generating period.

Is Basic EPS the same as Earnings Per Share (EPS)?

The term “EPS” is often used informally to refer to Basic EPS, as it is the simpler and more foundational measure. However, technically, “EPS” can refer to either basic or diluted EPS. Under GAAP and IFRS, companies must report both. When analysts and financial media report “earnings per share,” they are usually referring to the basic figure unless otherwise specified. Always check whether a quoted EPS figure is basic or diluted, as the distinction matters when assessing share dilution risk.

How do stock splits affect the EPS calculation?

Stock splits are applied retrospectively to all prior periods presented in the financial statements. If a company performs a 2-for-1 stock split, the weighted average shares outstanding in all comparative periods is doubled, and prior EPS figures are restated accordingly. This retroactive adjustment ensures that EPS figures across different reporting periods remain comparable on a consistent per-share basis, preventing artificial distortions in trend analysis.

(Qualified) Chartered Accountant – ICAP

Master of Commerce – HEC, Pakistan

Bachelor of Accounting (Honours) – AeU, Malaysia