FVOCI also referred as Fair Value Through Other Comprehensive Income is a classification under IFRS 9 used for certain financial assets. It allows changes in fair value to be recorded in other comprehensive income instead of profit or loss.

FVOCI – Fair Value Through

Other Comprehensive

Income

A definitive guide to FVOCI; understanding classification, measurement, recognition and disclosure of financial assets under IFRS 9.

What Is FVOCI in IFRS 9?

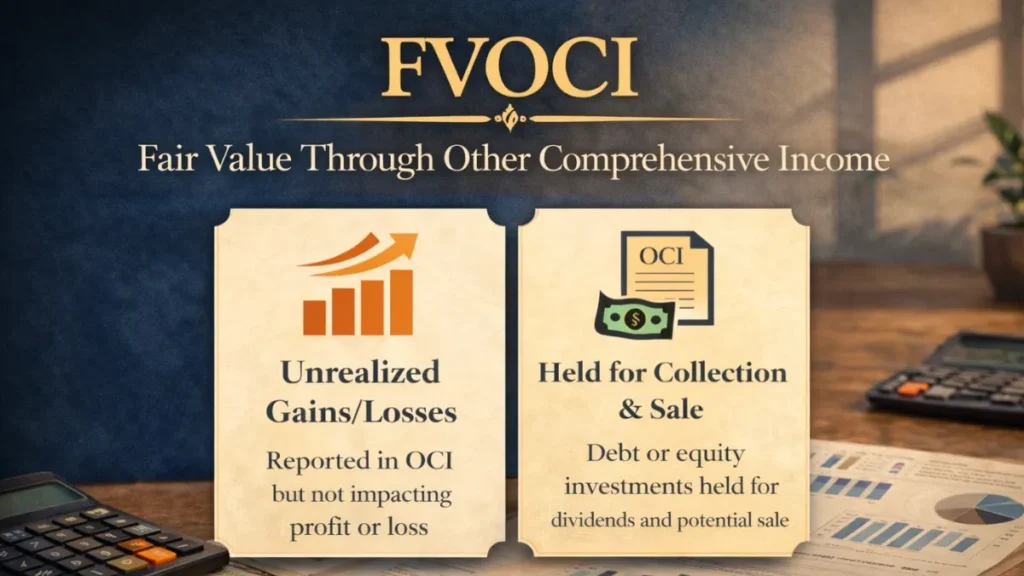

FVOCI stands for Fair Value through Other Comprehensive Income. It is one of three measurement categories for financial assets introduced by IFRS 9 – Financial Instruments (effective 1 January 2018), alongside Amortised Cost (AC) and Fair Value through Profit or Loss (FVTPL).

Under Fair Value through Other Comprehensive Income, a financial asset is carried on the balance sheet at its current fair value, but changes in that fair value do not immediately flow through the income statement. Instead, they accumulate in Other Comprehensive Income (OCI), a separate section of equity until specific trigger events cause them to be reclassified or recycled.

It is designed to reduce income statement volatility for assets that are held for collection and for sale, reflecting both their contractual cash flow purpose and their trading reality without creating artificial earnings swings.

Balance Sheet

Asset carried at fair value each reporting period.

OCI – Not P&L

Fair value gains & losses park in OCI, not the income statement.

Recycling

For debt instruments, OCI gains recycle to P&L on derecognition.

ECL Still Applies

Expected Credit Losses hit P&L even under FVOCI for debt instruments.

FVOCI Meaning in Accounting

A financial asset is measured at Fair Value through Other Comprehensive Income when its contractual cash flows represent solely payments of principal and interest (the SPPI test), and the entity’s business model is to achieve objectives by both collecting contractual cash flows and selling financial assets.

The definition contains two distinct pathways:

Pathway A – Debt Instruments (Mandatory FVOCI)

A debt instrument must be classified as FVOCI when both of the following conditions are met:

- Business Model Test: The objective is to collect contractual cash flows and sell the financial asset.

- SPPI Test: Contractual cash flows are solely payments of principal and interest on the outstanding principal.

Pathway B – Equity Instruments (Irrevocable Election)

An equity instrument may be designated at FVOCI at initial recognition (on an instrument-by-instrument basis) provided it is not held for trading. This election is irrevocable, and gains/losses in OCI are never recycled to profit or loss.

Key difference: Debt instrument FVOCI gains recycle to P&L on disposal. Equity instrument FVOCI gains are permanently stranded in OCI and may only be transferred within equity.

Classification Criteria under IFRS 9

Determining whether a financial asset qualifies for FVOCI requires passing two sequential tests. If either test fails, the asset is classified at FVTPL by default.

Decision Tree – Debt Instruments

The Business Model Test in Practice

The business model is assessed at a portfolio level, not instrument by instrument. Evidence of a collect and sell business model includes:

- Management’s stated objectives and past practice of both collecting cash flows and selling assets

- Performance metrics that reflect both income received and realised gains on sales

- Active liquidity management with periodic disposal of assets to fund operations

The SPPI Test in Practice

A cash flow fails the SPPI test, and therefore cannot qualify for FVOCI, if it includes leverage features, equity-linked returns, or returns that don’t reflect basic lending risk and the time value of money.

Common instruments that typically qualify: government bonds, investment-grade corporate bonds, and mortgage-backed securities with standard terms. Common failures: convertible notes, equity-linked bonds, CLO tranches with leveraged returns.

Initial & Subsequent Measurement

Initial Recognition

At initial recognition, an FVOCI asset is measured at fair value plus transaction costs (unlike FVTPL where transaction costs are expensed immediately). The effective interest rate (EIR) is established at this point.

Subsequent Measurement – Debt Instruments

After initial recognition, interest income, impairment, and foreign exchange gains/losses are recognised in profit or loss using the effective interest method. All other changes in fair value, the fair value movement net of these items are recognised in OCI. On disposal, the cumulative OCI amount is recycled to profit or loss.

Subsequent Measurement – Equity Instruments (Elected FVOCI)

Dividends are recognised in profit or loss (unless they clearly represent a return of capital). All fair value movements go to OCI and are never reclassified to P&L. On disposal, amounts in OCI may be transferred within equity (e.g., to retained earnings) but not to profit or loss.

Impairment – Expected Credit Losses

Fair Value Through Other Comprehensive Income debt instruments are subject to the full IFRS 9 ECL impairment model. ECL is recognised in profit or loss with a corresponding adjustment to the OCI reserve (not the carrying amount, which remains at fair value). This is conceptually elegant: the fair value already reflects credit risk, so ECL adjusts the OCI split between credit and non-credit movements.

FVOCI Journal Entries with Examples

Entity A purchases a 5-year government bond for $100,000 (par value = fair value) on 1 January 20X1. Coupon rate 4%. At 31 December 20X1, fair value rises to $103,500. EIR = 4%.

Entry 1 – Initial Purchase (1 Jan 20X1)

Asset recorded at fair value (= cost in this case). EIR established at 4%.

Entry 2 – Interest Income (Year End)

$100,000 × 4% EIR. Interest income recognised in P&L via effective interest method.

Entry 3 – Fair Value Movement (Year End)

Fair value increase of $3,500 ($103,500 − $100,000) recognised in OCI, not P&L. Balance sheet carries asset at $103,500.

Entry 4 – Recycling on Disposal

Cumulative OCI balance of $3,500 recycled to profit or loss on derecognition. Total P&L gain = $3,500. Net effect = same as if asset had been FVTPL, but recognised later.

FVOCI vs FVTPL vs Amortised Cost

Understanding Fair Value Through Other Comprehensive Income requires placing it in context alongside the other two IFRS 9 categories. The table below compares all three across key dimensions.

| Criterion | Amortised Cost | FVOCI | FVTPL |

|---|---|---|---|

| Business Model | Collect cash flows only | Collect and sell | Trading / residual |

| SPPI Required? | Yes | Yes (debt) | No |

| Balance Sheet Value | Amortised cost | Fair value | Fair value |

| FV changes go to | N/A (not remeasured) | OCI | Profit or loss |

| Interest income | P&L (EIR) | P&L (EIR) | P&L (contractual) |

| ECL Impairment | P&L | P&L | N/A |

| Recycling on disposal | N/A | Yes (debt) / No (equity) | Already in P&L |

| P&L volatility | Low | Moderate | High |

| Typical instruments | Loans, held-to-maturity bonds | Available-for-sale bonds, strategic equity stakes | Trading securities, derivatives |

Fair Value Through Other Comprehensive Income is sometimes described as the IFRS 9 successor to the old IAS 39 “Available-for-Sale” (AFS) category. The two standards IFRS 9 and IAS 39 are conceptually similar but differ importantly in impairment treatment and the mandatory recycling of OCI for debt instruments.