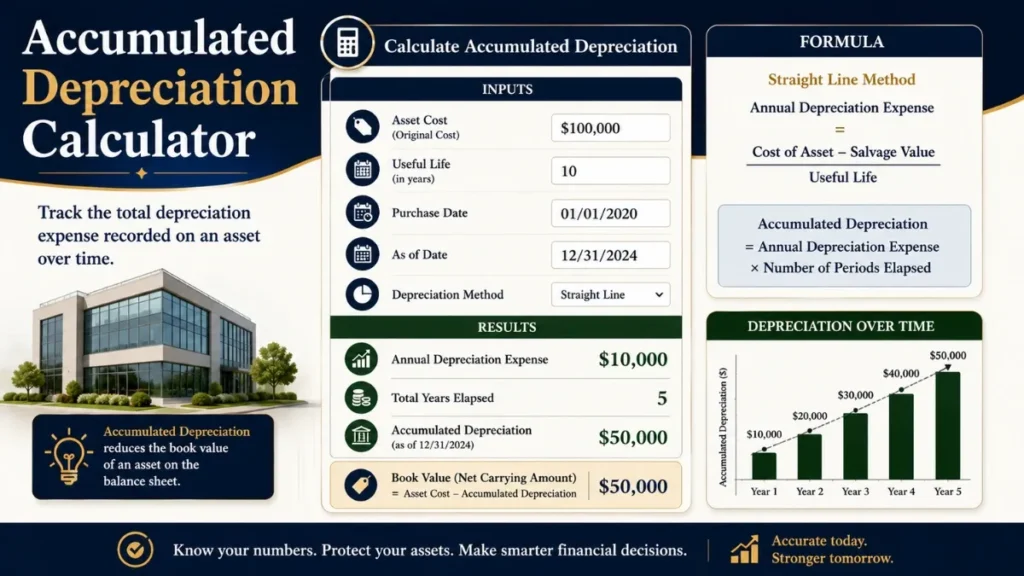

An accumulated depreciation calculator helps businesses and accountants quickly determine the total depreciation of an asset over time. By entering factors like asset cost, useful life, and depreciation method, you can accurately track value reduction.

Accumulated Depreciation Calculator

Compute how much value your asset has lost over time using three industry-standard depreciation methods, instantly and for free.

Calculate Accumulated Depreciation

Leave blank to use double-declining (2 ÷ useful life × 100%)

Rate must be between 1 and 100.Portion of total depreciable amount recovered by the target year.

Year-by-Year Depreciation Schedule

| Year | Depreciation Expense | Accumulated Depreciation | Book Value |

|---|

What Is Accumulated Depreciation?

Accumulated depreciation is the total depreciation expense recorded against a fixed asset from acquisition up to a specific date. It is a contra-asset account on the balance sheet, carrying a credit balance and subtracted from gross asset cost to reveal the asset’s net book value.

Each period a company records depreciation, that amount is simultaneously added to this account. Over the asset’s useful life, accumulated depreciation grows until it equals the depreciable cost (original cost minus salvage value), at which point the asset is fully depreciated.

Understanding accumulated depreciation is essential for:

- Accurately reporting asset values on financial statements

- Tax planning and deduction optimization (Source: irs.gov)

- Making informed asset replacement decisions

- Calculating return on assets and other financial ratios

- Compliance with GAAP and IFRS accounting standards

Accumulated Depreciation = Σ (Annual Depreciation Expenses recorded to date)

Depreciation Methods Comparison Explained

1. Straight-Line Depreciation (SL)

The most widely used method, it spreads the depreciable cost evenly across all years of useful life, resulting in an identical expense each period.

Accumulated Depreciation (Year n) = Annual Depreciation × n

2. Declining Balance (DB) / Double Declining Balance (DDB)

An accelerated method applying a fixed rate to the remaining book value each year. Depreciation is highest in early years and tapers over time. The DDB variant uses twice the straight-line rate.

Annual Depreciationn = Book Valuestart of year × Rate

Accumulated Depreciation (Year n) = Cost − Book Valueend of year n

3. Sum-of-Years-Digits (SYD)

Another accelerated method. A decreasing fraction is applied to depreciable cost each year, the numerator decreases by one annually; the denominator is the sum of all year-digits.

Annual Depreciation (Year k) = (Remaining life at start of year ÷ SYD) × Depreciable Cost

Accumulated Depreciation (Year n) = Σ Annual Depreciation from Year 1 to Year n

Depreciation Methods at a Glance (IAS 16)

| Feature | Straight-Line | Declining Balance | Sum-of-Years Digits |

|---|---|---|---|

| Depreciation Pattern | Equal each year | Higher early, lower later | Higher early, lower later |

| Complexity | Simple | Moderate | Moderate |

| GAAP / IFRS Accepted | ✔ Yes | ✔ Yes | ✔ Yes |

| Best For | Stable-use assets | Tech / vehicles | Early-productivity assets |

| Tax Advantage (Early Years) | ✘ No | ✔ Yes | ✔ Yes |

How to Use This Accumulated Depreciation Calculator

Follow these four steps for instant, accurate depreciation figures:

- Step 1 – Choose a Method. Select Straight-Line, Declining Balance, or Sum-of-Years Digits using the tabs above the input form.

- Step 2 – Enter Asset Details. Input the original purchase cost, expected salvage value at end of life, and total useful life in years.

- Step 3 – Specify the Target Year. Enter the year up to which you need the accumulated depreciation calculated.

- Step 4 – Click “Calculate Depreciation.” Review the KPI summary, progress bar, and the complete year-by-year schedule.

Use the Reset button to clear all inputs. You can switch between methods at any time, fields are preserved so you can compare results across methods.

Accumulated Depreciation Examples

Example 1 – Manufacturing Equipment (Straight-Line)

A factory purchases machinery for $80,000 with a salvage value of $8,000 and useful life of 8 years. Annual depreciation = ($80,000 − $8,000) ÷ 8 = $9,000/year. After 5 years, accumulated depreciation = $9,000 × 5 = $45,000; book value = $80,000 − $45,000 = $35,000.

Example 2 – Company Vehicle (Double Declining Balance)

A delivery van costs $40,000 with a $4,000 salvage value and 5-year life. DDB rate = (2 ÷ 5) × 100% = 40%. Year 1 depreciation = $40,000 × 40% = $16,000. Year 2 = $24,000 × 40% = $9,600. Accumulated after Year 2 = $25,600.

Example 3 – Office Furniture (Sum-of-Years Digits)

Office furniture costs $12,000 with a $2,000 salvage value and 5-year life. SYD = 5+4+3+2+1 = 15. Year 1 = (5/15) × $10,000 = $3,333. Year 2 = (4/15) × $10,000 = $2,667. Accumulated after Year 2 = $6,000.

Frequently Asked Questions

(Qualified) Chartered Accountant – ICAP

Master of Commerce – HEC, Pakistan

Bachelor of Accounting (Honours) – AeU, Malaysia