ISA 500 – Audit Evidence

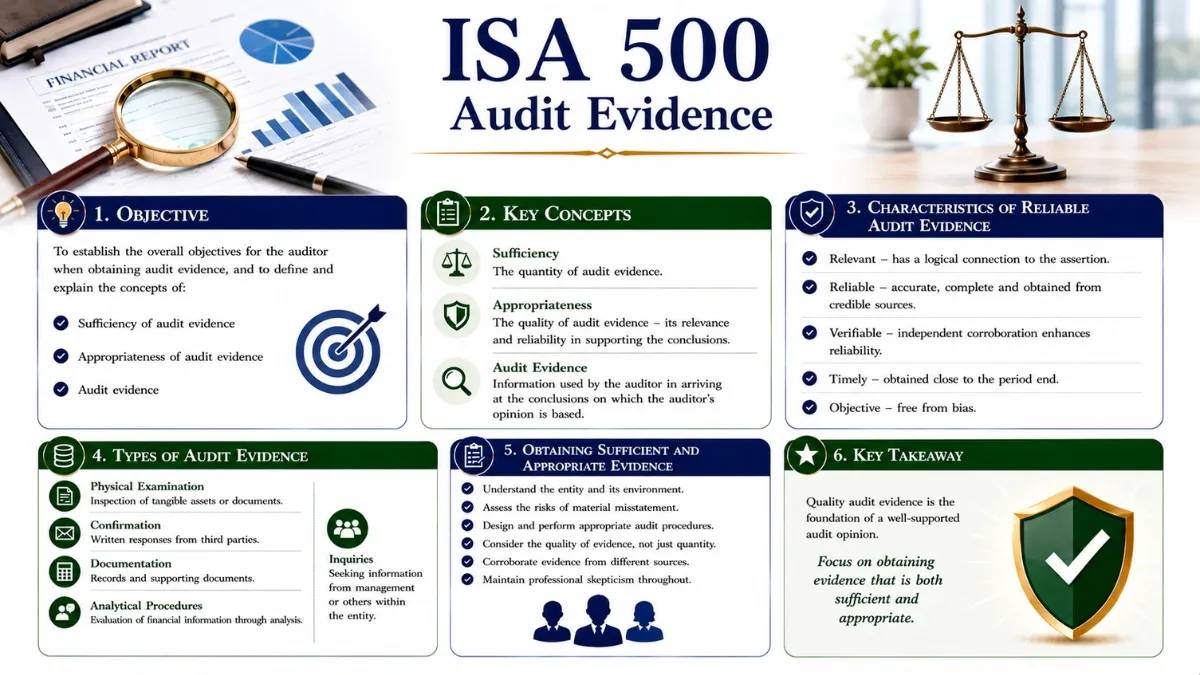

ISA 500 (Revised) explains what constitutes audit evidence in an ‘audit‘ of financial statements and deals with the auditor’s responsibility to design and perform audit procedures to obtain sufficient appropriate audit evidence. International Standards on Auditing ISA 500 – Audit Evidence A comprehensive guide to objectives, requirements, and professional application … Read More