The concept subsidiary vs affiliate refers to the level of ownership and control a parent company has over another business. A ‘subsidiary’ is typically majority-owned and fully controlled, while an ‘affiliate’ involves significant influence without full control.

When a corporation expands beyond its original borders through investment, acquisition, or strategic partnership, it inevitably creates intercompany relationships. Two of the most commonly confused terms in corporate structure are subsidiary and affiliate. While both involve one company holding an ownership stake in another, the legal, financial, and operational consequences diverge significantly depending on how much of that stake is held.

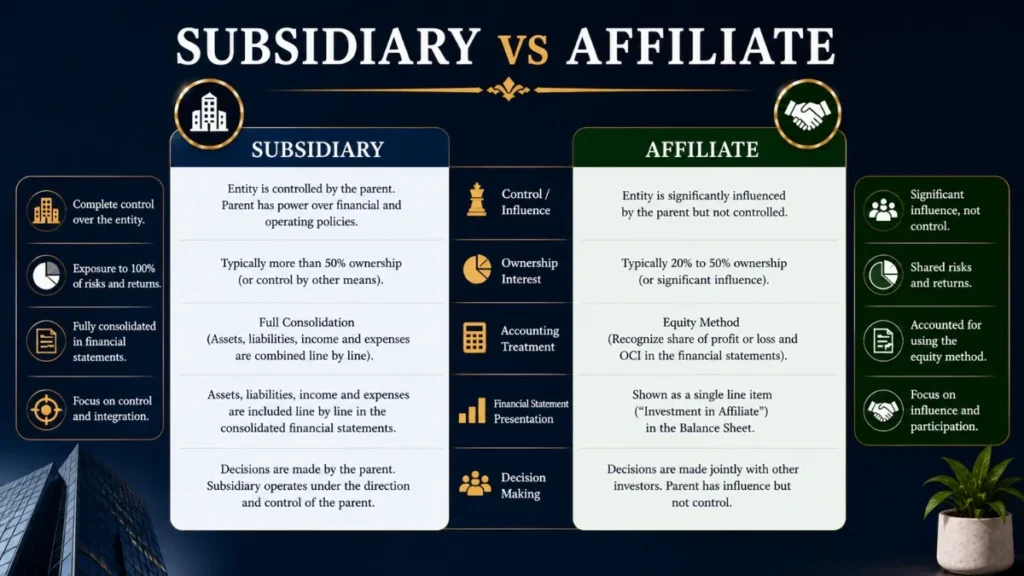

Subsidiary vs Affiliate: What’s the Difference?

A subsidiary is a company in which another company (the parent or holding company) owns more than 50% of the voting shares, thereby exercising majority control over its board and operations. When ownership reaches 100%, the entity is a wholly-owned subsidiary.

An affiliate (also called an associate in IFRS terminology) is a company in which a parent or investor holds a significant influence typically a stake between 20% and 50% of voting shares without having majority control over its governance or operations.

The critical dividing line is the 50% ownership threshold. Cross it and you have a subsidiary; stay below it (but above roughly 20%) and you have an affiliate. Below 20%, the investment is generally treated as a passive financial asset rather than a meaningful intercompany relationship.

Ownership Threshold Spectrum

Control vs Ownership in Corporate Structure

Ownership percentage is the starting point, but courts and accountants look beyond raw numbers. Control is the operative concept for subsidiaries (not merely a numerical majority), but the practical ability to direct an entity’s financial and operating policies to obtain benefit from its activities.

Under IFRS 10 (Consolidated Financial Statements), an investor controls an investee when it has:

- Power over the investee (through voting rights or contractual arrangements)

- Exposure, or rights, to variable returns from its involvement

- The ability to use its power to affect those returns

This means a company can technically hold only 45% of shares yet still be treated as the parent if no other party has more shares and its block votes effectively guarantee control. Conversely, a 55% holder may have control diluted by shareholder agreements that require unanimous consent on key decisions.

Important: Under US GAAP (ASC 810), the concept of a variable interest entity (VIE) can force consolidation even without majority ownership if the investor is the “primary beneficiary”, meaning it absorbs most of the entity’s expected losses or receives most of its expected residual returns. Never rely on ownership percentages alone.

Subsidiary vs Affiliate (Side-by-Side Comparison)

| Criterion | Subsidiary | Affiliate |

|---|---|---|

| Ownership Stake | >50% voting shares | 20–50% voting shares |

| Level of Control | Majority / full control over board & operations | Significant influence; no majority control |

| Accounting Method | Full consolidation (IFRS 10 / ASC 810) | Equity method (IAS 28 / ASC 323) |

| Financial Statements | Fully absorbed into parent’s consolidated financials | Shown as a single-line investment on balance sheet |

| Legal Identity | Separate legal entity; own contracts & liabilities | Separate legal entity; fully independent governance |

| Parent Liability Exposure | Higher – corporate veil may be pierced | Generally limited to investment amount |

| Tax Treatment | Consolidated tax return possible (varies by jurisdiction) | Parent recognizes share of associate’s profit/loss |

| Board Representation | Parent appoints majority of directors | Parent typically holds 1–2 board seats; no majority |

| Brand / Operations | May operate under parent brand or independently | Typically operates independently under own brand |

| Intercompany Eliminations | Required on consolidation (intercompany transactions eliminated) | Not required; treated as arm’s-length transactions |

Accounting Treatment of Subsidiary vs Affiliate

Subsidiaries: Full Consolidation

When a parent company controls a subsidiary, it must prepare consolidated financial statements that combine the financial results of both entities line-by-line. Every asset, liability, revenue, and expense of the subsidiary is incorporated into the parent’s statements, adjusted for intercompany eliminations (e.g., if the parent sells goods to the subsidiary, that revenue must be removed to avoid double-counting).

If the parent does not own 100% of the subsidiary, the portion owned by external shareholders is presented as a non-controlling interest (NCI) on the consolidated balance sheet and income statement.

Affiliates: The Equity Method of Accounting

Affiliates are accounted for using the equity method. The investment initially appears on the parent’s balance sheet at cost. Thereafter:

- The carrying amount is increased by the parent’s proportionate share of the affiliate’s profits

- The carrying amount is decreased by dividends received from the affiliate

- The carrying amount is adjusted for the parent’s share of any other comprehensive income or loss

This produces a single line on the balance sheet (“Investment in Associates”) and a single line in the income statement (“Share of Profit / Loss of Associates”), a much simpler presentation than full consolidation.

“The equity method is a midpoint between full consolidation and treating an investment as a passive financial asset, it reflects economic substance without imposing the complexity of line-by-line aggregation.”

– IASB Conceptual Framework Commentary

Legal Differences Between Subsidiary and Affiliate

Both subsidiaries and affiliates are legally distinct entities, meaning they can enter contracts, own assets, and incur liabilities in their own name. This separation is the foundation of limited liability (in principle), a parent or investor is not responsible for the debts of its subsidiary or affiliate beyond what it has invested.

In practice, however, subsidiaries carry a significantly higher liability risk for the parent because:

- Piercing the corporate veil: Courts can disregard the subsidiary’s separate legal status if it is found to be a mere alter ego of the parent, especially when the parent commingles funds, fails to maintain corporate formalities, or exercises excessive operational control.

- Guarantees: Parents frequently guarantee their subsidiaries’ debts to enable better financing terms, directly creating liability.

- Environmental and regulatory liability: In some jurisdictions, parent companies can be held liable for a subsidiary’s environmental violations, employment violations, or consumer protection breaches.

For affiliates, the parent’s limited influence means courts rarely pierce the corporate veil. The investor’s liability is generally capped at the carrying value of its investment.

Practical tip: Multinationals sometimes deliberately maintain an ownership stake just below 50% in a high-risk venture to retain affiliate classification and thereby contain legal liability, while still exercising board-level strategic influence.

Tax Treatment of Subsidiary vs Affiliate

The tax treatment of subsidiaries versus affiliates varies by jurisdiction, but several common principles apply internationally:

Subsidiaries and Tax Consolidation

In many countries, a parent and its wholly-owned or majority-owned subsidiaries can file a single consolidated tax return. This allows profits in one entity to be offset against losses in another, reducing the overall group tax burden. Intercompany dividends may be exempt or receive a participation exemption to prevent double taxation of the same profits.

However, transfer pricing rules require that transactions between the parent and subsidiary be conducted at arm’s-length prices. Tax authorities in most jurisdictions scrutinize intercompany pricing aggressively to prevent profit-shifting to low-tax territories.

Affiliates and Dividend Taxation

Because affiliates are accounted for on the equity method, the parent recognizes its share of the affiliate’s profits through accounting entries, not actual cash flows. When the affiliate pays dividends, the parent typically receives them as a return of the carrying amount of the investment (reducing the investment on the balance sheet), not as separate income.

Many jurisdictions provide a dividend received deduction (DRD) or participation exemption on qualifying inter-corporate dividends, though the threshold percentage of ownership required to qualify varies.

Advantages and Disadvantages of Both Structures

Subsidiary

✓ Advantages

- Full operational control enables strategic alignment

- Tax consolidation can reduce group-wide tax liability

- Easier to integrate brand, technology, and people

- Parent captures 100% of value creation above its stake

- Facilitates intercompany financing and cash pooling

✗ Disadvantages

- Increased legal and regulatory liability exposure

- Full consolidation increases financial reporting complexity

- Acquisition of majority stake requires significant capital outlay

- NCI holders may create governance friction

- Integration costs can be substantial

Affiliate

✓ Advantages

- Lower capital required to establish strategic relationship

- Limited liability: exposure capped at investment value

- Simpler accounting treatment (equity method)

- Board representation provides strategic insight and influence

- Maintains affiliate’s entrepreneurial independence

✗ Disadvantages

- Minority influence; cannot impose strategic decisions

- Parent shares upside with majority shareholders

- Less visibility into day-to-day financial performance

- Potential misalignment of objectives with majority owners

- Cannot access affiliate’s cash flows directly

Real-World Examples of Subsidiaries and Affiliates

Understanding how Fortune 500 companies structure their intercompany relationships makes these concepts tangible. Below are illustrative examples drawn from publicly reported corporate structures.

YouTube → Alphabet Inc.

Acquired by Google in 2006 for $1.65 billion, YouTube operates as a wholly-owned subsidiary of Alphabet. Its financials are consolidated into Alphabet’s “Google Services” segment. Alphabet appoints its leadership and sets its strategic direction.

Renault–Nissan Alliance

Renault holds approximately 43% of Nissan’s shares, making Nissan a Renault affiliate (associate), not a subsidiary. Renault applies the equity method to this investment and exercises significant influence without operational control.

Instagram → Meta Platforms

Meta (then Facebook) acquired Instagram in 2012 for $1 billion. Instagram is a wholly-owned subsidiary; its user data, revenues, and expenses are fully consolidated into Meta’s financial statements, though the brand is maintained separately.

Moody’s → Berkshire Hathaway

Warren Buffett’s Berkshire Hathaway holds roughly 13% of Moody’s Corporation below the 20% threshold, treating it as a passive investment. If Berkshire crossed 20%, Moody’s would qualify as an affiliate requiring equity method accounting.

When to Choose Subsidiary vs Affiliate Structure

The decision to structure an intercompany relationship as a subsidiary or affiliate is rarely arbitrary. It is driven by strategic intent, capital availability, risk appetite, and regulatory considerations.

Choose a Subsidiary Structure When:

- You need operational control to execute a unified business strategy (e.g., integrating supply chains, technology platforms, or customer data)

- The target entity is central to your core business and you want to capture 100% of its value creation

- You plan to fund the entity’s expansion with intercompany loans or equity injections

- Tax consolidation or intra-group financing efficiencies are material to the business case

- Regulatory approval requirements are manageable

Choose an Affiliate / Associate Structure When:

- You want strategic access or market intelligence without full integration (e.g., entering a new geography through a local partner)

- The target company’s independent management and culture are key to its success and should be preserved

- You want to limit liability exposure in a high-risk market or industry

- Capital constraints prevent acquisition of a majority stake

- Regulatory restrictions cap foreign ownership below 50% (common in media, aviation, and financial services in many countries)

It All Comes Down to Control

A subsidiary is a company you control; an affiliate is a company you influence. That single distinction cascades into profoundly different accounting methods, legal liability profiles, tax treatments, and strategic implications. The 50% ownership threshold is the conventional bright line, but always layer in the qualitative analysis of actual control, especially in complex cross-holding structures, joint ventures with special voting rights, or VIE arrangements under US GAAP.

Frequently Asked Questions

What is the main difference between a subsidiary and an affiliate? ▾

A subsidiary is a company in which the parent holds more than 50% of voting shares, giving it majority control over governance and operations. An affiliate is a company where the parent holds a minority stake typically between 20% and 50%, giving it significant influence but not outright control. The 50% ownership threshold is the conventional dividing line, though qualitative control factors also matter under IFRS 10 and US GAAP ASC 810.

Is a subsidiary always 100% owned by the parent company? ▾

No. A subsidiary only requires that the parent company owns more than 50% of its voting shares. A wholly-owned subsidiary is one where the parent holds 100%, but a company with 51% or 75% ownership in another entity also qualifies the latter as a subsidiary. The remaining shares are held by non-controlling interest (NCI) shareholders, whose stake must be separately disclosed in consolidated financial statements.

Are subsidiary financials consolidated with the parent company? ▾

Yes. Under IFRS 10 and US GAAP ASC 810, subsidiaries are fully consolidated into the parent’s financial statements. Every line of the subsidiary’s balance sheet and income statement is combined with the parent’s. Intercompany transactions are eliminated to prevent double-counting. Affiliate investments, on the other hand, are accounted for using the equity method under IAS 28 or ASC 323, appearing as a single-line item on the balance sheet.

Can an affiliate become a subsidiary? ▾

Yes. If a parent company increases its ownership stake in an affiliate above 50%, the affiliate transitions into a subsidiary and the parent must begin consolidating its financials. This is a significant event that triggers a step acquisition accounting treatment, the previously held equity interest is remeasured to fair value at the acquisition date, with any resulting gain or loss recognized in profit or loss.

What is the liability difference between a subsidiary and an affiliate? ▾

Because a subsidiary is controlled by the parent, courts in some jurisdictions can pierce the corporate veil and hold the parent liable for the subsidiary’s obligations, particularly if the parent commingles funds, fails to maintain corporate formalities, or operates the subsidiary as a mere extension of itself. Additionally, parents often provide guarantees for subsidiary debt. With affiliates, the parent’s liability is generally limited to the value of its investment, since it lacks operational control and management authority.

What is the difference between an affiliate and an associate company? ▾

The terms are largely interchangeable, but there is a technical distinction. Under IFRS (IAS 28), the formal term is associate, defined as an entity over which the investor has significant influence (typically 20–50% ownership). In US GAAP and common business parlance, the same relationship is often called an affiliate. In casual usage, “affiliate” is also used more broadly to describe any related company including subsidiaries, so context matters when interpreting the term.

Can two companies both be affiliates of each other? ▾

Yes, in common parlance, companies that share a common parent or investor are referred to as sister companies or affiliated companies. For example, if Company X owns 30% of both Company A and Company B, then A and B are affiliates of Company X and are affiliated with each other. Under formal accounting standards, however, each relationship is evaluated separately based on ownership percentage and control indicators.

(Qualified) Chartered Accountant – ICAP

Master of Commerce – HEC, Pakistan

Bachelor of Accounting (Honours) – AeU, Malaysia