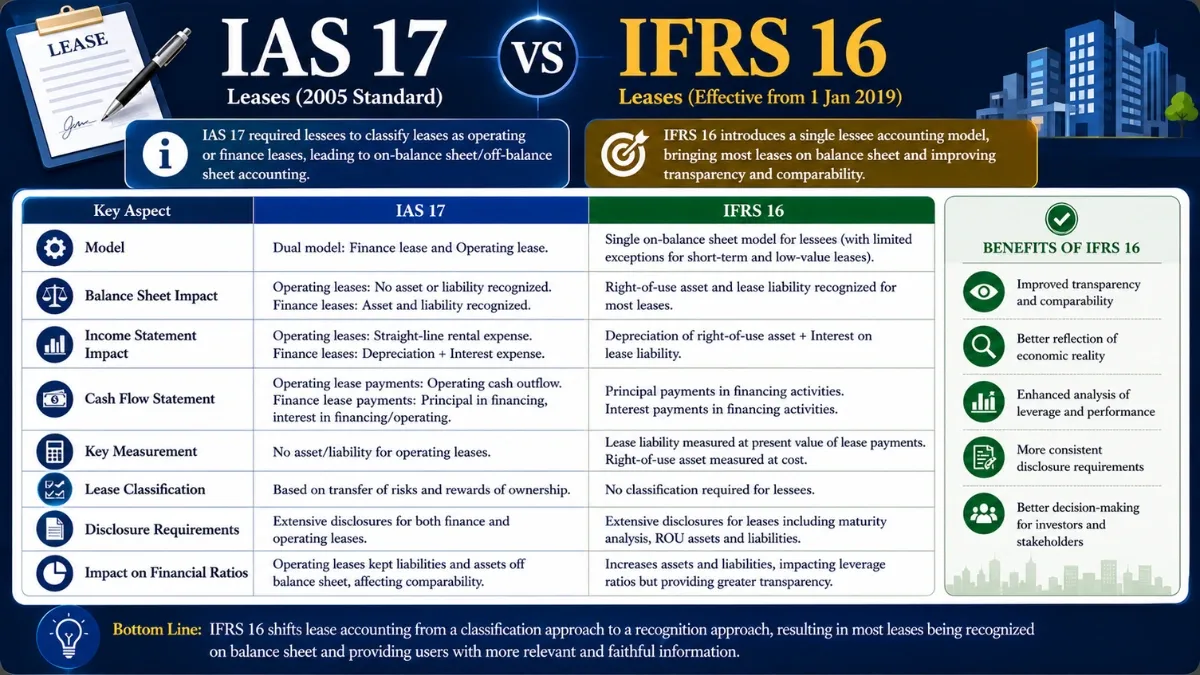

IAS 17 vs IFRS 16: Key Differences in Lease Accounting

IAS 17 vs IFRS 16 a concept that relates to leasing. IAS 17 is the International Accounting Standard (IAS) for leases that was issued by the International Accounting Standards Board (IASB) in 1982, while IFRS 16 is the new leasing standard that was issued by the IASB in 2016. Entrepreneurial … Read More