IFRS 15 promulgated by the International Accounting Standards Board (IASB) provides guidance on accounting for ‘Revenue from Contracts with Customers’. It was adopted in 2014 and became effective in January 2018.

IFRS 15 – Revenue from Contracts with Customers

The definitive, comprehensive guide to understanding, applying, and disclosing revenue under IFRS 15, from first principles to complex multi-element arrangements.

What is IFRS 15?

IFRS 15 – Revenue from Contracts with Customers is an International Financial Reporting Standard that establishes a comprehensive, principles-based framework for recognising revenue from contracts with customers. Issued jointly by the IASB and FASB in May 2014, it became effective for annual periods beginning on or after 1 January 2018.

Before IFRS 15, revenue recognition was governed by multiple, sometimes inconsistent standards including IAS 18 Revenue, IAS 11 Construction Contracts, and numerous industry-specific interpretations. IFRS 15 replaced all of these with a single, unified 5-step model, bringing significantly greater comparability and transparency to financial statements worldwide.

An entity shall recognise revenue to depict the transfer of promised goods or services to customers in an amount that reflects the consideration to which the entity expects to be entitled in exchange for those goods or services.

Why IFRS 15 Matters

Revenue is one of the most important metrics used by investors, analysts, and regulators to assess an entity’s financial performance. Inconsistencies in how revenue was previously recognised, especially in industries like software, construction, and telecommunications led to reduced comparability and, in some cases, accounting manipulation. IFRS 15 addresses this by requiring entities to apply a consistent, judgment-based model aligned with the economics of each transaction.

- Multiple fragmented standards

- Industry-specific guidance

- Risk & reward model (goods)

- Stage of completion (services)

- Limited variable consideration guidance

- Minimal disclosure requirements

- Single, unified 5-step model

- Consistent across all industries

- Performance obligation approach

- Over time or point in time

- Robust variable consideration guidance

- Extensive, disaggregated disclosures

Scope & Applicability of IFRS 15

IFRS 15 applies to all contracts with customers, with specific exceptions. Understanding the scope is crucial before applying the 5-step model.

✅ Within Scope

- Contracts with customers for goods or services

- Revenue from sale of goods

- Rendering of services

- Software licences and subscriptions

- Construction and long-term contracts

- Royalties from intellectual property

- Franchise fees

❌ Outside Scope

- Lease contracts (IFRS 16)

- Insurance contracts (IFRS 17)

- Financial instruments (IFRS 9)

- Non-monetary exchanges between entities in the same line of business

- Certain guarantees (IAS 32 / IFRS 9)

- Collaborative arrangements (not a customer)

Who is a “Customer”?

A customer is a party that has contracted with an entity to obtain goods or services that are an output of the entity’s ordinary activities in exchange for consideration. This distinction matters, collaborative partners sharing in risks and rewards of a project may not be customers under IFRS 15.

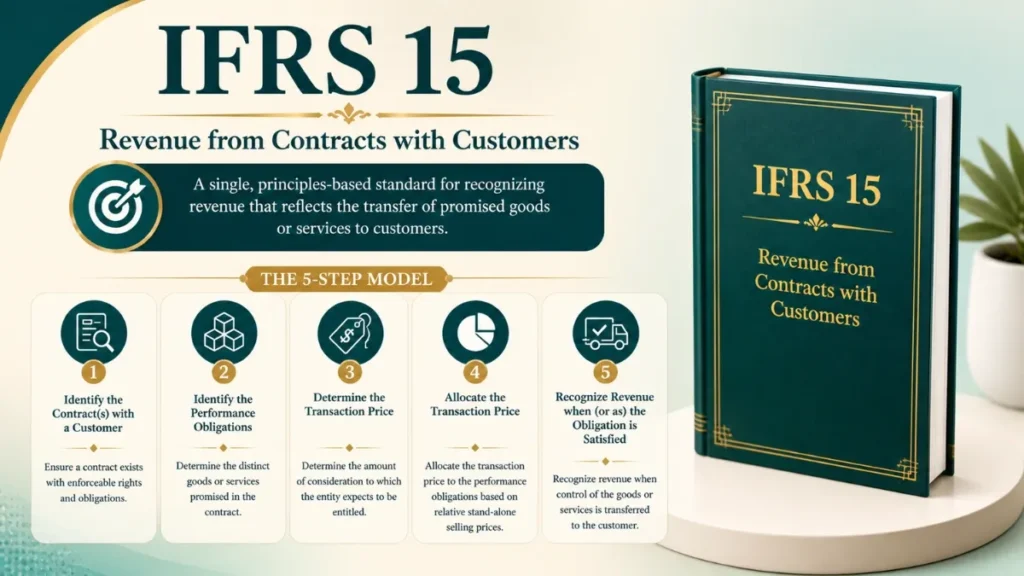

IFRS 15 5 Step Revenue Recognition Model

At the heart of IFRS 15 is a sequential five-step revenue recognition model. Each step must be completed before the next is applied. This model ensures that revenue reflects the actual transfer of economic benefits to the customer.

Identify the Contract

Determine whether a valid contract with a customer exists by meeting all five criteria.

Identify Performance Obligations

Identify each distinct promise to transfer goods or services within the contract.

Determine Transaction Price

Establish the total consideration expected in exchange for fulfilling obligations.

Allocate Transaction Price

Allocate the price to each performance obligation based on relative stand-alone selling prices.

Recognise Revenue

Recognise revenue when (or as) each performance obligation is satisfied.

Identify the Contract with a Customer

A contract is an agreement between two or more parties that creates enforceable rights and obligations. IFRS 15 specifies five criteria that must all be met for a contract to exist:

- Approval and Commitment: The parties have approved the contract and are committed to performing their obligations.

- Rights Identified: Each party’s rights regarding the goods or services to be transferred can be identified.

- Payment Terms: The payment terms for the goods or services to be transferred can be identified.

- Commercial Substance: The contract has commercial substance; the risk, timing, or amount of future cash flows is expected to change.

- Probable Collection: It is probable that the entity will collect the consideration to which it will be entitled.

Contract Modifications Under IFRS 15

A contract modification is a change in the scope or price (or both) of a contract that is approved by the parties. It should be accounted for as:

New Separate Contract

When the modification adds distinct promised goods or services and the price increases by an amount that reflects their stand-alone selling price.

Modification of Existing Contract

Treated as either a termination of the original contract and creation of a new one, or as a continuation depending on whether remaining goods/services are distinct.

Contract Combination

Entities must combine two or more contracts entered into at or near the same time with the same customer if: the contracts are negotiated as a package, consideration in one contract depends on the other, or the goods/services are a single performance obligation.

Identify Performance Obligations

A performance obligation is a promise in a contract with a customer to transfer either a good or service (or bundle) that is distinct, or a series of distinct goods/services that are substantially the same and transferred in the same pattern.

What Makes a Good or Service “Distinct”?

A good or service is distinct if it meets both of the following criteria:

- Capable of being distinct: The customer can benefit from the good or service on its own or together with other readily available resources.

- Distinct within the context of the contract: The promise to transfer the good or service is separately identifiable from other promises in the contract.

A software company sells a software licence, one year of support, and one year of updates for a single price. The software licence may be distinct (it can function on its own), while support and updates might be considered a single performance obligation if they are highly interrelated and cannot be separated without significant effort.

Series of Distinct Goods/Services

A series of distinct goods or services is treated as a single performance obligation if: (1) each distinct good/service in the series is substantially the same, and (2) each distinct good/service has the same pattern of transfer to the customer. This commonly applies to cleaning services, payroll processing, and monthly data hosting.

Determining whether a good or service is “distinct within the context of the contract” requires significant judgement. Indicators include: whether the entity provides a significant integration service, whether the goods/services are highly interrelated, or whether the entity significantly modifies one good or service using another.

Determine the Transaction Price

The transaction price is the amount of consideration to which the entity expects to be entitled in exchange for transferring promised goods or services to a customer, excluding amounts collected on behalf of third parties (e.g., sales taxes).

Key Factors Affecting Transaction Price

| Factor | Description | Key Consideration |

|---|---|---|

| Variable Consideration | Discounts, rebates, refunds, credits, incentives, bonuses, penalties, or price concessions | Estimate using expected value or most likely amount; subject to constraint |

| Significant Financing Component | Contract includes a significant timing difference between payment and performance | Adjust for time value of money using a discount rate that reflects the credit risk |

| Non-cash Consideration | Customer pays with goods, services, or equity instruments | Measure at fair value; variable portions estimated |

| Consideration Payable to Customer | Payments/vouchers/discounts given to customers | Reduce transaction price unless payment is for a distinct good/service |

Significant Financing Component

If the timing of payments agreed upon by the parties provides either party with a significant benefit of financing, the transaction price must be adjusted for the effects of the time value of money. Practical expedient: not required if the period between performance and payment is expected to be one year or less.

IFRS 15 Variable Consideration & the Constraint

Variable consideration is a particularly important and complex area of IFRS 15. An entity estimates variable consideration using the method that better predicts the amount of consideration it will be entitled to:

Expected Value Method

The sum of probability-weighted amounts across a range of possible consideration amounts. Best used when an entity has a large number of contracts with similar characteristics.

Most Likely Amount Method

The single most likely amount in a range of possible outcomes. Best used when a contract has only two possible outcomes (e.g., a bonus is either received or not).

The Variable Consideration Constraint

Variable consideration is included in the transaction price only to the extent that it is highly probable that a significant reversal of cumulative revenue recognised will not occur when uncertainty is resolved. Factors that increase the risk of a revenue reversal include:

A retailer sells 1,000 products for £100 each. Based on historical data, 5% are expected to be returned. Revenue is recognised at £95,000 (950 units × £100). A refund liability of £5,000 and a right-of-return asset are recorded. If the return estimate changes, revenue is adjusted prospectively.

Allocate the Transaction Price to Performance Obligation

When a contract has multiple performance obligations, the transaction price must be allocated to each obligation in a manner that depicts the relative stand-alone selling prices (SSP) of each distinct good or service.

Stand-Alone Selling Price (SSP)

The SSP is the price at which an entity would sell a promised good or service separately to a customer. When directly observable, that price is used. When not observable, entities must estimate using acceptable methods:

| Estimation Method | Description | Best Used When |

|---|---|---|

| Adjusted Market Assessment | Evaluate the market and estimate the price customers would pay | Goods/services with observable market pricing |

| Expected Cost Plus Margin | Forecast costs to satisfy the obligation, add appropriate margin | Services or customised goods |

| Residual Approach | Total transaction price less sum of SSPs of other obligations | Highly variable or uncertain pricing; SSP not directly observable |

Allocation of Discounts

If a discount exists in the contract, it is generally allocated proportionately across all performance obligations. However, the discount may be allocated entirely to one or more obligations if the entity regularly sells those items in a bundle at a discount, and the discounted amount is observable.

Allocation of Variable Consideration

Variable consideration may be allocated entirely to one performance obligation if: (1) the variable terms specifically relate to satisfying that obligation, and (2) the allocation is consistent with the principle of depicting the entity’s performance.

Recognise Revenue When (or As) Performance Obligations Are Satisfied

Revenue is recognised when control of a good or service transfers to the customer, either over time or at a point in time.

Over Time Recognition

A performance obligation is satisfied over time if any of the following criteria are met:

- The customer simultaneously receives and consumes the benefits of the entity’s performance as the entity performs.

- The entity’s performance creates or enhances an asset that the customer controls as the asset is created or enhanced.

- The entity’s performance does not create an asset with an alternative use to the entity, and the entity has an enforceable right to payment for performance completed to date.

Measuring Progress Over Time

For obligations satisfied over time, the entity selects a single method of measuring progress and applies it consistently to similar contracts. Methods include:

Output Methods

Based on value of goods/services transferred to the customer to date relative to remaining goods/services. Examples: surveys of performance, milestones reached, units produced, units delivered.

Input Methods

Based on entity’s efforts or inputs relative to total expected inputs. Examples: costs incurred, labour hours expended, machine hours used. Cost-to-cost is the most common.

Point in Time Recognition

If a performance obligation is not satisfied over time, it is satisfied at a point in time. Indicators that control has transferred include:

A manufacturer bills a customer for goods that remain in the manufacturer’s warehouse at the customer’s request. Revenue may still be recognised if control has transferred: the goods are identified as belonging to the customer, ready for physical transfer, and the entity cannot use them or redirect them elsewhere.

Contract Costs Under IFRS 15

IFRS 15 also addresses the accounting for costs related to contracts with customers.

Costs to Obtain a Contract

Incremental costs of obtaining a contract (e.g., sales commissions that would not be incurred if the contract was not obtained) must be capitalised as an asset if the entity expects to recover them. Practical expedient: expense if amortisation period would be one year or less.

Costs to Fulfil a Contract

Costs directly related to fulfilling a specific contract are capitalised if they: (1) relate directly to a specific contract, (2) generate or enhance resources used to satisfy future obligations, and (3) are expected to be recovered.

Amortisation & Impairment

Capitalised contract costs are amortised on a systematic basis consistent with the transfer of goods/services to which the asset relates. An impairment loss is recognised if the carrying amount exceeds the remaining amount of consideration expected minus remaining costs.

IFRS 15 Disclosure Requirements

IFRS 15 includes some of the most extensive disclosure requirements of any IFRS standard. The objective is to enable users to understand the nature, amount, timing, and uncertainty of revenue and cash flows from contracts with customers.

Quantitative Disclosures

Qualitative Disclosures

Disaggregation of Revenue

Entities must disaggregate revenue into categories that depict how the nature, amount, timing, and uncertainty of revenue and cash flows are affected by economic factors. Common disaggregation dimensions include:

| Dimension | Examples |

|---|---|

| Type of good or service | Product lines, service categories |

| Geographic region | Domestic vs international, by country |

| Market or customer type | Retail, wholesale, government, enterprise |

| Contract type | Fixed price, time and material, milestone-based |

| Duration | Short-term vs long-term contracts |

| Timing of transfer | Point in time vs over time |

| Sales channel | Direct, dealer, online, partner |

Contract Assets vs Contract Liabilities

Contract Asset

An entity’s right to consideration in exchange for goods/services transferred to a customer when that right is conditional on something other than the passage of time (e.g., future performance). Also called “unbilled revenue.”

Contract Liability

An entity’s obligation to transfer goods/services to a customer for which it has received consideration. Previously called “deferred revenue” or “advances from customers.”

Practical Expedients in IFRS 15

IFRS 15 provides several practical expedients to reduce the cost and complexity of applying the standard:

| Expedient | Applies To | Disclosure Required |

|---|---|---|

| Portfolio Approach | Apply the standard to a portfolio of contracts with similar characteristics (rather than each individual contract) | Yes |

| Short-term Contract Costs | Expense costs to obtain contracts with amortisation period of one year or less | Yes |

| Significant Financing Component | Ignore financing if expected gap between performance and payment is ≤ 1 year | Yes |

| Remaining Performance Obligations | Omit disclosure if original expected contract duration is ≤ 1 year, or if right to invoice corresponds to performance completed | N/A |

| Sales-based Royalties | Recognise only when the subsequent sale or usage occurs | No |

| Shipping and Handling | Treat as a fulfilment activity (not a separate performance obligation) if occurring before or after control transfers | Yes |

Transition to IFRS 15

Entities could adopt IFRS 15 using one of two transition methods:

Full Retrospective Method

Apply the standard to all prior periods presented, restating comparatives. Cumulative effect recognised at the beginning of the earliest comparative period. Provides most comparable information but is most costly.

Modified Retrospective Method

Apply IFRS 15 only to contracts not yet complete at the date of initial application. Cumulative effect as an adjustment to opening retained earnings. No restatement of comparative periods. Most commonly adopted.

Transition Timeline

Standard Issued

IFRS 15 published jointly by IASB and FASB in May 2014, converging revenue recognition frameworks.

Clarifications Issued

Clarifications to IFRS 15 issued addressing identifying performance obligations, principal vs agent considerations, and licensing.

Mandatory Effective Date

IFRS 15 became mandatory for annual reporting periods beginning on or after 1 January 2018.

Ongoing Application & Guidance

IASB and preparers continue to develop guidance on complex areas including variable consideration, licensing, and agent/principal arrangements.

Industry-Specific Applications of IFRS 15

While IFRS 15 applies across all industries, its impact varies significantly by sector. Here are the key considerations for major industries:

Software & Technology

Licence vs service distinction, software-as-a-service vs on-premise, bundled vs unbundled arrangements, usage-based royalties, and renewal options.

Construction & Real Estate

Over-time recognition for construction, developer sales (control of apartments), variable consideration in contract modifications, and customisation services.

Telecommunications

Multi-element arrangements (handset + service), subsidised handsets, customer loyalty programmes, contract modifications upon upgrades.

Pharmaceuticals & Life Sciences

Licensing of intellectual property, milestone payments, upfront fees in research collaborations, variable consideration constraints.

Aerospace & Defence

Long-term contracts, bill-and-hold, variable consideration (cost escalation clauses), contract modifications, and incentive fees.

Automotive

Dealer network as agent or principal, warranty provisions, incentive programmes, sale-and-repurchase agreements, and fleet arrangements.

Retail & Consumer Goods

Rights of return, loyalty programmes, gift cards (breakage), consignment arrangements, and slotting fees.

Financial Services

Asset management fees, performance fees, insurance distribution, interchange fees, and financial advisory services.

Education

Tuition revenue recognition, scholarship offsets, online vs in-person modules, and refund policies.

Principal vs Agent Considerations

When an entity is involved in providing goods or services to a customer along with another party, it must determine whether it is acting as a principal (recognises gross revenue) or an agent (recognises only the net fee or commission).

Principal Indicators

- Controls the good/service before transfer

- Inventory risk (before or after delivery)

- Discretion in establishing pricing

- Primary responsibility for fulfilment

Agent Indicators

- Another party controls the good/service

- No inventory or credit risk

- Earns a commission or fee

- Acts on behalf of another party

An online marketplace charges sellers a platform fee of 15% on each sale. If the marketplace never takes control of the inventory (the seller ships directly to the buyer), the marketplace is an agent and should recognise only the 15% fee as revenue — not the gross transaction value.

IFRS 15 vs ASC 606 (US GAAP)

IFRS 15 and ASC 606 (Topic 606) were developed jointly and are substantially converged. However, several differences remain:

| Area | IFRS 15 | ASC 606 (US GAAP) |

|---|---|---|

| Licences | Functional vs symbolic distinction | Same framework, but more application guidance |

| Sales with right of return | Same model | Same model |

| Interim disclosures | Less prescriptive | More prescriptive (ASC 270) |

| Collectability threshold | “Probable” | “Probable” (interpreted differently ~80% vs 75%) |

| Contract costs | No industry-specific exceptions | Some exceptions for brokers/dealers, insurance |

| Presentation of taxes | Guidance less specific | More specific guidance exists |

The Core Objective of IFRS 15

Recognise revenue in a way that faithfully depicts the transfer of goods or services and the consideration an entity expects to receive; creating transparency, comparability, and investor confidence across all industries and geographies.

Frequently Asked Questions

A trade receivable is an unconditional right to receive consideration, only the passage of time is required before payment is due. A contract asset is a conditional right, the entity must perform further obligations before it has the right to payment. Both are recognised on the balance sheet but presented separately.

It depends on whether the licence is functional (right to use IP as it exists at a point in time, recognised at a point in time) or symbolic (right to access IP as it evolves over time, recognised over the licence period). A software licence is typically functional and recognised at the point the customer can use and benefit from it.

Loyalty points that provide a material right to the customer are treated as a separate performance obligation. A portion of the transaction price is allocated to the points based on their stand-alone selling price (considering expected redemption rates). Revenue for the points is deferred and recognised when points are redeemed or expire.

Rather than applying IFRS 15 to each individual contract, an entity can apply it to a portfolio of contracts with similar characteristics if the outcome would not differ materially from applying the standard individually. This is common for entities with high volumes of homogeneous contracts (e.g., retail, subscriptions).

Generally, no. Non-monetary exchanges between entities in the same line of business to facilitate sales to customers are outside the scope of IFRS 15. However, if non-cash consideration is received from a customer, it is measured at fair value.

A contract modification is approved by both parties and changes the scope or price. If the modification adds distinct goods/services at their SSP, it is a new separate contract. Otherwise it is a modification of the existing contract, treated as either a termination and creation of a new contract (prospective), or a continuation (cumulative catch-up adjustment), depending on whether remaining goods/services are distinct.

Entities must disclose the aggregate amount of transaction price allocated to performance obligations that are unsatisfied (or partially unsatisfied) at the reporting date, along with the expected timing of recognition. Exceptions apply for contracts with durations ≤ 1 year, variable consideration subject to the constraint, and practical expedients elected for right-to-invoice situations.

IFRS 15 Summary & Key Takeaways

IFRS 15 represents a landmark shift in how revenue is recognised globally. Its principles-based, contract-centric approach requires significant judgement and robust internal processes, but provides vastly improved transparency for users of financial statements.

- Apply the 5-step model sequentially to every revenue contract.

- Carefully identify distinct performance obligations, this drives the entire accounting.

- Use the highly probable constraint when estimating variable consideration.

- Use observable SSPs wherever possible; estimate only when necessary.

- Distinguish carefully between over-time and point-in-time recognition, it has major P&L implications.

- Fulfil extensive disclosure requirements to ensure financial statement users understand the revenue story.

- Document judgements, estimates, and policies thoroughly for audit readiness.

(Qualified) Chartered Accountant – ICAP

Master of Commerce – HEC, Pakistan

Bachelor of Accounting (Honours) – AeU, Malaysia