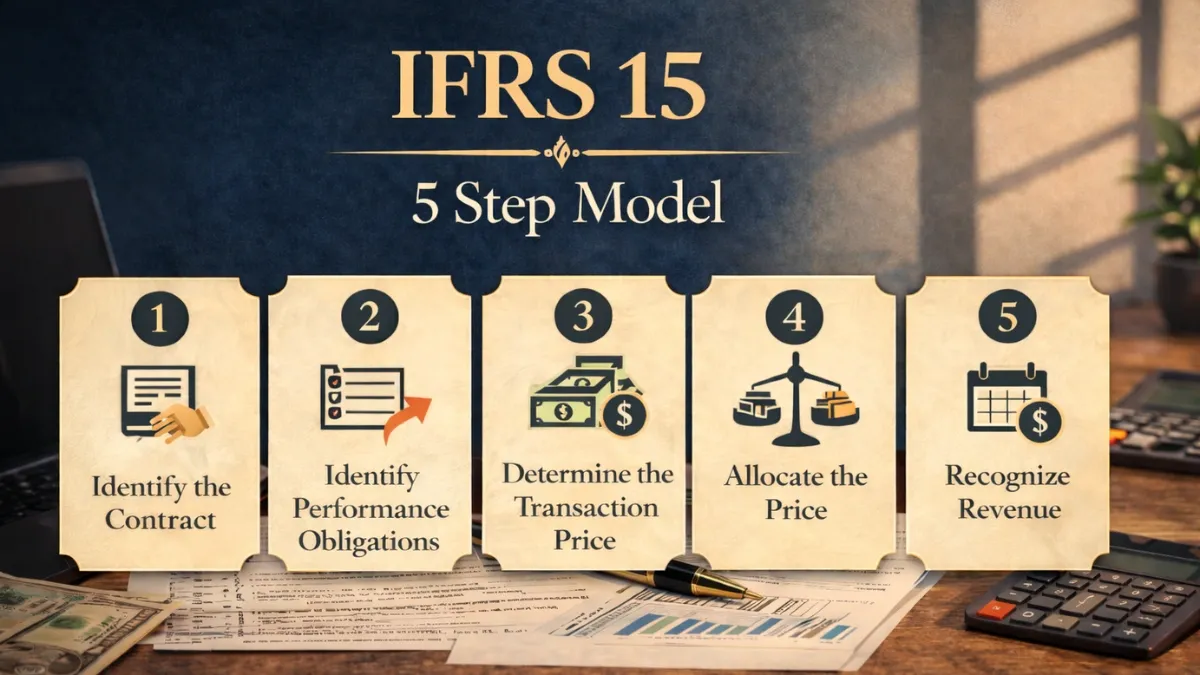

IFRS 15 – Revenue from Contracts with Customers

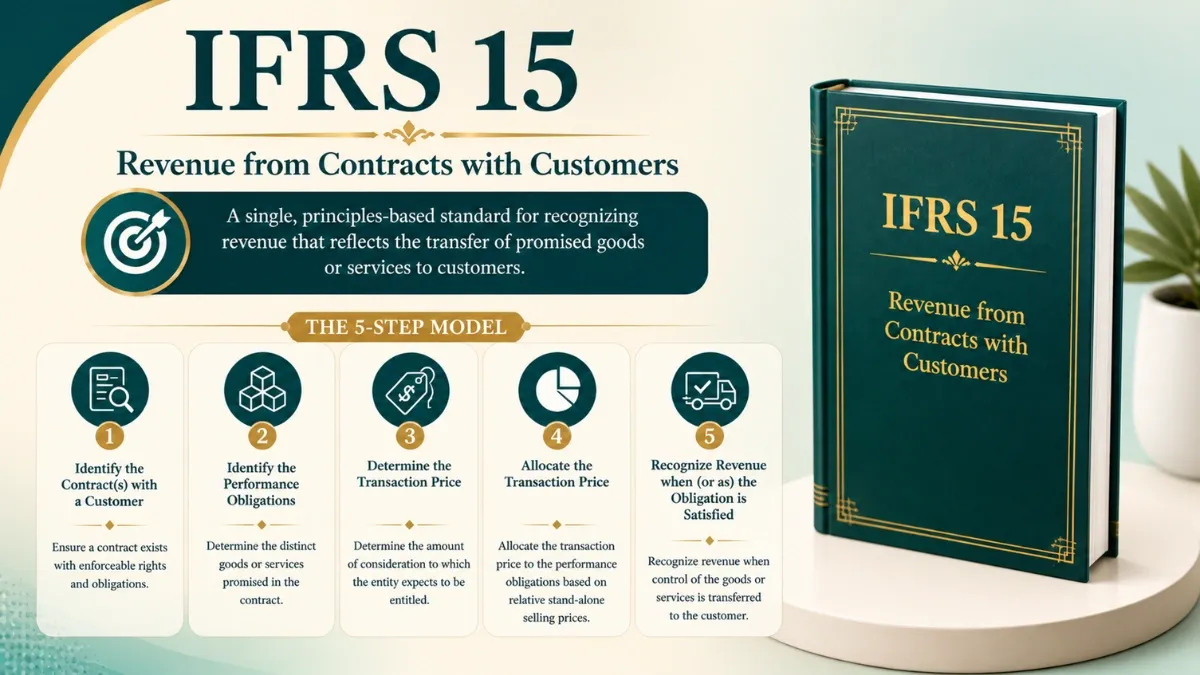

IFRS 15 promulgated by the International Accounting Standards Board (IASB) provides guidance on accounting for ‘Revenue from Contracts with Customers’. It was adopted in 2014 and became effective in January 2018. IFRS Standard · Revenue Recognition IFRS 15 – Revenue from Contracts with Customers The definitive, comprehensive guide to understanding, … Read More