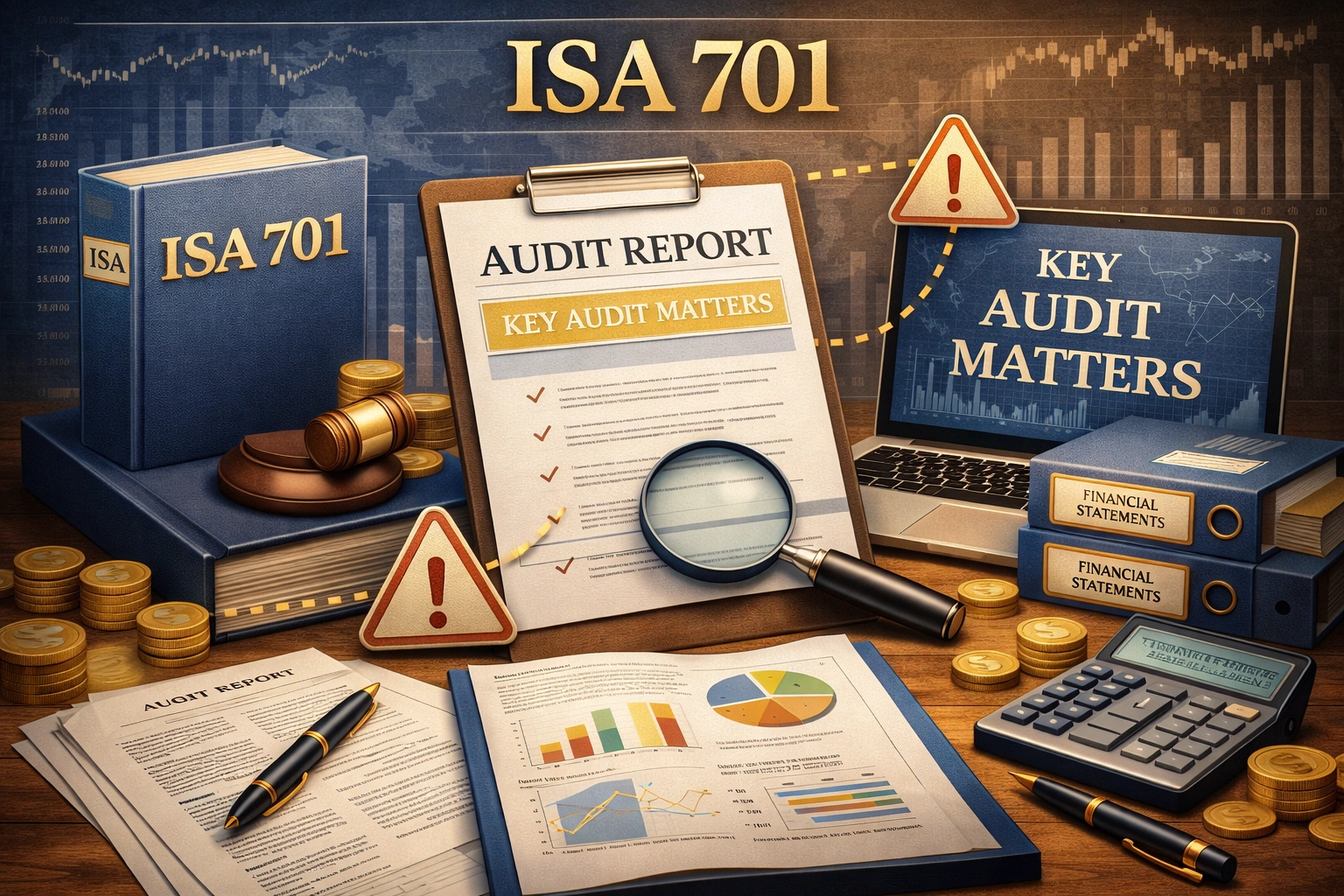

ISA 705 (Revised) – Modifications to the Opinion in the Independent Auditor’s Report

ISA 705 (Revised) deals with the auditor’s responsibility to issue an appropriate report in circumstances when in forming an opinion in accordance with ISA 700 (Revised), the auditor concludes that a ‘modification’ to the auditor’s opinion on the financial statements is necessary. International Standards on Auditing | IAASB ISA 705 … Read More