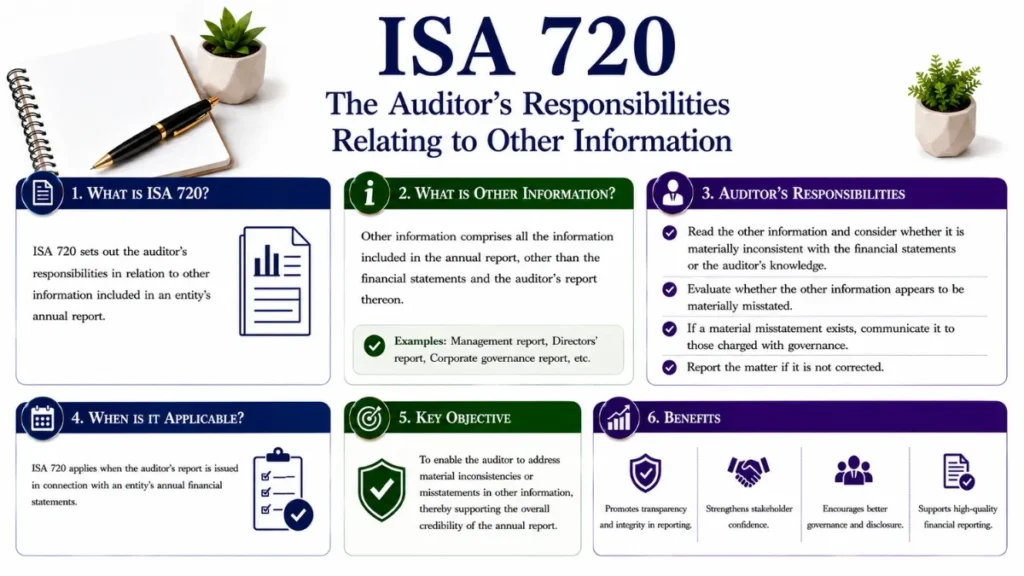

ISA 720 (Revised) deals with the auditor’s responsibilities relating to other information, whether financial or non-financial information (other than ‘financial statements‘ and the ‘auditor’s report‘ thereon) included in an entity’s annual report.

ISA 720 – The Auditor’s Responsibility Relating to Other Information

A definitive guide to the auditor’s obligations when reading and reporting on documents containing audited financial statements

ISA 720 stands as one of the most practically significant yet often underestimated standards in the auditor’s toolkit. It governs the auditor’s responsibilities for information beyond the audited financial statements, the broader narrative that surrounds those numbers. Understanding ISA 720 is essential not just for compliance, but for protecting the integrity of the entire annual reporting process.

What Is ISA 720?

ISA 720, formally titled “The Auditor’s Responsibilities Relating to Other Information,” is an International Standard on Auditing issued by the International Auditing and Assurance Standards Board (IAASB).

In today’s corporate reporting landscape, annual reports routinely include the chairman’s statement, management commentary, operational reviews, sustainability disclosures, corporate governance reports, remuneration reports, and much more. Collectively, these form the “other information” that surrounds the audited financials. While none of these are audited in the same way as financial statements, they can create a materially misleading impression if they contradict or are inconsistent with the audited numbers.

The IAASB revised ISA 720 in 2015 because stakeholders and regulators recognised that auditors were reading other information in annual reports but had limited, inconsistent obligations to report on what they found. The revised standard introduced far more prescriptive requirements and a new mandatory section in the auditor’s report.

— IAASB, Revised ISA 720 (2015)The current version of ISA 720 became effective for audits of financial statements for periods ending on or after December 15, 2016. Many jurisdictions adopted it for earlier periods. In the UK and Ireland, the equivalent standard is ISA (UK) 720, which carries additional requirements specific to that regulatory environment.

Objective of ISA 720

The objective of ISA 720 is clearly stated within the standard itself. The auditor’s goal is to:

It is critical to understand what this objective does not include. The auditor is not required to verify the accuracy of every statement in the annual report, nor to express a positive opinion on the other information. The standard is calibrated around a reading-and-responding obligation, not an assurance obligation.

This distinction is deliberate. Other information is often narrative, forward-looking and qualitative in nature, characteristics that make it difficult to audit in the same way financial figures are audited. ISA 720 therefore threads a practical needle: it imposes meaningful scrutiny without requiring the auditor to take full responsibility for all non-financial disclosures.

What is Other Information?

The term “other information” has a precise meaning under ISA 720. It refers to financial or non-financial information included in an entity’s annual report, other than the audited financial statements and the auditor’s report thereon.

Common Examples of Other Information

Directors’ / Management Report

The statutory management commentary covering business performance, strategy, and principal risks.

Chairman’s Statement

Narrative commentary from the board chair on company performance and future outlook.

Non-GAAP Financial Measures

Alternative performance measures such as adjusted EBITDA, underlying profit, or like-for-like revenue.

Corporate Governance Report

Disclosures on board composition, committee activities, and compliance with governance codes.

Sustainability / ESG Report

Environmental, social, and governance disclosures included within the annual report document.

Remuneration Report

Disclosures of director remuneration, pay ratios, and remuneration policy.

ISA 720 applies only to other information obtained or expected to be obtained prior to the date of the auditor’s report. Information published only after the auditor’s report date falls outside its scope but may be addressed under ISA 560 (Subsequent Events).

What is NOT Other Information?

Not all documents accompanying financial statements fall within the scope of ISA 720. The standard explicitly excludes:

- The audited financial statements themselves

- The auditor’s report on those financial statements

- A predecessor auditor’s report

- Regulatory filings that contain only the financial statements and auditor’s report (e.g., a stand-alone statutory filing without narrative commentary)

- Information published separately from the annual report (unless the entity treats them as a single document)

Scope & Applicability of ISA 720

ISA 720 applies when the auditor’s audit engagement covers financial statements included within an annual report, a document (or combination of documents) that contains audited financial statements and the auditor’s report thereon, along with other information.

The standard’s applicability is triggered by the nature of the document, not the type of entity. It applies to:

- Listed companies with obligations to publish full annual reports

- Public interest entities (PIEs) under local regulation

- Private entities that voluntarily produce documents meeting the definition of an annual report

- Not-for-profit and government entities, where local standards or ISA adoption requirements apply

Where an entity does not produce an annual report for example, a small private company that files only statutory accounts and an auditor’s report (ISA 720 may not apply), or its application may be limited in scope. Auditors must exercise professional judgement in borderline cases.

National versions of ISA 720 such as ISA (UK) 720, ISA (IE) 720, or standards issued by the PCAOB in the United States may impose additional requirements beyond the base IAASB standard. Always consult the applicable national standard.

Key Requirements Under ISA 720

ISA 720 imposes a structured set of requirements on auditors. These fall into three broad categories: obtaining other information, reading and considering it, and responding to what is found.

Obtaining the Other Information

The auditor must make arrangements with management to obtain, before the date of the auditor’s report, the final or substantially complete version of the annual report. This is an active duty, the auditor should not wait passively for documents to be delivered. Where the entire annual report is not available before the auditor’s report date, the auditor obtains the available portions and addresses any remaining portions as soon as practicable after the report date.

Reading and Considering Other Information

The auditor reads the other information to identify:

- Material inconsistencies with the audited financial statements

- Material inconsistencies with the auditor’s knowledge obtained during the audit

- Apparent misstatements of fact – information that appears to be incorrectly stated regardless of the financial statements

Understanding the Annual Report

The auditor should develop an understanding of the purpose and context of the annual report. This helps calibrate what a reasonably informed reader would expect, which in turn helps the auditor judge materiality in the context of other information, a concept that can be more nuanced than financial statement materiality.

Auditor Procedures Required by ISA 720: Step-by-Step

The following outlines the practical workflow an auditor follows in applying ISA 720 during an engagement.

Identify the Annual Report and Obtain Other Information

Determine which documents constitute the annual report. Communicate with management early in the engagement to obtain the final version before signing the auditor’s report. Where only draft versions are available, arrange to review the final version promptly.

Read Other Information in Its Entirety

Read all sections of the other information carefully. This is a reading exercise, not a re-audit of the underlying data. The auditor applies the knowledge gained throughout the audit engagement to assess what is read.

Identify Material Inconsistencies

Consider whether financial data, statistics, or factual claims in the other information are consistent with amounts, disclosures, and knowledge obtained during the audit. Pay particular attention to non-GAAP measures, segment data, and key performance indicators.

Identify Apparent Misstatements of Fact

Look beyond the financial statements for information that appears to be factually incorrect or misleading in itself. This requires professional judgement and awareness of the business, sector, and publicly available information.

Communicate with Management

If a material inconsistency or apparent misstatement is identified, bring it to management’s attention. Management must be given the opportunity to explain or correct the matter before the auditor takes further action.

Respond Based on Management’s Action or Inaction

If management corrects the issue, the matter is resolved. If they refuse, the auditor considers the implications for the auditor’s report and documents their conclusions. In extreme circumstances, the auditor may consider withdrawing from the engagement.

Include a Separate Section in the Auditor’s Report

Under the revised ISA 720, the auditor must include an “Other Information” section in the audit report. This section states management’s responsibility for other information, the auditor’s obligations, and any matters arising.

Material Inconsistencies and Misstatements of Fact

Two key concepts lie at the heart of ISA 720 and understanding their distinction is essential for effective application.

Material Inconsistency

A material inconsistency occurs when other information contradicts information contained in the audited financial statements, or contradicts knowledge the auditor obtained during the audit. For example:

- The chairman’s statement claims a 15% increase in operating profit, but the audited financial statements show a 5% increase

- The directors’ report describes a significant litigation matter as resolved, but the auditor’s knowledge indicates it remains outstanding

- A KPI summary states zero employee fatalities, but the auditor is aware of a workplace fatality disclosed elsewhere in the notes

Misstatement of Fact

A misstatement of fact is other information that is incorrectly stated. It may not necessarily be inconsistent with the financial statements, it may simply be factually wrong in itself. For example, stating that the company was founded in 1978 when it was actually incorporated in 1989, or misquoting a regulatory threshold. The auditor is not required to verify all factual claims exhaustively, but apparent errors noted during reading must be addressed.

Materiality in the Context of Other Information

Materiality under ISA 720 is not the same as the quantitative financial statement materiality threshold established under ISA 320 (Materiality in Planning and Performing an Audit). When assessing whether an inconsistency or misstatement is material, the auditor considers:

- Whether it could reasonably be expected to influence the economic decisions of users of the annual report

- The context in which it appears and the prominence given to it

- Whether the information is qualitative or quantitative in nature

- The significance of the item to which the information relates

Alternative performance measures (APMs) or non-GAAP measures are a particularly high-risk area under ISA 720. These figures are unaudited but are often given more prominence than statutory figures. An inconsistency between an APM and its closest audited equivalent can be material even where the absolute difference is small.

Reporting Requirements Under ISA 720

One of the most significant changes introduced by the revised ISA 720 is the requirement to include a dedicated “Other Information” section in every auditor’s report where ISA 720 applies. This section is now a standard feature of long-form audit reports and increases transparency for users.

Content of the Other Information Section

The standard section must contain the following elements:

- Identification of management’s responsibility for the other information

- Identification of the other information (e.g., naming the annual report sections covered)

- A statement that the auditor’s opinion does not cover the other information

- A description of the auditor’s responsibilities: to read, consider, and report material inconsistencies

- A statement of the outcome – confirming that nothing material has come to the auditor’s attention, or describing any unresolved material matters

Outcome Scenarios and Reporting Language

| Scenario | Auditor’s Response | Effect on Report |

|---|---|---|

| No material inconsistencies found | Standard closing statement in Other Information section | Clean report; standard language |

| Material inconsistency found; management corrects it | Matter resolved; no further reporting required | Clean report |

| Material inconsistency found; management refuses to correct | Describe inconsistency in Other Information section | Modified Other Information section |

| Material inconsistency that also casts doubt on financial statements | Consider implications under ISA 700; may modify audit opinion | Potentially modified opinion |

| Apparent misstatement of fact; management corrects it | Matter resolved | Clean report |

| Apparent misstatement of fact; management refuses to correct | Describe in Other Information section; consider withdrawal | Modified Other Information section |

Sample Auditor’s Report Language for Other Information

The following illustrates the typical language used in an auditor’s report where no material inconsistencies have been identified, the most common outcome in practice.

Other Information

The directors are responsible for the other information. The other information comprises the information included in the Annual Report, other than the financial statements and our auditor’s report thereon.

Our opinion on the financial statements does not cover the other information and, except to the extent otherwise explicitly stated in our report, we do not express any form of assurance conclusion thereon.

In connection with our audit of the financial statements, our responsibility is to read the other information and, in doing so, consider whether the other information is materially inconsistent with the financial statements or our knowledge obtained in the audit or otherwise appears to be materially misstated.

If we identify such material inconsistencies or apparent material misstatements, we are required to determine whether this gives rise to a material misstatement in the financial statements themselves. If, based on the work we have performed, we conclude that there is a material misstatement of this other information, we are required to report that fact.

We have nothing to report in this regard.

The final line “We have nothing to report in this regard” is the standard clean conclusion. Where a material inconsistency exists and is unresolved, that sentence is replaced with a description of the specific inconsistency identified.

Pre-2016 vs Revised ISA 720: What Changed?

The 2015 revision of ISA 720 was a substantive overhaul, not a minor update. The table below summarises the most important differences between the original and revised standards.

| Feature | Original ISA 720 | Revised ISA 720 (2016) |

|---|---|---|

| Reporting requirement | No specific section required in auditor’s report | Dedicated “Other Information” section mandatory in auditor’s report |

| Timing of procedures | Read other information; no specific timing requirement | Obtain final or substantially complete version before date of auditor’s report |

| Misstatements of fact | Limited guidance on apparent misstatements of fact | Explicit requirements to identify and respond to apparent misstatements of fact |

| Scope of “annual report” | Less prescriptive definition | Clear definition; examples of inclusions and exclusions provided |

| Management responsibility | Not prominently stated in auditor’s report | Management’s responsibility explicitly stated in Other Information section |

| After-date information | Not specifically addressed | Addresses procedures when other information available only after auditor’s report date |

Practical Challenges in Applying ISA 720

1. Timing Pressures

In many engagements, the annual report is finalised under significant time pressure. Obtaining a substantially complete version before signing the audit report can be difficult when different sections of the annual report are drafted and approved by different parts of the organisation at different times. Effective project management and early communication with the client are essential.

2. Volume of Other Information

Modern annual reports can exceed 200 pages. Reading them in their entirety is resource-intensive. Audit teams must allocate sufficient time and often assign senior staff to this task to ensure that knowledge of the business and the audit findings is brought to bear effectively.

3. Evaluating Alternative Performance Measures

Non-GAAP measures are increasingly prominent in annual reports. Determining whether an APM is consistent with the financial statements requires understanding both the APM’s definition and the reconciliation methodology. Inconsistencies can be subtle for example, a revenue figure that excludes certain items differently than described in the accounting policies.

4. Forward-Looking Statements

Statements about the future; strategic intentions, expected market growth, planned investments are difficult to assess against audited financial information. The auditor is generally not expected to verify prospective information but must remain alert to cases where forward-looking statements directly contradict known facts or going concern assessments.

5. Sustainability and ESG Disclosures

As ESG reporting becomes more extensive and integrated into annual reports, auditors face new challenges under ISA 720. Statements about carbon emissions, water usage, supply chain labour standards, and diversity metrics may be inconsistent with data seen during the audit but are inherently difficult to verify without specialist knowledge. This is an evolving area, and many jurisdictions are developing separate assurance standards for ESG information.

The IAASB’s ongoing work on sustainability assurance including the International Standard on Sustainability Assurance (ISSA) 5000 is expected to supplement ISA 720 for entities with mandatory sustainability reporting requirements in the coming years.

Frequently Asked Questions

No. ISA 720 does not require the auditor to audit, review, or express any form of assurance on other information. The standard requires the auditor to read and consider other information, applying audit knowledge to identify material inconsistencies or apparent misstatements of fact. The auditor’s report explicitly states that the audit opinion does not cover the other information.

If management refuses to amend material inconsistencies or apparent misstatements of fact, the auditor must describe the inconsistency or misstatement in the Other Information section of the auditor’s report. The auditor should also consider whether the unresolved matter casts doubt on the audited financial statements or on the auditor’s opinion thereon. In extreme cases and where permitted by law or regulation, the auditor may consider withdrawing from the engagement.

ISA 720 applies in the context of an audit engagement. It does not apply to review engagements covering interim financial information (which are governed by ISRE 2410). However, where a full audit is performed on interim statements and those statements are published as part of an annual report document, the principles of ISA 720 would be applicable in that context.

ISA 720 and ISA 570 interact where the going concern assessment in the financial statements is inconsistent with narrative disclosures in the annual report. For example, if the financial statements include a material uncertainty related to going concern but the chairman’s statement portrays an unqualifiedly positive outlook without any reference to that uncertainty, the auditor would consider this a potential material inconsistency under ISA 720 requiring discussion with management.

The IAASB’s ISA 720 forms the international baseline, but many countries have adopted national variants with additional requirements. ISA (UK) 720, for instance, includes specific requirements relating to the UK Corporate Governance Code and the Strategic Report, and extends the auditor’s responsibilities to check consistency with the entity’s corporate governance disclosures. Auditors must always apply the version of the standard adopted in their jurisdiction.

ISA 710 deals with comparative information; figures, disclosures, or complete financial statements from prior periods included within the current year’s financial statements. ISA 720 deals with other information; narrative and non-financial content included in the annual report document alongside the financial statements. They address different aspects of corporate reporting and both may apply in the same engagement.

ISA 720 is fundamentally about the credibility of the annual report as a whole. Auditors who apply it rigorously protect both the users of corporate reporting and the integrity of the audit profession. Its requirements are demanding but proportionate (read, consider, and report). The standard does not ask auditors to audit everything; it asks them to bring their professional expertise to bear on the totality of what is published in their name.

— Core Principle of ISA 720

(Qualified) Chartered Accountant – ICAP

Master of Commerce – HEC, Pakistan

Bachelor of Accounting (Honours) – AeU, Malaysia