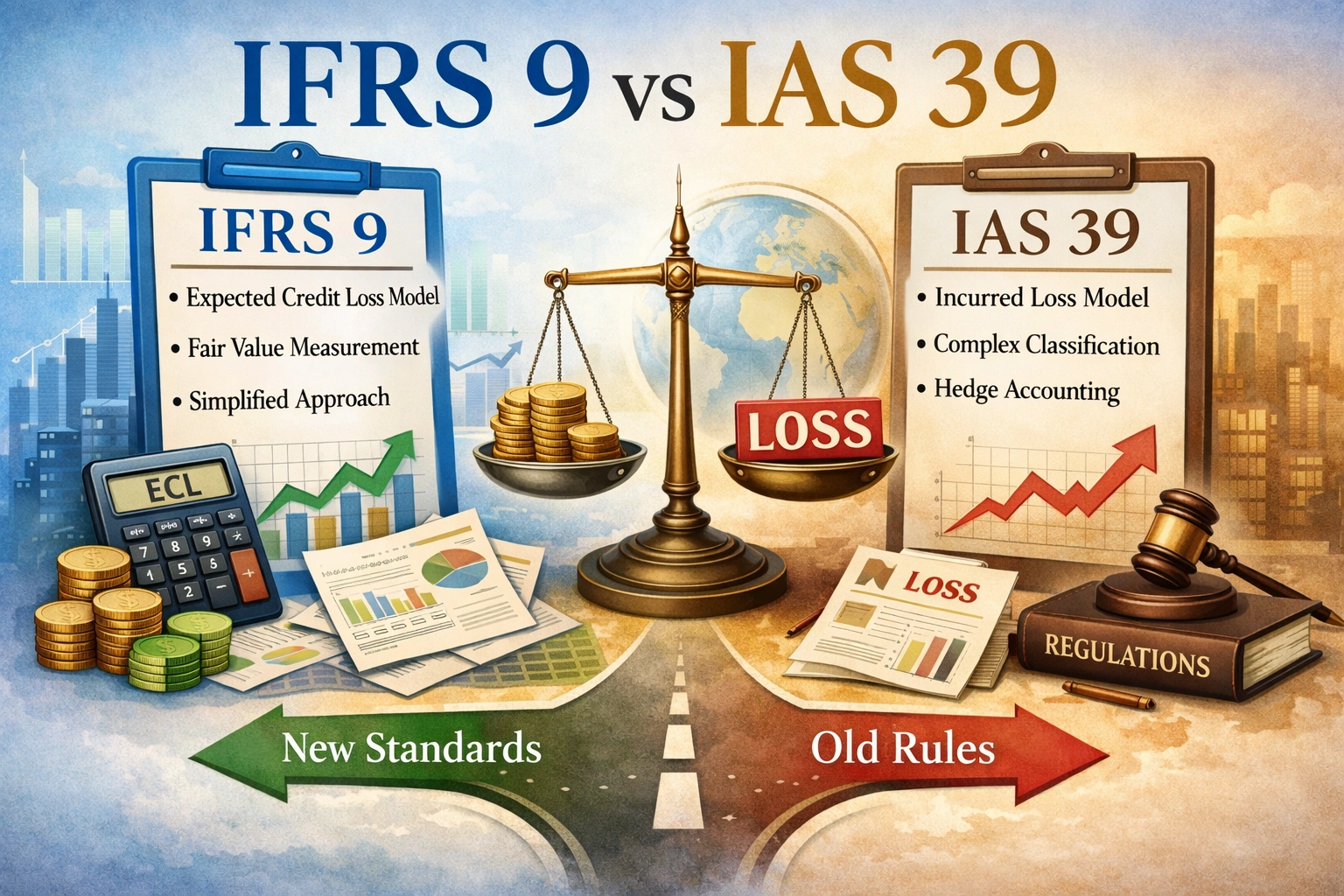

IFRS 9 Vs IAS 39 – Financial Instruments: Key Differences

The One difference amongst Many of IFRS 9 Vs IAS 39 STATES that the key difference is in relation to the approach to ‘IMPAIRMENT’. IFRS 9 uses ‘Expected Credit Losses‘ (ECLs) to recognize impairment losses on financial assets, as compared to IAS 39 ‘Incurred Losses‘. Financial Reporting Standards · Comparative … Read More