ISA 560 deals with the auditor’s responsibilities relating to subsequent events in an ‘audit‘ of financial statements.

ISA 560

Subsequent Events

Overview and Objective of ISA 560

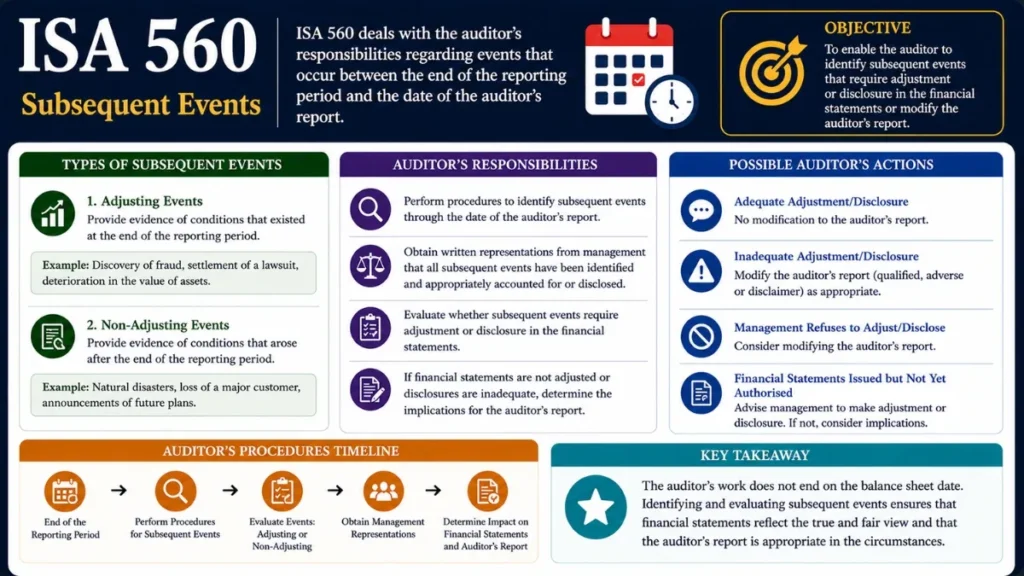

ISA 560 – Subsequent Events is an International Standard on Auditing issued by the IAASB, establishes the auditor’s responsibilities relating to subsequent events, those events occurring after the financial statement date that may materially affect the financial statements and therefore require either adjustment or disclosure.

The standard works in conjunction with IAS 10, Events After the Reporting Period, which governs the accounting treatment, while ISA 560 governs the auditor’s evidence-gathering and reporting obligations.

To obtain sufficient appropriate audit evidence that all subsequent events up to the date of the auditor’s report that require adjustment or disclosure in the financial statements have been appropriately identified and reflected.

Key Definitions Under ISA 560

ISA 560 introduces precise terminology that every auditor must understand. Confusion between these dates is a common source of audit failures.

Types of Subsequent Events: Adjusting vs Non-Adjusting Events

Both ISA 560 and IAS 10 recognise two distinct categories of subsequent events, each triggering a different accounting and audit response.

Conditions Existing at Balance Sheet Date

Events that provide additional evidence of conditions that already existed at the period-end. The financial statements must be adjusted.

- Resolution of litigation that was pending at year-end

- Customer insolvency confirming year-end receivable is irrecoverable

- Discovery of fraud or errors affecting reported figures

- Sale of inventory below cost after year-end, evidencing NRV at period-end

- Final determination of year-end bonus or profit-sharing amounts

Conditions Arising After Balance Sheet Date

Events that are indicative of conditions arising after the period-end. No adjustment is required; disclosure is required if material.

- Major acquisition or disposal of a subsidiary

- Announcement of a restructuring plan

- Significant fire, flood or other disaster

- Issuance of new shares or bonds after year-end

- Abnormally large changes in asset prices or exchange rates

The auditor must carefully distinguish between the two types. Misclassifying a Type 1 event as Type 2 or vice versa can result in materially misstated or inadequately disclosed financial statements, potentially leading to a modified opinion.

Important Dates and Reporting Timeline

Understanding how ISA 560 maps the auditor’s obligations across the audit timeline is essential. Each phase carries distinct responsibilities.

Audit Procedures Under ISA 560

Paragraphs 6–9 of ISA 560 require the auditor to perform specific procedures designed to identify subsequent events up to the date of the auditor’s report. These are not optional, they are mandatory requirements.

“The auditor shall perform audit procedures designed to obtain sufficient appropriate audit evidence that all subsequent events… have been identified.”

ISA 560, Paragraph 6Review the entity’s most recent interim financial statements (whether prepared for internal or external purposes) to identify unusual transactions or significant changes since the balance sheet date.

Read minutes of meetings of owners, management, and those charged with governance held after the balance sheet date. Inquire about matters discussed but not yet minuted.

Make specific inquiries of management (and where appropriate, those charged with governance) about: events that could affect the financial statements, new commitments or borrowings, sales or acquisitions of major assets, changes in share capital, and pending or threatened litigation.

Follow up on items initially assessed as uncertain or provisional at the balance sheet date such as contingent liabilities, going concern indicators, or provisional valuations.

As per ISA 580, obtain a management representation letter dated as of the date of the auditor’s report, confirming that all events subsequent to the balance sheet date that require adjustment or disclosure have been adjusted or disclosed.

If interim financial statements are not available, inspect bank statements, cash receipts/payments journals, and other accounting records for the subsequent period.

Auditor Responsibilities for Facts Discovered After the Auditor’s Report but Before Issuance

Between the date of the auditor’s report (D3) and the date the financial statements are issued (D4), the auditor has no active duty to perform further procedures. However, if the auditor becomes aware of a fact that, had it been known at D3, may have caused the report to be amended, ISA 560 paragraphs 10–12 require specific actions.

The auditor must discuss the matter with management and those charged with governance as per ISA 260 requirements to determine whether the financial statements need amendment.

The auditor performs necessary audit procedures on the amendment, extends subsequent events procedures to the new date, and provides either a new or updated auditor’s report. If the original report is returned and not reissued, a new report is issued with an explanatory paragraph. Dual dating may be used, restricting the extension to the specific amendment only.

The auditor must modify the opinion if the original auditor’s report has not been released to the entity. If it has been released, the auditor notifies management not to issue the statements. If statements are issued regardless, the auditor takes legal advice and considers notifying users.

When the auditor restricts an updated report date to a specific subsequent amendment, the original audit work date is preserved. The dual date format reads: “[Original date], except as to Note X, which is as of [new date].” This limits the auditor’s responsibility to the specific amendment only.

Auditor Responsibilities for Facts Discovered After Financial Statements Are Issued

Once financial statements are issued (after D4), ISA 560 paragraphs 14–17 govern the auditor’s obligations. While the auditor has no duty to perform ongoing procedures, discovered facts cannot be ignored.

| Scenario | Management Responds | Management Does NOT Respond |

|---|---|---|

| New fact discovered post-issuance | Auditor assists management in amending statements, performs procedures on amendments, issues new report. Acceptable | Auditor notifies management not to issue statements. If already issued, notifies management of intent to prevent future reliance. Non-compliant |

| Management issues amended statements | New auditor’s report issued, not dated earlier than the date the amended statements are approved. | Auditor may need to notify regulatory authorities, shareholders, or other users depending on jurisdiction. |

| Regulatory & legal obligations | The auditor may have additional legal obligations, particularly when securities offerings are involved (e.g., a prospectus). ISA 560 notes that auditors may be required to perform procedures to the date of the final offering document. | |

Relationship Between ISA 560 and IAS 10

ISA 560 and IAS 10 are complementary standards, one governs the accounting treatment, the other the audit response. Understanding both is essential for audit professionals and finance teams alike.

| Dimension | IAS 10 | ISA 560 |

|---|---|---|

| Issued by | IASB (International Accounting Standards Board) | IAASB (International Auditing & Assurance Standards Board) |

| Primary audience | Management / Finance teams preparing statements | External auditors reporting on statements |

| Key obligation | Adjust or disclose events after the reporting period | Obtain evidence that adjustments/disclosures are complete and appropriate |

| Type 1 / Adjusting events | Recognise in financial statements | Evaluate whether recognition is appropriate; gather sufficient evidence |

| Type 2 / Non-adjusting events | Disclose if material; do not adjust | Verify disclosure is adequate; consider impact on auditor’s report |

| Cut-off date for obligations | Date financial statements are authorised for issue | Date of auditor’s report (active); date of issuance (passive) |

Frequently Asked Questions

(Qualified) Chartered Accountant – ICAP

Master of Commerce – HEC, Pakistan

Bachelor of Accounting (Honours) – AeU, Malaysia