ISA 710 deals with the auditor’s responsibilities relating to comparative information in an ‘audit‘ of financial statements.

ISA 710 – Comparative Information:

Corresponding Figures & Comparative Financial Statements

A definitive guide for auditors, finance professionals, and students on applying ISA 710 correctly and confidently.

01 Overview of ISA 710

ISA 710 deals with the auditor’s responsibilities regarding comparative information in financial statements, specifically the two forms it may take: corresponding figures and comparative financial statements.

Issued by the International Auditing and Assurance Standards Board (IAASB), ISA 710 – Comparative Information: Corresponding Figures and Comparative Financial Statements establishes how auditors should treat prior period financial data that appears alongside current period information.

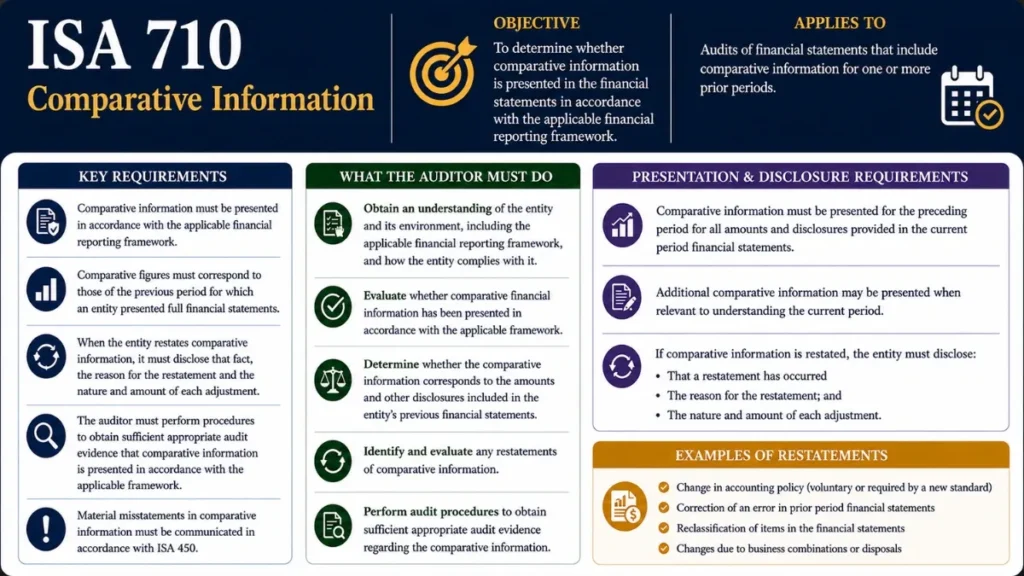

02 Objective and Scope of ISA 710

The objective of ISA 710 is to obtain sufficient appropriate audit evidence about whether the comparative information presented in the financial statements has been appropriately stated, in all material respects, in accordance with the requirements for comparative information in the applicable financial reporting framework.

The standard also addresses how the auditor’s opinion should be expressed given the form of comparative information used in the presentation.

Scope clarification: ISA 710 applies when the financial reporting framework requires or permits comparative information. It does not apply when the entity voluntarily presents supplementary comparative data that falls outside the framework’s requirements, such disclosures are addressed under ISA 720.

Importantly, this ISA deals with audit obligations. It does not prescribe how comparative information must be presented, that responsibility rests with the applicable financial reporting framework (e.g., IFRS, US GAAP).

03 Key Definitions Under ISA 710

Before applying ISA 710, auditors must understand the precise meanings of the key terms used throughout the standard.

04 ISA 710 Approaches to Comparative Information

ISA 710 recognises that financial reporting frameworks differ in how they require prior period data to be presented. The two approaches carry different implications for the auditor’s report.

| Aspect | Corresponding Figures | Comparative Financial Statements |

|---|---|---|

| Presentation | Prior period figures are presented as an integral part of current period statements. They are a reference point, not a separate set of statements. | Prior period statements are presented with equal prominence alongside current period statements, effectively two complete sets of financial statements. |

| Audit Opinion | The audit opinion refers only to the current period. Prior period figures are not separately opined on. | The audit opinion covers both the current and prior period financial statements i.e., two periods are within the opinion’s scope. |

| Common in | Many jurisdictions using IFRS (e.g., UK, EU, most Commonwealth countries) | United States (US GAAP), some other jurisdictions |

| Auditor’s focus | Whether corresponding figures are correctly presented and disclosed in relation to the current period | Whether both periods’ statements present a true and fair view, with potentially separate or combined opinions |

| Level of evidence | Less extensive than a full audit of prior period, focused on material consistency | Substantive evidence required for both periods |

The distinction matters greatly for drafting the auditor’s report and for understanding the extent of audit procedures required.

05 Auditor’s Responsibilities Relating to Corresponding Figures

When financial statements present prior period data as corresponding figures, the auditor’s responsibilities are clearly scoped by ISA 710. The opinion is focused on the current period, but prior period information must not be ignored.

What the Auditor Must Do

Evaluate consistency: Determine whether the corresponding figures agree with the amounts and disclosures presented in the prior period, or have been appropriately restated (e.g., for a change in accounting policy or error correction).

Read prior period financials: Even where the prior period was audited by a predecessor auditor, the current auditor should review the prior year financial statements and the predecessor’s audit report.

Obtain audit evidence: Perform procedures to determine whether material misstatements in corresponding figures exist that could affect current period comparatives.

Assess disclosures: Confirm that the financial reporting framework’s disclosure requirements for comparative information are satisfied, including explanations of any restatements.

Consider the prior year opinion: If the predecessor auditor issued a modified opinion on the prior year, assess whether that modification has implications for the current year audit report.

When corresponding figures are used, the auditor’s opinion for the current period does not separately refer to the corresponding figures, unless a modification of opinion, emphasis of matter, or other communication is needed about those figures.

When the Corresponding Figures Are Misstated

If the auditor identifies that corresponding figures are materially misstated and management refuses to correct them, the auditor should consider the implications for the audit opinion. This could lead to a qualified or adverse opinion, depending on the severity and pervasiveness of the misstatement.

06 Auditor’s Responsibilities Relating to Comparative Financial Statements

Under the comparative financial statements approach, the auditor’s responsibilities extend more broadly. Both the current period and the prior period financial statements are within the scope of the audit opinion.

Forming the Opinion

ISA 710 requires that when an auditor is engaged to audit both periods, they should express an opinion on both periods in their current audit report. However, if only engaged for the current period, the opinion covers only the current period, and prior period comparative statements are referenced accordingly.

Where the prior period was audited by a predecessor auditor and the current auditor is presenting an opinion only on the current period, the audit report should indicate that the prior period was audited by another auditor, typically by including the predecessor’s name (if not prohibited by law or regulation) and the type of opinion issued.

Reporting on Both Periods

- The opinion covers both the current and comparative period financial statements when the auditor was engaged for both periods.

- Separate opinions may be issued for each period, or a combined opinion may cover both, the form depends on jurisdiction and engagement terms.

- A modification of the opinion in respect of either period must be clearly expressed, with the applicable period identified.

- If the prior period opinion was modified and the matter giving rise to that modification remains unresolved, the current year opinion must also be modified.

When comparative financial statements are presented, the auditor’s report should refer to each period for which financial statements are presented and on which an audit opinion is expressed.

— ISA 710, Para. 1507 Prior Period Misstatements Under ISA 710

A common and practical challenge in applying ISA 710 arises when prior period misstatements are identified during the current period audit. This intersects with IAS 8 (Accounting Policies, Changes in Accounting Estimates and Errors) and ISA 450 (Evaluation of Misstatements).

Retrospective Restatement

If the prior period financial statements contain a material misstatement, the applicable financial reporting framework may require retrospective restatement of comparative information. In that case, the auditor must:

- Evaluate whether the restatement has been correctly reflected in the current period’s comparative figures.

- Assess whether disclosures regarding the nature and amount of the restatement are adequate.

- Consider whether the restatement affects the opening balances and the current period’s figures.

When Prior Period Was Unaudited

Where comparative information has not been previously audited; common with newly incorporated entities, first-time audits, or voluntary comparative disclosure, the auditor should clearly indicate in the audit report that the comparative information is unaudited. This protects users from drawing unwarranted conclusions about the assurance provided.

Interaction with ISA 510: ISA 710 must be read alongside ISA 510 (Initial Audit Engagements – Opening Balances). Opening balances carried into the current period from unaudited or predecessor-audited prior periods require specific procedures under ISA 510, which directly feeds into the treatment of comparative information under ISA 710.

08 Impact of ISA 710 on the Audit Report

Understanding how ISA 710 affects the final audit report is critical. The treatment of comparative information shapes what the auditor can and must say in their report.

Unmodified Opinion

Where corresponding figures are correctly presented and material misstatements are absent, the audit report need not make specific reference to comparative information. The opinion covers the current period in the usual way.

Modified Opinion Scenarios

| Situation | Auditor’s Action | Opinion Type |

|---|---|---|

| Corresponding figures contain a material misstatement; management refuses to correct | Modify the opinion in relation to comparative information | Qualified or Adverse |

| Prior period modified opinion – matter unresolved | Modify current opinion consistently | Qualified, Adverse, or Disclaimer |

| Prior period modified opinion – matter now resolved | Issue unmodified opinion; may include Emphasis of Matter | Unmodified (with or without EOM) |

| Prior period unaudited – now presented as comparatives | State clearly in report that prior period is unaudited | Unmodified (with other matter paragraph) |

| Predecessor auditor’s prior period report was modified | Include Other Matter paragraph referencing predecessor’s modified opinion | Unmodified with Other Matter |

Reference to Predecessor Auditor in the Report

Under the comparative financial statements approach, when a predecessor auditor performed the prior period audit, the current auditor may include an Other Matter paragraph referencing this fact and the predecessor’s opinion. This is jurisdictionally sensitive, some local regulations prohibit naming the predecessor; in that case, the report should simply note that another auditor conducted the prior period audit.

09 Predecessor Auditor Considerations

ISA 710 specifically addresses the complexities that arise when the current auditor is new to the engagement and comparative information was audited by a predecessor auditor.

Corresponding Figures – Predecessor Auditor

Even though the current auditor’s opinion does not separately cover corresponding figures, they still bear responsibility for ensuring those figures are not misleading in the context of the current period financial statements. This requires:

- Reviewing predecessor’s audit report for the prior period.

- Reading the prior period financial statements to identify potential discrepancies with what is presented as comparatives.

- Considering whether matters raised in the predecessor’s report still have ongoing relevance.

Comparative Financial Statements – Predecessor Auditor

Here the current auditor must be more transparent in their report. They typically include language such as: “The financial statements of [Entity] for the year ended [prior date] were audited by another auditor who expressed an unmodified opinion on those statements on [date].”

This ensures that readers of the audit report are not misled into believing the current auditor has opined on the prior period’s figures beyond the extent of their procedures.

Before communicating with a predecessor auditor (e.g., to access prior working papers), the incoming auditor must comply with relevant ethical requirements including obtaining client consent in many jurisdictions. This is governed by the IESBA Code of Ethics rather than ISA 710 itself.

10 Practical Application of ISA 710

Translating the requirements of ISA 710 into day-to-day audit practice requires a structured approach. Here is a practical framework:

Identify the presentation approach: At the planning stage, determine whether the financial reporting framework applicable to the entity uses corresponding figures or comparative financial statements. This determines the scope of your opinion.

Review prior period financials: Obtain and read the prior period financial statements and (where available) the predecessor auditor’s report. Note any modifications, emphasis of matter, or other matter paragraphs.

Check arithmetic and roll-forward: Verify that prior period closing balances agree with the current period’s opening balances. Cross-reference to the trial balance, general ledger, and relevant schedules.

Assess accounting policy consistency: Identify any changes in accounting policies or estimates between periods. Determine whether such changes are properly disclosed and whether comparative figures have been restated appropriately.

Evaluate disclosures: Review comparative disclosures in the notes to the financial statements. Ensure they are complete, consistent with the amounts presented, and compliant with the framework’s requirements.

Consider material misstatements in comparatives: Assess whether any misstatements identified in prior period figures are material to the current period statements. If so, discuss with management and consider the need for correction or disclosure.

Draft the audit report correctly: Reflect the ISA 710 requirements in the report, whether or not to mention comparatives, and whether any modifications, emphasis of matter, or other matter paragraphs are needed.

11 Frequently Asked Questions

No. Under the corresponding figures approach, the auditor’s opinion refers only to the current period financial statements. The corresponding figures are not separately opined upon. However, if there is a material misstatement in the corresponding figures, the opinion on the current period may be modified.

If the comparative information relates to a prior period that was not audited, ISA 710 requires the auditor to state this clearly in their report, typically via an Other Matter paragraph. This makes it transparent to users that the prior period figures carry no assurance from the current or any prior audit.

ISA 510 governs initial audit engagements and the treatment of opening balances, while ISA 710 deals with comparative information in the financial statements. They are closely linked: opening balances verified under ISA 510 feed directly into the prior period comparative figures presented under ISA 710. Auditors must consider both standards together in initial engagements.

IFRS 18 (Presentation and Disclosure in Financial Statements) requires comparative information for the preceding period. In practice, IFRS-based financial statements commonly use the corresponding figures approach, where prior period figures appear alongside current period figures but are not presented as a separate complete set. However, the exact treatment depends on the entity’s jurisdiction and whether any national standards supplement IFRS requirements.

No. While the current auditor takes note of the predecessor’s report and opinion, they cannot simply rely on it without independent procedures. ISA 710 and ISA 510 require the current auditor to independently assess whether comparative figures are appropriately stated. If access to predecessor working papers is possible (with client consent), reviewing them can help but they do not replace the current auditor’s own judgement.

An “Other Matter” paragraph (governed by ISA 706) is included in the auditor’s report to communicate information relevant to users’ understanding of the audit, the auditor’s responsibilities, or the auditor’s report itself but that is not required to be presented in the financial statements. Under ISA 710, this paragraph may be used to reference the fact that a predecessor auditor audited the prior period, or that prior period comparative figures are unaudited.

ISA 710 should be studied in conjunction with ISA 510 (Initial Audit Engagements – Opening Balances), ISA 700 (Forming an Opinion and Reporting on Financial Statements), ISA 705 (Modifications to the Opinion), ISA 706 (Emphasis of Matter and Other Matter Paragraphs), and ISA 450 (Evaluation of Misstatements Identified During the Audit).

12 Conclusion

ISA 710 is a focused but consequential standard. Applied correctly, it preserves the integrity of comparative disclosures, information that users depend on for meaningful financial analysis.

The standard hinges on a clear distinction between two presentation approaches: corresponding figures, where the auditor’s opinion is directed solely at the current period, and comparative financial statements, where both periods fall within the opinion’s scope. Each approach carries distinct requirements for audit procedures, reporting language, and the treatment of predecessor auditor matters.

For auditors, the practical takeaway is this: do not treat prior period comparative information as passive background data. ISA 710 requires active evaluation of consistency, of restatements, of prior period opinions, and of the adequacy of disclosures. Failure to address these areas may not only compromise audit quality but could result in an incorrectly drafted audit report that misleads users.

For students of auditing and finance professionals, a firm grasp of ISA 710 is essential for understanding how the audit opinion is scoped and communicated, particularly in first-year and transitional audits where predecessor auditor dynamics come into play.

(Qualified) Chartered Accountant – ICAP

Master of Commerce – HEC, Pakistan

Bachelor of Accounting (Honours) – AeU, Malaysia