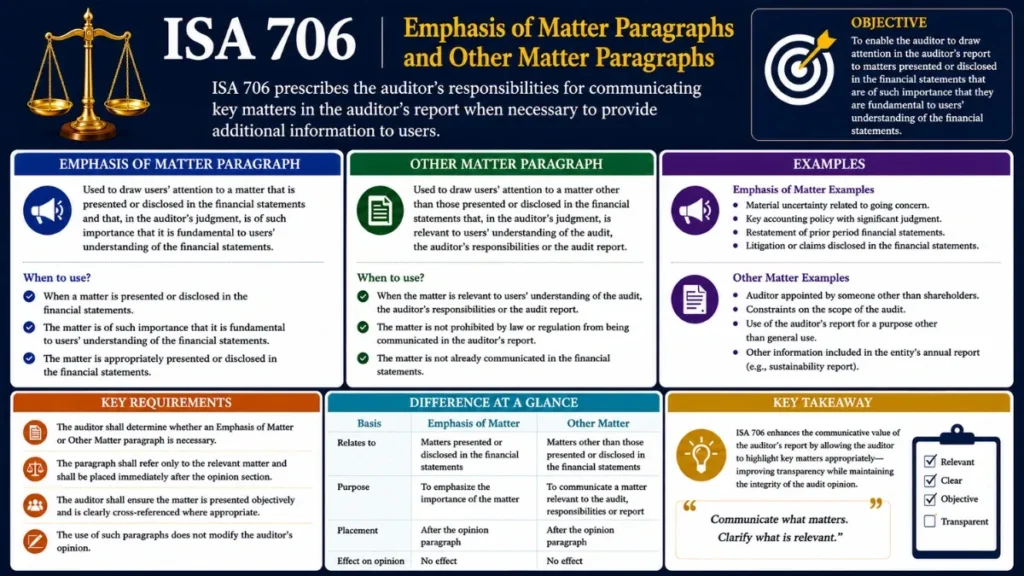

ISA 706 (Revised) deals with additional communication in the auditor’s report when the auditor considers it necessary to include (a) Emphasis of Matter Paragraph, and (b) Other Matter Paragraph.

Emphasis of Matter & Other Matter Paragraphs

A practitioner-level guide to ISA 706, the international standard governing when and how auditors draw special attention in the independent auditor’s report, without modifying the opinion.

What Is ISA 706? (Purpose and Scope)

ISA 706 (Revised) – formally titled “Emphasis of Matter Paragraphs and Other Matter Paragraphs in the Independent Auditor’s Report” issued by IAASB, addresses situations where an auditor wishes to draw users’ attention to matters beyond what a standard report communicates, without modifying the audit opinion itself.

These paragraphs serve a signposting function: they tell the reader “look at this particular matter; it is important for understanding these financial statements (EOM) or this audit (OM).” They are a tool for enhanced communication, not a halfway house for a modified opinion.

Critical distinction: Neither an Emphasis of Matter paragraph nor an Other Matter paragraph modifies the auditor’s opinion. If a matter warrants opinion modification, the auditor must apply ISA 705 not add an EOM paragraph as a substitute.

ISA 706 was revised as a direct consequence of the new ISA 701, which introduced Key Audit Matters (KAM) reporting for listed entities. The revision clarified the interaction between EOM paragraphs and KAMs to avoid duplication and confusion in the auditor’s report.

Emphasis of Matter vs Other Matter

ISA 706 governs two distinct types of additional paragraph. Understanding the distinction is fundamental to applying the standard correctly.

Emphasis of Matter Paragraph Under ISA 706

A paragraph included in the auditor’s report that refers to a matter appropriately presented or disclosed in the financial statements that, in the auditor’s judgment, is of such importance that it is fundamental to users’ understanding of the financial statements.

The matter must already exist in the financial statements, the EOM paragraph merely highlights it.

Other Matter Paragraph Under ISA 706

A paragraph included in the auditor’s report that refers to a matter not presented or disclosed in the financial statements that, in the auditor’s judgment, is relevant to users’ understanding of the audit, the auditor’s responsibilities, or the auditor’s report.

The matter is not in the financial statements, it concerns the audit process or the auditor’s report itself.

Conditions for Including EOM and OM Paragraphs

Emphasis of Matter – Prerequisites

Matter in the Financial Statements

The matter must be appropriately presented or disclosed in the financial statements. If not properly disclosed, the auditor would consider a modified opinion instead.

Fundamental to User Understanding

In the auditor’s judgment, the matter is of such importance that it is fundamental not merely helpful for users to understand the financial statements.

Opinion Not Modified on the Matter

An EOM paragraph cannot be used when the auditor has, or should have, expressed a modified opinion regarding the same matter.

Not a Key Audit Matter (When ISA 701 Applies)

When ISA 701 applies (listed entities), the matter must not have already been determined to be a Key Audit Matter communicated in the KAM section.

Other Matter – Prerequisites

Matter Outside the Financial Statements

The matter is not presented or disclosed in the financial statements themselves. It relates to the audit, the auditor’s responsibilities, or the scope of the auditor’s report.

Relevant to User Understanding

The matter is relevant to users’ understanding of the audit, the auditor’s responsibilities, or the auditor’s report not merely interesting background information.

Not Prohibited by Law or Ethics

The OM paragraph must not include information that the auditor is prohibited from providing by law, regulation, or ethical standards relating to confidentiality.

Not Management’s Responsibility

The OM paragraph must not include information that should properly be provided by management, it is not a substitute for management disclosures.

Common Triggers for ISA 706 (ISAs That Require EOM or OM)

ISA 706 is most frequently triggered by requirements in other ISAs rather than by the auditor’s voluntary judgment. The following are common mandatory triggers appended in the standard’s annexures.

Common Emphasis of Matter (EOM) Triggers

- Going Concern Uncertainty (ISA 570) when significant doubt exists but the going concern basis is still appropriate

- Subsequent Events (ISA 560) revision of financial statements after their original issuance

- Comparative Information (ISA 710) prior period statements audited by a predecessor auditor or significantly restated

- Early IFRS Adoption early application of a new IFRS with material effect on the financial statements

- Major Catastrophe a significant catastrophe that has or continues to affect the entity’s financial position

- Special Purpose Frameworks (ISA 800) drawing attention to the basis of accounting used

Common Other Matter (OM) Triggers

- Initial Engagement prior year financial statements were not audited (ISA 510)

- Predecessor Auditor current year audit report references prior year audited by another firm

- Restricted Distribution the auditor’s report is intended solely for specific users

- Additional Reporting Obligations law or regulation requires the auditor to communicate planning or scoping matters

- Agreed Terms of Engagement (ISA 210, 800) specific purpose framework restrictions or agreed reporting obligations

- Scope Limitations on Prior Year limitations affecting the auditor’s report on comparative information

Placement in the Auditor’s Report

The auditor must use a heading that clearly identifies the nature of the paragraph. Placement follows a standard hierarchy, though auditor judgment governs the relative positioning of EOM paragraphs when both a KAM section and an EOM paragraph are present.

Positioning flexibility: When an EOM paragraph is included alongside a KAM section, the auditor may position the EOM paragraph either directly before or after the KAM section based on judgment about the relative significance of the matter.

Practical Examples of EOM and OM Paragraph

Emphasis of Matter Examples

We draw attention to Note 3 in the financial statements, which indicates that the Company incurred a net loss of $4.2 million during the year ended December 31, 20XX, and, as of that date, the Company’s current liabilities exceeded its current assets by $6.8 million. As stated in Note 3, these events or conditions, along with other matters as set forth in Note 3, indicate that a material uncertainty exists that may cast significant doubt on the Company’s ability to continue as a going concern. Our opinion is not modified in respect of this matter.

As discussed in Note 9 to the financial statements, the comparative information for the year ended December 31, 20X0, has been restated to reflect the correction of an error in the previously issued financial statements. Our audit procedures were restricted to the restatement adjustments described in Note 9. Our opinion is not modified in respect of this matter.

Other Matter Examples

The financial statements of ABC Company for the year ended December 31, 20X0, were audited by another auditor who expressed an unmodified opinion on those statements on March 31, 20X1.

This report is intended solely for the information and use of the Board of Directors and management of ABC Company and is not intended to be and should not be used by anyone other than these specified parties.

Interaction Between ISA 706 and ISA 701

The revised ISA 706 was necessitated by the introduction of ISA 701, which requires auditors of listed entities to communicate Key Audit Matters. The two standards interact critically:

When ISA 701 Applies (Listed Entities)

An EOM paragraph cannot be used for a matter that has already been determined to be a Key Audit Matter. This prevents double-reporting and confusion.

However, EOM paragraphs can still coexist with KAM sections for matters that are not KAMs (for example), a going concern material uncertainty that the auditor judges warrants even stronger signposting than a KAM.

When ISA 701 Applies (Listed Entities)

OM paragraphs can coexist with KAM sections, they address fundamentally different things: OM paragraphs concern the audit context, while KAMs concern the financial statements.

When ISA 701 does not apply (non-listed entities), EOM and OM paragraphs operate without this interaction and can be used more freely.

Practical note: For non-listed entities not subject to ISA 701, the EOM paragraph effectively performs a KAM-like function, it highlights the most significant areas of the audit requiring user attention without the structured ISA 701 disclosure requirements.

Key Differences Between EOM and OM

| Criterion | Emphasis of Matter (EOM) | Other Matter (OM) |

|---|---|---|

| Source of matter | Within the financial statements | Outside the financial statements |

| Purpose | Highlight what’s disclosed, fundamental to FS understanding | Inform about audit context, scope, or responsibilities |

| Opinion impact | None – must state opinion is not modified | None – does not affect the opinion |

| KAM overlap (ISA 701) | Cannot duplicate a KAM | Can coexist with KAMs |

| Reference to FS | Must reference relevant disclosure in FS | Explicitly about matters not in FS |

| Confidentiality limit | Cannot include prohibited information | Cannot include prohibited information |

| Management info substitute | Cannot replace management disclosures | Cannot replace management disclosures |

| Governance communication | Auditor must communicate expected inclusion | Auditor must communicate expected inclusion |

| Typical heading | “Emphasis of Matter” or “Emphasis of Matter [Topic]” | “Other Matter” or “Other Matter [Topic]” |

Frequently Asked Questions

Can an EOM paragraph be used instead of modifying the audit opinion?

No. An EOM paragraph is strictly for matters where the opinion is not modified. If a matter warrants a qualified, adverse, or disclaimer of opinion, ISA 705 applies. Regulators have specifically warned against using EOM paragraphs as a substitute for modification.

Can the same matter appear as both an EOM paragraph and a Key Audit Matter?

No. When ISA 701 applies, if a matter has been determined to be a KAM, the auditor cannot also include an EOM paragraph for that same matter. The EOM cannot duplicate a KAM. However, the auditor may elevate a matter from a KAM to the first KAM in the section, or add an additional description to signal its exceptional importance.

What happens if there are multiple OM matters?

When the OM section includes more than one matter, it may be helpful to use different sub-headings for each matter to assist users in understanding each separate topic. Multiple sub-headings improve readability and navigability.

Does ISA 706 apply to special purpose audit engagements?

Yes. ISA 800 and ISA 805 (special purpose frameworks and single financial statements) explicitly require OM paragraphs in many circumstances (for example), drawing attention to the basis of accounting used, or restricting distribution of the report. ISA 706 governs the form and content of these paragraphs.

Must the auditor consult with management before including an EOM or OM paragraph?

ISA 706 requires the auditor to communicate with those charged with governance when expecting to include either type of paragraph. While management input is part of this process, the decision to include the paragraph and its wording is ultimately the auditor’s professional judgment.

Do national standards differ from IAASB’s ISA 706?

The IAASB ISA 706 forms the basis for most national implementations. National variants such as ISA (UK) 706 from the FRC, COS 706 in the Netherlands, or IDW PS 406 in Germany may include additional or modified requirements reflecting local legal or regulatory environments. Practitioners should always consult the applicable national standard.

(Qualified) Chartered Accountant – ICAP

Master of Commerce – HEC, Pakistan

Bachelor of Accounting (Honours) – AeU, Malaysia