The concept associate vs subsidiary explains the ‘Associate’ in which another Co. has a significant ownership stake, and ‘Subsidiary’ that is owned and controlled by another Co.

Corporate Structures · Ownership · Accounting

Associate vs Subsidiary

A definitive guide to ownership thresholds, financial reporting, legal control, and strategic implications

Associate vs Subsidiary: What’s the Difference?

Significant Influence, Not Control

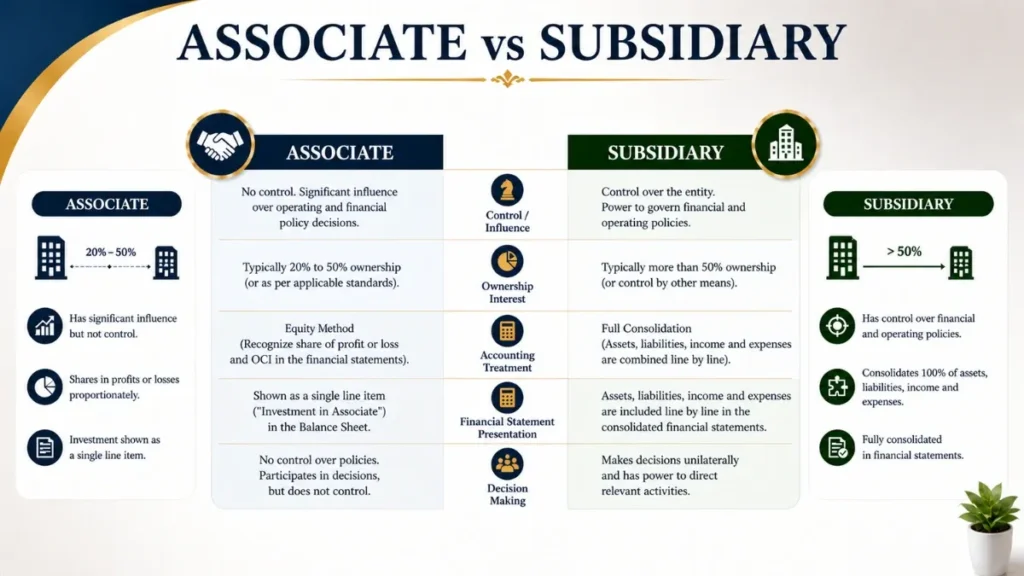

An associate is a company in which the investor holds between 20% and 50% of the voting shares. This gives the investor significant influence over financial and operating decisions, but not the power to dictate them. Under IAS 28, the equity method of accounting applies.

Full Control & Consolidation

A subsidiary is a company controlled by a parent, typically through ownership of more than 50% of voting shares. The parent can dictate operational and financial policies. Under IFRS 10, the subsidiary’s financials are fully consolidated into the parent’s statements.

Ownership and Control: Associate vs Subsidiary

Ownership percentage is the foundational criterion. Both IFRS and US GAAP use similar thresholds, though the underlying concept of control versus significant influence can sometimes override these numbers.

Rebuttable Presumptions

The 20% and 50% thresholds are rebuttable presumptions, not absolute rules. Under IAS 28, significant influence may be evidenced by representation on the board, participation in policy-making, material intercompany transactions, interchange of managerial personnel, or provision of essential technical information, even if the ownership stake falls below 20%.

Control vs Significant Influence

The distinction between control and significant influence is the conceptual foundation of this entire topic, and it has profound practical consequences.

What Is Control?

Control, as defined under IFRS 10, means the investor has all three of the following: power over the investee, exposure to variable returns from its involvement, and the ability to use that power to affect those returns. A parent controls a subsidiary and can direct its operations, appoint or remove its directors, and set its strategic direction.

What Is Significant Influence?

Significant influence is the power to participate in the financial and operating policy decisions of an entity, but not to control them. An associate investor can exert pressure, vote at general meetings, and have a voice on the board, but cannot unilaterally impose decisions. The associate’s management retains independence in day-to-day affairs.

The difference between control and significant influence is the difference between directing a symphony and being a first-chair violinist, one sets the tempo for everyone; the other plays a powerful part without commanding the whole.

– Corporate Governance PrincipleDe Facto Control

Sometimes a company can have de facto control of a subsidiary with less than 50% of shares (for example), if the remaining shares are widely dispersed among thousands of passive shareholders and the investor consistently achieves its preferred voting outcomes. IFRS 10 requires entities to assess actual power, not just legal ownership percentages.

Accounting Treatment: Equity Method vs Consolidation

How a company accounts for its investment in an associate versus a subsidiary is one of the most consequential financial distinctions in corporate reporting. The two methods differ fundamentally.

Associates: The Equity Method

Under the equity method (required by IAS 28), the investment is initially recorded at cost. Subsequently, the carrying amount is adjusted to reflect the investor’s share of the associate’s profit or loss and other comprehensive income.

- Investment shown as a single line on the balance sheet

- Investor’s proportional share of net income recognized in P&L

- Dividends received reduce the carrying value of the investment

- Impairment testing required if indicators exist

Subsidiaries: Full Consolidation

Under IFRS 10, a parent must consolidate its subsidiary by combining the financial statements line by line; adding together all assets, liabilities, equity, income, and expenses. Intercompany transactions are eliminated to avoid double-counting.

- All assets and liabilities consolidated 100%, even if <100% owned

- Non-controlling interests presented separately in equity

- Intercompany sales, loans, and dividends fully eliminated

- Goodwill arises on acquisition and is tested for impairment annually

Associate vs Subsidiary: Side-by-Side Comparison

| Criterion | Associate Company | Subsidiary Company |

|---|---|---|

| Ownership Stake | 20% – 50% of voting shares | More than 50% of voting shares |

| Degree of Influence | Significant influence | Control (full decision-making power) |

| Accounting Method | Equity method (IAS 28 / ASC 323) | Full consolidation (IFRS 10 / ASC 810) |

| Financial Statements | Investment shown as single line item | All assets & liabilities combined |

| Profit Recognition | Proportional share of net profit only | Full revenue and expenses consolidated |

| Non-Controlling Interest | Not applicable | Presented in equity if <100% owned |

| Goodwill Treatment | Included within equity investment value | Recognised separately; annual impairment test |

| Legal Independence | Fully independent legal entity | Legally separate but operationally directed |

| Board Representation | Typically has board seats; no majority | Parent typically controls board majority |

| Liability Exposure | Limited to investment amount (generally) | Potential for group-wide liability in some jurisdictions |

| Dividend Policy | Investor has limited influence | Parent sets or heavily influences dividend policy |

| Tax Filing | Files independently | May file consolidated tax return (jurisdiction-specific) |

| Strategic Alignment | Collaborative; associate sets own strategy | Strategy dictated by parent group |

Legal and Strategic Differences

Beyond accounting, the associate vs. subsidiary classification carries significant legal weight across multiple dimensions.

Liability and Creditor Rights

A subsidiary, while legally separate, can in some circumstances expose a parent to liability, particularly where courts apply the doctrine of “piercing the corporate veil” when the subsidiary is undercapitalized, used to commit fraud, or where the parent treats it as an alter ego. Associates carry much lower liability risk for the investor, since there is no control and the investor is treated as an arms-length shareholder.

Regulatory Compliance

Subsidiaries must comply with local corporate law, employment law, and tax regulations in every jurisdiction they operate in, and the parent is responsible for ensuring group-level compliance. Associates are independent legal entities; the investor has no compliance obligation beyond standard shareholder duties.

Competition Law

In merger control proceedings, regulators assess whether one entity controls another. Acquiring a 20-50% stake in an associate may still require regulatory notification in many jurisdictions if it confers significant influence. Acquiring majority control of a subsidiary almost always triggers merger review thresholds.

Real-World Examples of Associate and Subsidiary

Associate Examples

Volkswagen Group holds approximately a 20% stake in Aston Martin Lagonda, classifying it as an associate and accounting for it under the equity method. Similarly, large institutional investors, pension funds and sovereign wealth funds frequently hold 20–40% stakes in infrastructure or energy companies, classifying them as associates and recording proportional earnings without full consolidation.

Subsidiary Examples

Alphabet Inc. treats Google LLC, YouTube, and Waymo as wholly-owned subsidiaries, all financials are consolidated into Alphabet’s group statements. Berkshire Hathaway fully consolidates GEICO, BNSF Railway, and dozens of other businesses as wholly-owned subsidiaries while simultaneously holding associate-level stakes in companies like Kraft Heinz at proportional equity method recognition.

Which Structure Should You Choose? (Associate or Subsidiary)

The choice between establishing or investing in an associate versus creating or acquiring a subsidiary is rarely arbitrary; it involves balancing control ambitions, financial statement optics, regulatory constraints, and risk appetite.

Choose an Associate Structure When…

- You want strategic alignment without full liability exposure

- The target company’s management and independence is a key value driver

- You prefer to keep debt and liabilities off the consolidated balance sheet

- Regulatory or antitrust environments limit full acquisitions

- You’re entering a new market and want a local partner to retain autonomy

- Capital constraints prevent a majority acquisition

Choose a Subsidiary Structure When…

- Full operational integration and unified strategy is required

- You need control over dividend flows and capital allocation

- Consolidated tax benefits justify full ownership

- Brand and reputational alignment requires complete authority

- You’re acquiring a target whose full revenue must consolidate

- Long-term strategic importance demands undivided control

Frequently Asked Questions

-

What is the main difference between an associate and a subsidiary?

The core difference is the degree of ownership and the resulting level of control. A subsidiary requires more than 50% ownership, giving the parent company full control. An associate involves 20-50% ownership, granting significant influence (the ability to participate in decisions but not to dictate them). This distinction also drives entirely different accounting treatments: consolidation for subsidiaries versus the equity method for associates.

-

Can a company be both an associate and a subsidiary?

No, a company cannot be both simultaneously in relation to the same investor. The classification is mutually exclusive and depends on the ownership percentage and the degree of control or influence exercised. However, the same investee company could be classified differently by different shareholders (e.g., one shareholder at 60% treats it as a subsidiary, while another shareholder at 25% treats it as an associate).

-

What happens if ownership falls from 55% to 30%? Does a subsidiary become an associate?

Yes. If a parent disposes of shares such that its holding falls below 50%, it loses control and the entity is derecognised as a subsidiary. It is then reclassified as an associate if the remaining 30% stake still confers significant influence. The parent must recognise any gain or loss on disposal, remeasure the retained interest at fair value, and begin applying the equity method prospectively.

-

Is an associate’s debt included on the investor’s balance sheet?

No. Under the equity method, only the carrying value of the investment appears on the investor’s balance sheet as a single asset. The associate’s individual assets, liabilities, revenues, and expenses are not consolidated. This is a significant reason why many companies prefer associate structures, it keeps leveraged entities’ debt from inflating their own balance sheets.

-

What is goodwill, and does it arise for associates?

Goodwill represents the excess of the acquisition price over the fair value of net identifiable assets acquired. For a subsidiary, goodwill is recognised as a separate intangible asset and tested for impairment annually. For an associate, goodwill is not separately recognised, it is instead subsumed within the carrying amount of the equity investment and impaired as part of the overall investment assessment.

-

Are associates required to be disclosed in financial statements?

Yes. IAS 28 requires disclosure of the nature of the relationship, the associate’s principal activities, the investor’s ownership percentage, the associate’s summarised financial information (assets, liabilities, revenues, profit), and any restrictions on the transfer of funds. Subsidiaries require extensive disclosure under IFRS 12, including the basis of consolidation and details of non-controlling interests.

Summary: The Essential Takeaway

The associate vs. subsidiary distinction ultimately comes down to a single word: control. Subsidiaries are controlled entities; financially consolidated, operationally directed, and strategically unified with their parent. Associates are influenced entities; reported via the equity method, independently managed, and strategically aligned but not absorbed.

For finance professionals, the implications span accounting treatment, tax strategy, regulatory compliance, and capital structure. For business strategists, the choice between the two reflects broader decisions about integration depth, risk appetite, and growth philosophy. Understanding both structures, and knowing when each is appropriate is a cornerstone of corporate finance literacy.

(Qualified) Chartered Accountant – ICAP

Master of Commerce – HEC, Pakistan

Bachelor of Accounting (Honours) – AeU, Malaysia