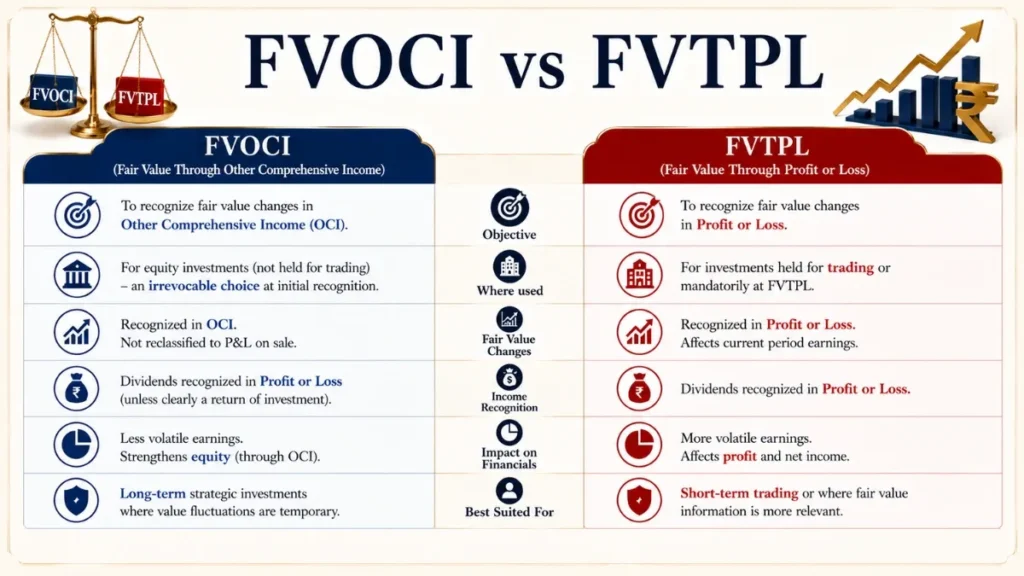

FVOCI vs FVTPL a concept which describes the key classification categories under IFRS 9 that determine how financial assets are measured and reported. While FVOCI records value changes outside profit or loss, FVTPL directly ‘impacts earnings‘.

Understanding the difference between FVOCI and FVTPL is essential for accurate financial reporting and investment analysis. Learn how these classifications affect income statements, equity, and overall financial performance.

FVOCI vs FVTPL

A Definitive Accounting Guide

Fair Value through Other Comprehensive Income vs Fair Value through Profit or Loss classification criteria, treatment differences, and practical application under IFRS 9.

Quick Reference

IFRS 9 at a Glance- Standard: IFRS 9 – Financial Instruments (issued by IASB) effective 1 Jan 2018

- Replaced: IAS 39

- Categories: 3 measurement categories

- Key Tests: Business Model + SPPI

- Impairment: ECL applies to FVOCI debt only

- Equity FVOCI: Irrevocable election

- OCI Recycling: Debt (yes) · Equity (never)

- Default: FVTPL for all other assets

What is FVOCI and FVTPL in IFRS 9?

Under IFRS 9 – Financial Instruments, entities are required to classify and measure financial assets based on two factors: the business model for managing those assets, and the contractual cash flow characteristics of the asset. This results in three primary measurement categories, two of which FVOCI and FVTPL involve fair value measurement.

FVOCI

Fair Value through Other Comprehensive Income. Fair value changes are recognised in OCI and accumulated in equity. Depending on instrument type, gains and losses may or may not be recycled to profit or loss upon derecognition.

FVTPL

Fair Value through Profit or Loss. All fair value changes are recognised immediately in the income statement. This is the default classification under IFRS 9 when no other category applies.

Both categories require assets to be carried at fair value on the statement of financial position. The critical distinction lies in where fair value movements are reported in equity (OCI) or in the income statement (profit or loss) and the consequent effects on earnings volatility, financial ratios, and tax treatment.

How Financial Assets are Classified under IFRS 9?

IFRS 9 establishes a principle-based classification framework. The decision tree below illustrates how a financial asset is routed to FVOCI or FVTPL:

Classification depends on: (1) Business Model Test how the entity manages its financial assets; and (2) SPPI Test (Solely Payments of Principal and Interest) whether contractual cash flows are solely principal and interest on outstanding principal. Both must be assessed to determine the correct classification.

Business Model Test

The business model reflects how an entity manages its financial assets to generate cash flows. Three business model categories exist: hold to collect, hold to collect and sell, and other. FVOCI applies to debt instruments managed under a “hold to collect and sell” business model. If managed under any other model (including trading), FVTPL is the result.

SPPI Test

For a debt instrument to qualify for FVOCI (or Amortised Cost), its contractual terms must give rise on specified dates to cash flows that are solely payments of principal and interest on the principal outstanding. If this test is failed (for example), an equity-linked note or an instrument with leverage features, the asset must be classified at FVTPL regardless of the business model.

FVOCI vs FVTPL for Debt Instruments

For debt instruments (bonds, loans, receivables), the classification follows directly from the business model and SPPI tests. The table below details the accounting treatment under each category:

| Accounting Element | FVOCI – Debt Instrument | FVTPL – Debt Instrument |

|---|---|---|

| Initial measurement | Fair value (including transaction costs) | Fair value (transaction costs expensed) |

| Subsequent measurement | Fair value | Fair value |

| Fair value changes | Recognised in OCI | Recognised in profit or loss |

| Interest income | Recognised in P&L using EIR method | Recognised in P&L (may use EIR) |

| ECL impairment | Required (12-month or lifetime ECL) | Not applicable, losses already in P&L |

| OCI recycling on disposal | Yes — recycled to P&L | N/A |

| Foreign exchange gain/loss | In P&L (monetary item treatment) | In P&L |

| Business model required | Hold to collect and sell | Any other (or FPTO election) |

IFRS 9 permits entities to irrevocably designate a financial asset as FVTPL at initial recognition if doing so eliminates or significantly reduces an accounting mismatch that would otherwise arise. This “fair value option” (FVO) can override an otherwise applicable FVOCI classification for debt instruments.

FVOCI vs FVTPL for Equity Instruments

The treatment of equity instruments under IFRS 9 differs significantly from debt instruments. Equity instruments are by default measured at FVTPL, since they typically do not pass the SPPI test. However, IFRS 9 provides an irrevocable election to designate eligible equity instruments as FVOCI.

The FVOCI Election for Equity Instruments

An entity may elect, at initial recognition, to classify equity instruments not held for trading as FVOCI. This election is irrevocable (once made), the instrument cannot be reclassified back to FVTPL. Critically, for equity instruments, gains and losses recognised in OCI are never recycled to profit or loss, even upon disposal.

| Accounting Element | FVOCI – Equity Instrument | FVTPL – Equity Instrument |

|---|---|---|

| Default classification | No, requires irrevocable election | Yes, default for equity instruments |

| Held-for-trading instruments | Not eligible | Mandatory FVTPL |

| Fair value changes | Recognised in OCI | Recognised in profit or loss |

| Dividends | In P&L (unless clearly return of investment) | In P&L |

| OCI recycling on disposal | Never recycled | N/A, already in P&L |

| Impairment assessment | Not required under IFRS 9 | Not required under IFRS 9 |

| Effect on earnings volatility | Lower, changes bypass P&L | Higher, all changes hit P&L |

| Accumulated OCI on disposal | Transferred within equity (not P&L) | N/A |

Unlike debt instruments classified as FVOCI (where cumulative OCI gains/losses are recycled to P&L on derecognition), equity instruments designated as FVOCI accumulate gains/losses in OCI that are permanently parked in equity upon disposal. This is a fundamental and often-tested distinction in professional accounting examinations.

FVOCI vs FVTPL: Key Differences Explained (Comparison Table)

The following comprehensive comparison covers all major dimensions on which FVOCI and FVTPL differ:

| Criterion | FVOCI | FVTPL |

|---|---|---|

| Measurement basis | Fair value | Fair value |

| Fair value movements – debt | In OCI (recycled on disposal) | In profit or loss |

| Fair value movements – equity | In OCI (never recycled) | In profit or loss |

| Interest income – debt | EIR method via P&L | May use EIR or coupon rate |

| Dividends – equity | P&L | P&L |

| ECL impairment – debt | Required | Not applicable |

| Transaction costs – initial | Included in carrying amount | Expensed immediately |

| P&L volatility | Lower (movements buffered in OCI) | Higher (all changes in P&L) |

| Balance sheet transparency | Full fair value reflected | Full fair value reflected |

| Eligible instrument types | Debt (BM test + SPPI); Equity (election) | All, default category |

| Reclassification possible | For debt if BM changes; equity, never | For debt if BM changes |

| FX component – monetary debt | P&L (separate from OCI) | P&L |

| Preference for | Liquidity portfolios, strategic stakes | Trading books, derivatives, default |

OCI Recycling in FVOCI vs FVTPL

“Recycling” (also called reclassification) refers to the transfer of accumulated OCI gains or losses to profit or loss upon the derecognition (disposal, maturity, or write-off) of a financial asset.

Debt Instruments – Recycling Applies

When a debt instrument classified as FVOCI is derecognised, the cumulative gain or loss previously recognised in OCI is reclassified from equity to profit or loss. This ensures that the total gain or loss recognised in P&L over the instrument’s life equals the economic gain or loss realised, identical to what would have been recognised under Amortised Cost, plus the fair value gain/loss at disposal.

Equity Instruments – No Recycling

For equity instruments designated as FVOCI, the accumulated OCI balance is never transferred to profit or loss. Upon disposal, the entity transfers the cumulative gain or loss within equity (e.g., to retained earnings), but it never passes through the income statement. This policy was deliberately designed by the IASB to prevent “cherry-picking”, the selective sale of appreciated investments to boost reported earnings.

Debt FVOCI: Entity A holds a bond at FVOCI. It was acquired at £100, currently carried at £108 (£8 accumulated in OCI). On disposal at £108, the £8 OCI gain is recycled to profit or loss. Total P&L impact: £8 gain recognised on disposal.

Equity FVOCI: Entity B holds shares at FVOCI. Acquired at £50, fair value now £65 (£15 in OCI). On disposal at £65, the £15 OCI balance is transferred to retained earnings, not to profit or loss. P&L impact on disposal: £nil from the FV gain.

ECL Impairment Model: FVOCI vs FVTPL

One of the most consequential differences between FVOCI and FVTPL relates to impairment accounting under the Expected Credit Loss (ECL) model in IFRS 9.

FVOCI – Debt Instruments

Debt instruments classified as FVOCI are subject to the full ECL impairment model. Entities must recognise an ECL allowance, which is presented as an adjustment to the OCI reserve (not the carrying amount, since the instrument is already at full fair value). The impairment charge is recognised in profit or loss. The three-stage ECL model applies: Stage 1 (12-month ECL), Stage 2 (lifetime ECL, significant increase in credit risk), and Stage 3 (lifetime ECL, credit-impaired).

FVTPL – No Separate Impairment

Financial assets at FVTPL do not require a separate ECL impairment assessment. Since all fair value changes including those arising from credit deterioration, flow directly through profit or loss, any credit-related losses are automatically captured in the fair value measurement. There is no concept of an impairment allowance for FVTPL assets.

For FVOCI debt instruments: Stage 1 performing; recognise 12-month ECL. Stage 2 significant increase in credit risk (SICR); recognise lifetime ECL. Stage 3 credit-impaired; recognise lifetime ECL and switch interest revenue to net carrying amount basis.

Real-Life Examples of FVOCI and FVTPL

A commercial bank holds a portfolio of government bonds primarily to earn interest but may sell them to manage liquidity needs. The business model is hold to collect and sell, and the bonds pass the SPPI test. Classification: FVOCI. Fair value changes flow through OCI each period; interest income is recognised via the EIR method in P&L; ECL impairment is assessed. Upon maturity or sale, cumulative OCI is recycled to P&L.

An investment bank holds corporate bonds for short-term profit-taking. The business model does not meet the “hold to collect” or “hold to collect and sell” criteria. Classification: FVTPL. All fair value movements, interest income, and FX differences are recognised in profit or loss. No ECL assessment is required.

A manufacturing company holds a 5% stake in a key supplier for strategic relationship purposes, not for trading. At initial recognition, it makes the irrevocable FVOCI election. Subsequent fair value increases of £2m are recognised in OCI. Dividends received are recognised in P&L. If the stake is sold, the £2m OCI gain is reclassified to retained earnings, not profit or loss.

A hedge fund acquires shares in a listed company to benefit from short-term price movements. No FVOCI election is made (instrument is held for trading, ineligible for election). Classification: FVTPL. All fair value gains and losses flow through P&L each reporting period, reflecting the fund’s trading intent and creating direct earnings impact.

Summary: FVOCI vs FVTPL Key Takeaways

FVOCI – When to Use & Key Facts

- Debt: BM = hold to collect AND sell + SPPI pass

- Equity: irrevocable election at initial recognition

- Fair value changes go to OCI, not P&L

- Debt OCI gains/losses recycled to P&L on disposal

- Equity OCI gains/losses never recycled to P&L

- ECL impairment required for debt instruments

- Reduces earnings volatility from market movements

- Transaction costs included in initial carrying amount

FVTPL – When to Use & Key Facts

- Default category, applies when no other fits

- Mandatory for held-for-trading equity instruments

- All fair value changes hit profit or loss directly

- No separate ECL impairment assessment needed

- Transaction costs expensed immediately

- Fair value option available to reduce accounting mismatch

- Higher earnings volatility from market fluctuations

- No OCI accumulation or recycling complexity

Frequently Asked Questions

What is the main difference between FVOCI and FVTPL?

The fundamental difference lies in where fair value changes are recognised. Under FVOCI, fair value movements are recorded in Other Comprehensive Income (OCI), a component of equity and do not flow through the income statement. Under FVTPL, all fair value changes are recognised immediately in profit or loss. Both categories carry assets at fair value on the balance sheet; only the routing of gains and losses differs.

Can equity instruments be classified as FVOCI under IFRS 9?

Yes, but only through an irrevocable election made at initial recognition. The election is available for equity instruments that are not held for trading. Once elected, the instrument stays at FVOCI for its entire life, it cannot be reclassified. Importantly, unlike debt instruments, gains and losses on equity FVOCI instruments are never recycled to profit or loss, even on disposal.

What is the SPPI test and why does it matter?

The Solely Payments of Principal and Interest (SPPI) test assesses whether a debt instrument’s contractual cash flows represent only payments of principal and interest on the outstanding principal amount. A debt instrument must pass this test to be eligible for either Amortised Cost or FVOCI classification. Instruments with equity-linked returns, leverage features, or complex cash flow structures typically fail the SPPI test and must be classified at FVTPL.

What does “OCI recycling” mean in the context of FVOCI?

OCI recycling (or reclassification) refers to the transfer of accumulated OCI balances to profit or loss when a financial asset is derecognised. For debt instruments at FVOCI, the cumulative fair value gain or loss held in OCI is reclassified to P&L upon disposal, ensuring total P&L recognition equals the economic gain/loss. For equity instruments at FVOCI, recycling never occurs; the OCI balance is transferred within equity upon disposal.

Is ECL impairment required for FVTPL assets?

No. The ECL impairment model under IFRS 9 does not apply to financial assets classified at FVTPL. Because the asset is carried at fair value and all changes flow through profit or loss, any credit deterioration is automatically reflected in the fair value measurement. There is no need for a separate impairment allowance. ECL is required for assets at Amortised Cost and for debt instruments at FVOCI.

Can an entity reclassify between FVOCI and FVTPL?

Reclassification of debt instruments between categories is permitted under IFRS 9, but only when an entity changes its business model for managing financial assets. Such changes are expected to be infrequent and must be demonstrated by significant internal and external changes. Reclassification is applied prospectively from the reclassification date. For equity instruments, the FVOCI designation is irrevocable, reclassification is never permitted.

Why would an entity prefer FVOCI over FVTPL for equity instruments?

Entities that hold equity investments for strategic rather than trading purposes often prefer FVOCI to reduce earnings volatility. By routing fair value changes through OCI rather than P&L, the income statement is shielded from fluctuations in share prices that are unrelated to the entity’s core operating performance. This is particularly relevant for long-term strategic stakes, cross-shareholdings, or investments in unlisted companies where fair value can be volatile and hard to predict.

How are dividends treated for FVOCI equity instruments?

Dividends received on equity instruments designated as FVOCI are generally recognised in profit or loss, unless they clearly represent a recovery of part of the cost of the investment (i.e., a return of capital). This means entities still recognise investment income from FVOCI equity holdings through P&L, even though capital appreciation/depreciation flows through OCI.

(Qualified) Chartered Accountant – ICAP

Master of Commerce – HEC, Pakistan

Bachelor of Accounting (Honours) – AeU, Malaysia