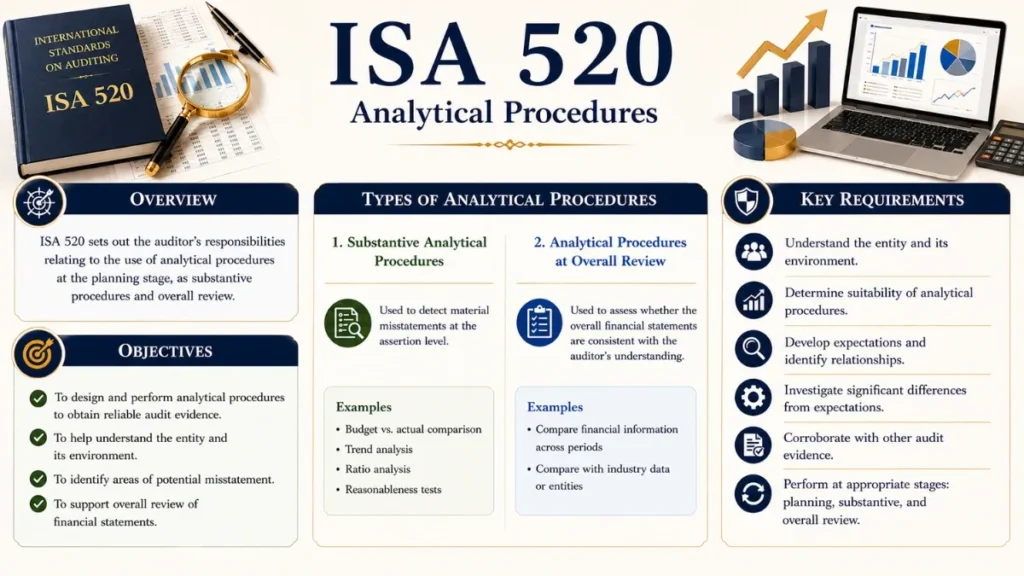

ISA 520 deals with the auditor’s use of analytical procedures as substantive procedures (Substantive Analytical Procedures).

ISA 520 – Analytical Procedures

A comprehensive, practitioner-focused guide to the auditor’s responsibilities under ISA 520, from forming precise expectations to investigating unexpected results near the close of the audit.

ISA 520 governs one of the most powerful and cost-efficient techniques in the auditor’s toolkit (analytical procedures). By evaluating the plausible relationships between financial and non-financial data, auditors can identify risks, gather substantive evidence, and reach well-founded overall conclusions about financial statements.

1. What Is ISA 520? (Scope and Purpose)

Para. 1 – What ISA 520 covers and what it does not.

It addresses two distinct aspects of an auditor’s work. For the authoritative text, refer to the Official IAASB Standard ISA 520 – Analytical Procedures. First, it covers the use of analytical procedures as substantive procedures (that is), as direct evidence-gathering tools aimed at the assertion level in financial statements. Second, it governs the auditor’s obligation to perform analytical procedures near the end of the audit when forming an overall conclusion.

Importantly, the use of analytical procedures as risk assessment tools is governed by ISA 315 (Identifying and Assessing the Risks of Material Misstatement), not ISA 520. ISA 330 (The Auditor’s Responses to Assessed Risks) provides further guidance on the nature, timing, and extent of substantive procedures which may include analytical procedures.

ISA 520 applies to substantive analytical procedures and overall review procedures. Planning-stage analytical procedures used for risk identification fall under ISA 315, not ISA 520.

2. Definition of Analytical Procedures

Para. 4 – The authoritative IAASB definition.

“Analytical procedures” means evaluations of financial information through analysis of plausible relationships among both financial and non-financial data. Analytical procedures also encompass such investigation as is necessary of identified fluctuations or relationships that are inconsistent with other relevant information or that differ from expected values by a significant amount.

In plain terms, analytical procedures involve comparing, computing, and questioning relationships in financial data. The word “plausible” is key: auditors build an independent expectation of what a figure should be, then investigate material deviations from that expectation.

Types of Analytical Procedures in Auditing

Methods range from straightforward comparisons to complex statistical modelling:

Trend Analysis

Comparing current-period data to prior periods. For example, examining whether revenue growth tracks historical patterns or deviates unexpectedly.

Ratio Analysis

Computing financial ratios (gross margin %, current ratio, receivables days) and comparing against prior periods, budgets, or industry benchmarks.

Reasonableness Tests

Building an independent estimate using non-financial data — e.g., predicting total payroll using headcount × average salary × months without relying on prior periods.

Regression Analysis

Using statistical techniques to predict expected values based on identified relationships between variables, offering the highest level of assurance among analytical methods.

3. Objectives of ISA 520

Para. 3 – Dual objectives the auditor must achieve.

The auditor’s objectives under ISA 520 are twofold:

- To obtain relevant and reliable audit evidence when using substantive analytical procedures; and

- To design and perform analytical procedures near the end of the audit that assist the auditor when forming an overall conclusion as to whether the financial statements are consistent with the auditor’s understanding of the entity.

Analytical procedures are not optional “nice-to-have” steps. When designed well, they can provide highly persuasive evidence, in some cases reducing or replacing extensive tests of details, thereby improving audit efficiency without compromising quality.

4. Substantive Analytical Procedures

Para. 5 – Requirements when using analytical procedures as substantive evidence.

When an auditor decides to use analytical procedures as substantive evidence at the assertion level, ISA 520 requires that those procedures meet four specific criteria. The auditor must:

Determine Suitability

Assess whether the analytical procedure is suitable for the assertion given the assessed risk of material misstatement. Analytical procedures are generally more reliable for high-volume, predictable transactions.

Evaluate Data Reliability

Assess the reliability of the data used to develop the expectation; considering its source, comparability, nature, and the controls over its preparation.

Develop a Sufficiently Precise Expectation

Develop an expectation of recorded amounts precise enough to identify a potential material misstatement. The higher the risk, the more precise the expectation must be.

Set an Acceptable Threshold of Difference

Determine the amount of difference from the expectation that is acceptable without further investigation, influenced by materiality and the desired level of assurance.

Suitability for the Assertion

Substantive analytical procedures are generally more applicable to large volumes of homogeneous transactions that tend to be predictable over time. For example, they are highly effective for payroll costs (predictable from headcount and pay rates), utility expenses, and rental income based on known occupancy rates. They are typically less appropriate for high-risk assertions such as the existence of inventory or the occurrence of revenue where cut-off risks are elevated.

If a company has 120 employees at an average monthly salary of $4,500, the auditor can independently predict annual payroll at approximately $6.48 million. If the financial statements show $8.1 million, the unexplained variance of $1.62 million demands investigation, without the auditor having tested a single payslip.

5. Reliability of Data in Analytical Procedures

Para. 5(b) & A12–A13 – What makes data suitable for analytical procedures.

The quality of an analytical procedure’s conclusion depends entirely on the quality of the underlying data used to form the expectation. ISA 520 identifies four factors relevant to data reliability:

Source

Data from independent external sources is generally more reliable than internally generated management data. Industry benchmarks, central bank rates, and regulatory filings are examples of higher-reliability sources.

Comparability

Broad industry averages may need supplementation to be comparable to a specific entity’s profile e.g., adjusting for company size, geography, or business model differences.

Nature & Relevance

Budgets set as aspirational goals may be less reliable than budgets set as expected results. The auditor must understand management’s intent behind the data.

Controls Over Preparation

If the entity has effective controls over the preparation of the data (e.g., HR system controls over headcount), the auditor can place greater reliance on that data.

Using management-prepared analytical data can be effective, but the auditor must first satisfy themselves that the underlying data has not been manipulated to support the financial statement figures being audited. This requires some level of independent corroboration.

Testing Controls Over Non-Financial Data

ISA 520 permits the auditor to test the operating effectiveness of controls over information used in analytical procedures. For instance, if HR system controls over recording employee headcount are effective, the auditor may rely more heavily on headcount data when forming payroll expectations, combining this with tests of those controls to increase overall efficiency.

6. Developing Expectations Under ISA 520

Para. 5(c) & A15 – How precise must the expectation be?

ISA 520 requires the auditor to evaluate whether the expectation can be developed with sufficient precision to identify a material misstatement. Key considerations include:

| Factor | Effect on Precision Required | Implication |

|---|---|---|

| High assessed risk | Higher precision needed | More disaggregated data; narrower acceptable threshold |

| Disaggregated data available | Enables greater precision | Procedure applied at segment/division level is more effective |

| Predictable, stable relationships | Higher precision achievable | Fixed costs, long-term contracts, regulated tariffs |

| Complex, volatile relationships | Lower precision achievable | May require tests of details as primary evidence |

| Non-financial data available | Independent expectation possible | Reduces reliance on client-controlled financial data |

For example, predicting total rental income from a property portfolio using known rental rates, number of units, and vacancy rates can produce a highly precise expectation, potentially providing persuasive evidence without detailed vouching of individual lease agreements.

7. Analytical Procedures at the End of the Audit

Para. 6 & A17–A19 – The mandatory overall review.

Separate from their role as substantive procedures, ISA 520 mandates that the auditor perform analytical procedures near the end of the audit. The purpose is to assist when forming an overall conclusion about whether the financial statements are consistent with the auditor’s accumulated knowledge of the entity.

These “completion procedures” differ from substantive analytical procedures in their purpose: they are not primarily aimed at detecting individual misstatements, but rather at corroborating conclusions drawn throughout the audit and identifying any previously unrecognised risks.

If end-of-audit analytical procedures reveal unexpected results or relationships, the auditor must investigate, revisiting risk assessments under ISA 315 and considering whether additional audit procedures are required under ISA 330.

Considerations at this stage include reviewing the financial statements as a whole, assessing consistency with prior-period trends, evaluating whether previously noted accounting issues have been adequately resolved, and confirming that the financial statements reflect the auditor’s overall understanding of the entity and its environment.

8. Investigating Unexpected Variances As Per ISA 520

Para. 7 & A20–A21 – What to do when results deviate from expectations.

When analytical procedures reveal fluctuations or relationships that are inconsistent with expectations or with other relevant information gathered during the audit, ISA 520 requires the auditor to investigate.

Step-by-Step Investigation Process

Inquire of Management

Obtain management’s explanations for the unexpected variance. Document the inquiry and evaluate the plausibility of the response in light of the auditor’s understanding of the entity.

Corroborate Management’s Explanations

Management’s explanations must be corroborated with other audit evidence, they cannot be accepted at face value. Obtain documentary or other evidence to support the explanation provided.

Perform Other Audit Procedures If Necessary

If management cannot explain the variance, or if the explanation is implausible, the auditor must design and perform additional audit procedures including tests of details to resolve the matter.

Management responses alone are not sufficient audit evidence. ISA 520 Para. A20 makes clear that the auditor must evaluate management’s explanations against their broader understanding of the entity and corroborate them with independent evidence. An unexplained variance left unresolved is a qualification risk.

If the investigation of unexpected analytical procedure results reveals a previously unrecognised risk of material misstatement, ISA 315 (Revised) requires the auditor to revise the risk assessment and modify the audit plan accordingly.

10. Practical Examples of ISA 520

Example 1: Gross Profit Margin Analysis

An auditor notes that the entity’s gross profit margin has declined from 42% to 31% in the current year with no change in product mix or pricing strategy disclosed by management. This unexpected result triggers an investigation: the auditor inquires of management, reviews purchase contracts, and performs detailed testing of inventory valuation and cut-off. An error in inventory valuation is identified.

Example 2: Interest Expense Verification

Using loan agreement data (principal amounts and applicable interest rates), the auditor independently estimates expected interest expense. Comparing this to the recorded figure provides persuasive evidence regarding the completeness and accuracy of interest expense, significantly reducing the need for detailed vouching of individual interest payments.

Example 3: Predictive Model for Rental Income

For a property company, the auditor builds a rental income expectation: total leasable units × average monthly rent × (1 − vacancy rate) × 12 months. This independently derived figure is compared to recorded revenue. Where the difference exceeds the threshold, the auditor investigates specific lease agreements or vacancies.

Well-designed substantive analytical procedures can provide highly persuasive audit evidence for significant financial statement items, without the time cost of vouching every transaction. When the relationship is stable and data is reliable, reasonableness tests and regression models are genuinely powerful audit tools.

11. Frequently Asked Questions

(Qualified) Chartered Accountant – ICAP

Master of Commerce – HEC, Pakistan

Bachelor of Accounting (Honours) – AeU, Malaysia