IFRS 15 5 step model provides a structured framework for ‘recognizing revenue from customer contracts’. It helps businesses identify obligations, determine transaction prices, and recognize revenue accurately and consistently.

International Financial Reporting Standard

IFRS 15 –

The Five‑Step Revenue

Recognition Model

A definitive, practical guide to applying IFRS 15 5 step model for recognising revenue from contracts with customers, used by entities reporting under IFRS worldwide.

IFRS 15 – Revenue from Contracts with Customers was jointly issued by the IASB and FASB in May 2014 and became mandatory for annual reporting periods beginning on or after 1 January 2018. It replaced IAS 18, IAS 11, and related IFRIC interpretations with a single, comprehensive principle-based standard.

At its core, IFRS 15 establishes that an entity should recognise revenue in a manner that depicts the transfer of promised goods or services to customers in an amount that reflects the consideration to which the entity expects to be entitled in exchange for those goods or services.

To achieve this, the standard prescribes a structured approach as explained by this guide IFRS 15 5 step model that all entities must apply consistently. Each step builds on the last, ensuring revenue is recognised at the right time, in the right amount, and for the right performance obligation.

Core Principle

Revenue is recognised when (or as) an entity satisfies a performance obligation by transferring a promised good or service to a customer. A good or service is transferred when or as the customer obtains control of it.

Why IFRS 15 Matters

IFRS 15 fundamentally shifted how revenue is recognised, moving from a risk-and-rewards model (IAS 18) to a control-transfer model. This change has far-reaching implications across industries: software, construction, telecommunications, real estate, and more. Understanding the five-step model is essential for accountants, auditors, CFOs, and finance professionals worldwide.

IFRS 15 5 Step Model Explained with Examples

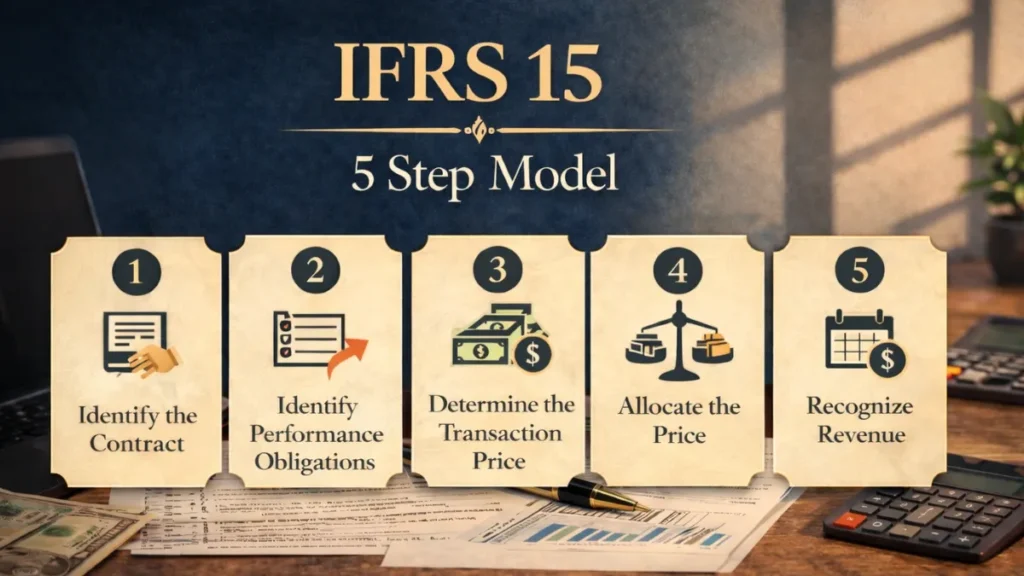

IFRS 15 requires entities to apply the following five steps sequentially to each contract or portfolio of contracts with a customer.

IFRS 15 Five-Step Revenue Recognition Model

Identify the Contract

Identify Performance Obligations

Determine Transaction Price

Allocate Transaction Price

Recognise Revenue

Step One

Identify the Contract (IFRS 15)

A contract is an agreement between two or more parties that creates enforceable rights and obligations. IFRS 15 applies to contracts that meet all five of the following criteria:

- a The parties have approved the contract (written, oral, or implied by customary business practices) and are committed to perform their obligations.

- b Each party’s rights regarding the goods or services to be transferred can be identified.

- c The payment terms for the goods or services to be transferred can be identified.

- d The contract has commercial substance (i.e. the risk, timing, or amount of the entity’s future cash flows is expected to change as a result of the contract).

- e It is probable that the entity will collect the consideration to which it will be entitled in exchange for the goods or services transferred.

Practical Example

A software company signs a written agreement with a client to deliver a customised ERP system for $500,000. Both parties’ rights and payment terms are clear, the contract has commercial substance, and the client has a strong credit history. All five criteria are met, a contract exists under IFRS 15.

IFRS 15 Contract Modifications

When a contract is modified, entities must assess whether the modification creates a new, separate contract or changes an existing one, with different revenue recognition implications for each outcome.

Step Two

Identify Performance Obligations in the Contract

At contract inception, the entity must identify all performance obligations i.e. promises to transfer a distinct good or service (or a series of distinct goods or services that are substantially the same) to the customer.

A good or service is distinct if it meets both of the following criteria:

- ① Capable of being distinct – The customer can benefit from the good or service on its own or together with other readily available resources.

- ② Distinct within the context of the contract – The promise to transfer the good or service is separately identifiable from other promises in the contract.

Practical Example

A telecom company sells a smartphone bundled with a 24-month service plan for a fixed monthly fee. There are two distinct performance obligations: (1) the handset, the customer can use it independently and (2) the network service. Each must be accounted for separately.

Step Three

Determine the Transaction Price

The transaction price is the amount of consideration an entity expects to be entitled to in exchange for transferring promised goods or services, excluding amounts collected on behalf of third parties (such as sales taxes).

To determine the transaction price, entities must consider:

- 1 Variable consideration – Discounts, rebates, refunds, credits, price concessions, incentives, bonuses, or penalties. Estimated using the expected value or most likely amount method, subject to the constraint that significant revenue reversals are not highly probable.

- 2 Significant financing component – If payment timing provides either party with a significant financing benefit, the transaction price must be adjusted to reflect a cash-selling price (applying a discount rate).

- 3 Non-cash consideration – Measured at fair value at contract inception.

- 4 Consideration payable to the customer – Treated as a reduction of the transaction price unless it is payment for a distinct good or service from the customer.

Practical Example

A construction company signs a $10m contract with a $1m performance bonus payable if the project is completed by the deadline. Using the most likely amount method, management assesses there is an 80% chance the bonus will be earned and includes $1m in the transaction price, subject to the variable consideration constraint.

Step Four

Allocate the Transaction Price to Performance Obligations

Once the transaction price is determined, it must be allocated to each performance obligation in proportion to the relative standalone selling prices (SSP) of each distinct good or service.

Standalone selling price is the price at which an entity would sell a promised good or service separately to a customer. When observable prices are not available, entities must estimate SSP using one of the following approaches:

- A Adjusted market assessment approach – Evaluate the market in which goods or services are sold and estimate the price customers in that market would be willing to pay.

- B Expected cost plus margin approach – Forecast expected costs plus an appropriate margin for that good or service.

- C Residual approach – Permitted only when the SSP is highly variable or uncertain; allocated as the residual after allocating SSPs of other obligations.

Practical Example

The telecom company from Step 2 charges a total of $720 over the contract. The handset’s SSP is $400 and the service plan’s SSP is $480 (total: $880). The allocated prices are: Handset = $720 × ($400/$880) = $327; Service = $720 × ($480/$880) = $393.

Step Five

Recognise Revenue When (or As) Performance Obligations Are Satisfied

Revenue is recognised when or as the entity satisfies a performance obligation by transferring control of a promised good or service to the customer. Control can be transferred either over time or at a point in time.

Revenue is recognised over time if any one of the following three criteria is met:

- i The customer simultaneously receives and consumes the benefits as the entity performs (e.g. cleaning services, routine maintenance).

- ii The entity’s performance creates or enhances an asset that the customer controls as the asset is created or enhanced (e.g. construction on the customer’s land).

- iii The entity’s performance does not create an asset with an alternative use, and the entity has an enforceable right to payment for performance completed to date.

If none of these criteria are met, revenue is recognised at the point in time when control transfers; typically on delivery, legal title passing, or physical possession transferring.

Practical Example – Over Time

A law firm provides ongoing legal advisory services. The client receives and consumes the benefit as the lawyers work (criterion i). Revenue is recognised over time, typically using an input method (hours incurred as a percentage of total estimated hours).

Practical Example – Point in Time

A manufacturer delivers a batch of components to a customer. None of the over-time criteria are met. Revenue is recognised at the point the customer gains control, typically on delivery, when the customer can direct the use of and obtain the benefits from the goods.

Scope & Exclusions of IFRS 15

IFRS 15 applies to contracts with customers, but several types of contracts are explicitly excluded from its scope.

Within Scope

- All contracts to provide goods or services to customers

- Partial application where some components are in scope

- Licences of intellectual property

- Construction and long-term service contracts

- Warranties (assurance vs. service-type)

Excluded from Scope

- Lease contracts – IFRS 16

- Insurance contracts — IFRS 17

- Financial instruments – IFRS 9

- Non-monetary exchanges between entities in the same line of business

- Certain collaborative arrangements

IFRS 15 vs IAS 18 Key Differences

Understanding how IFRS 15 changed practice is critical for financial statement preparers and users.

| Aspect | IAS 18 (Old) | IFRS 15 (Current) |

|---|---|---|

| Core Principle | Risks and rewards transfer | Transfer of control |

| Framework | Separate rules for goods, services, interest, royalties | Single five-step model for all contracts |

| Multiple Elements | Limited, rule-based guidance | Comprehensive guidance on identifying and allocating performance obligations |

| Variable Consideration | Recognised when determinable | Estimated and constrained; recognised to the extent it is highly probable there will be no significant reversal |

| Licences | Minimal specific guidance | Detailed guidance, right to use vs right to access |

| Disclosures | Limited | Significantly expanded; disaggregation, contract assets/liabilities, judgements |

Frequently Asked Questions

Answers to the most common questions about the IFRS 15 5 step model.

IFRS 15 had the most significant impact on industries with complex bundled arrangements or long-term contracts: telecommunications (bundled handset/service deals), software and technology (SaaS, licences, implementation), construction and engineering (long-term contracts, claims), real estate (off-plan property sales), and aerospace and defence.

A contract asset arises when an entity has transferred goods or services to a customer but has not yet billed, the entity’s right to consideration is conditional on something other than the passage of time. A contract liability (previously called deferred revenue) arises when a customer has paid before the entity has transferred the related goods or services, the entity has an obligation to perform.

The constraint requires entities to include variable consideration in the transaction price only to the extent it is highly probable that a significant revenue reversal will not occur when the uncertainty is subsequently resolved. This prevents premature recognition of revenue that may need to be reversed. Entities must reassess variable consideration at each reporting date.

IFRS 15 distinguishes between two types: (1) Assurance-type warranties – a guarantee that the product will function as promised (e.g. a 1-year standard warranty). These are accounted for under IAS 37 as a provision, not as a separate performance obligation. (2) Service-type warranties – provide the customer with additional services beyond assurance (e.g. extended warranty with additional coverage). These are separate performance obligations and revenue is allocated to and recognised over the warranty period.

Output methods recognise revenue based on direct measurements of value to the customer such as units produced, milestones reached, or surveys of completion. Input methods recognise revenue based on efforts expended relative to total expected effort such as costs incurred, labour hours, or machine hours. The chosen method must faithfully depict the entity’s performance and be applied consistently.

IFRS 15 and ASC 606 (US GAAP) were developed jointly by the IASB and FASB and are substantially converged, sharing the same five-step framework and core principles. There are a small number of differences in specific areas such as licences of intellectual property, sales with right of return, and certain disclosure requirements but the standards are largely aligned, making them easier to apply for multinational groups.

(Qualified) Chartered Accountant – ICAP

Master of Commerce – HEC, Pakistan

Bachelor of Accounting (Honours) – AeU, Malaysia