Lessee accounting a concept that explains the way by which a lessee records the financial impacts of its leasing activities. As per IFRS 16, lessees recognize ‘right of use’ asset (RoU) and ‘lease liability’, reflecting the present value (PV) of future lease payments.

Lessee Accounting:

The Complete Guide

A practitioner’s guide to recognising right-of-use assets and lease liabilities, classifying operating and finance leases, preparing journal entries, and satisfying disclosure requirements under ASC 842 and IFRS 16.

What Is Lessee Accounting?

Lessee accounting refers to the set of accounting principles, recognition criteria, and measurement requirements that govern how a lessee, the party that obtains the right to use an asset records leases in its financial statements. Under modern standards, the days of keeping operating leases entirely off the balance sheet are largely over.

The two governing frameworks are ASC 842 (issued by the Financial Accounting Standards Board for US GAAP entities) and IFRS 16 (issued by the International Accounting Standards Board for IFRS entities). Both standards require lessees to bring the vast majority of leases onto the balance sheet, fundamentally changing how investors and analysts evaluate leverage and asset intensity.

An entity that obtains the right to use an underlying asset for a period of time in exchange for consideration. The lessee does not acquire ownership of the asset but controls its use during the lease term under the terms agreed with the lessor.

Before ASC 842 and IFRS 16, companies could structure operating leases to remain off-balance-sheet, creating what analysts called “off-balance-sheet financing.” The new standards largely eliminated this, requiring lessees to recognise a right-of-use (ROU) asset and a corresponding lease liability for virtually all leases.

Who Is Affected?

Any entity that enters into an arrangement where it controls the use of an identified asset for a period of time in exchange for consideration is a lessee and must apply lessee accounting. This includes leases of:

- Real estate (offices, warehouses, retail spaces)

- Equipment (machinery, vehicles, medical devices)

- Aircraft and marine vessels

- IT infrastructure and data centre space

- Embedded leases within service contracts

Lease Classification in Lessee Accounting

Under ASC 842, lessees must classify each lease as either an operating lease or a finance lease at the commencement date. The classification determines how expenses are recognised in the income statement and how the ROU asset is amortised.

A lease is classified as a finance lease if any one of the following five criteria is met:

The lease transfers ownership of the underlying asset to the lessee by the end of the lease term.

The lessee has an option to purchase the underlying asset that the lessee is reasonably certain to exercise.

The lease term covers the major part of the remaining economic life of the underlying asset. ASC 842 does not define “major part”; 75% is a common practical threshold.

The present value of lease payments equals or exceeds substantially all of the fair value of the underlying asset. 90% is a common practical threshold.

The underlying asset is of such a specialised nature that it is expected to have no alternative use to the lessor at the end of the lease term.

If none of the five criteria are met, the lease is classified as an operating lease. Under IFRS 16, there is only one lessee model, all leases are treated similarly to what US GAAP calls a finance lease, with limited exceptions.

Initial Recognition of Lease Liabilities and ROU Assets

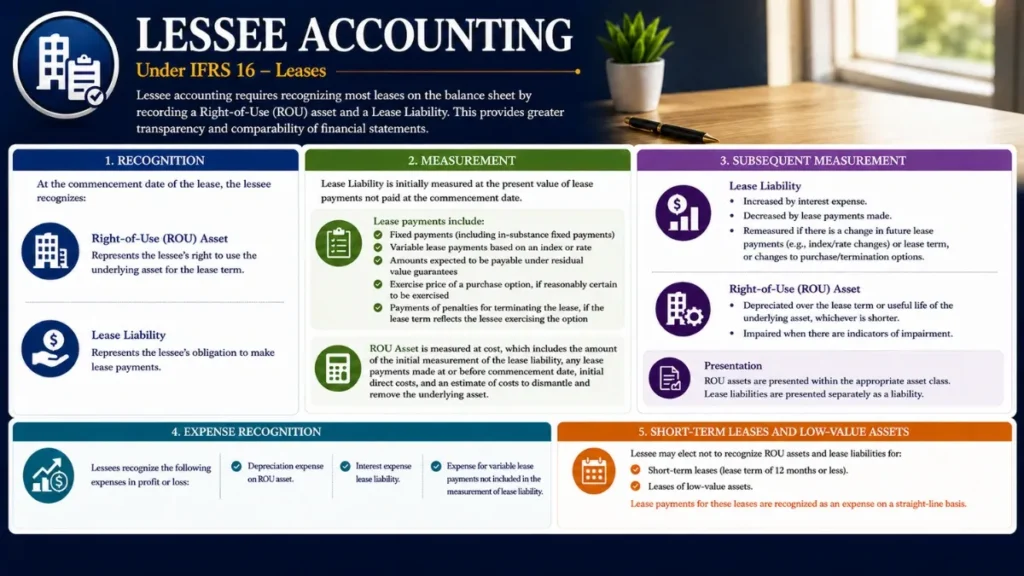

At the commencement date, the date on which the lessor makes the underlying asset available for use, the lessee recognises both a right-of-use (ROU) asset and a lease liability, regardless of lease classification (operating or finance).

Measuring the Lease Liability

The lease liability is initially measured at the present value of lease payments not yet made, discounted using the rate implicit in the lease. If that rate cannot be readily determined, the lessee uses its incremental borrowing rate (IBR), the rate at which it could borrow a similar amount over a similar term with similar security.

Lease payments included in the measurement are:

- Fixed payments (less any lease incentives receivable)

- Variable payments that depend on an index or rate

- Exercise price of a purchase option the lessee is reasonably certain to exercise

- Payments for penalties for terminating the lease, if the lease term reflects exercise of a termination option

- Residual value guarantees the lessee is expected to make

Measuring the ROU Asset

The ROU asset is initially measured at the initial amount of the lease liability, adjusted for:

- Plus: Lease payments made at or before the commencement date

- Plus: Initial direct costs incurred by the lessee

- Plus: Estimated costs of dismantling/restoring the site (if an obligation exists)

- Less: Lease incentives received

Operating Lease Accounting for Lessees

For operating leases under ASC 842, the income statement presentation is distinctly different from a finance lease. The lessee recognises a single straight-line lease expense over the lease term, even though the underlying liability is accreting on an effective interest basis.

Subsequent Measurement – Operating Lease

After the commencement date, the lessee measures the operating lease:

- The lease liability increases each period for interest accrued and decreases by cash payments made.

- The ROU asset is measured as the carrying amount of the lease liability, adjusted for prepaid/accrued rent, unamortised lease incentives, and remaining unamortised initial direct costs. In effect, the ROU asset is a “plug” that ensures straight-line expense recognition.

Operating lease expense is presented as a single line item within operating expenses (often rent or occupancy expense). It does not bifurcate into depreciation and interest components, a key distinction from finance lease accounting.

Balance Sheet Classification

Operating lease ROU assets are typically presented separately from property, plant and equipment. Lease liabilities are split between current (amounts due within 12 months) and non-current, classified separately from finance lease liabilities.

Finance Lease Accounting for Lessees

Finance leases under ASC 842 (and all leases under IFRS 16) mirror the accounting treatment that was historically applied to capital leases under ASC 840. The lessee recognises two separate expenses: amortisation of the ROU asset and interest on the lease liability.

Subsequent Measurement – Finance Lease

- The lease liability accretes using the effective interest method, interest is recognised each period and cash payments reduce the liability.

- The ROU asset is amortised on a straight-line basis (or another systematic basis if more representative of the pattern of use) over the shorter of the lease term or the useful life of the asset.

Front-Loaded Expense Profile

A distinguishing feature of finance lease accounting is the front-loaded total expense profile. Because interest is highest in the early periods (when the liability balance is highest), total combined expense (amortisation + interest) is greater in earlier years and declines over time, unlike the straight-line expense of an operating lease.

- Single lease expense line

- Straight-line over lease term

- Reported in operating expenses

- No bifurcation into interest & depreciation

- Amortisation of ROU asset

- Interest on lease liability

- Front-loaded expense profile

- Interest often below operating line (EBIT impact)

Lessee Accounting Journal Entries and Examples

The following illustrative example cover the most common transactions in lessee accounting. Assume a 5-year lease with annual payments of $50,000, an IBR of 5%, and initial direct costs of $2,000.

At Commencement Date

End of Year 1 – Operating Lease

End of Year 1 – Finance Lease

Subsequent Measurement and Lease Modifications

After initial recognition, both the ROU asset and lease liability may need to be remeasured when certain events occur. These trigger points are critical to monitor throughout the lease term.

Events Requiring Remeasurement of the Lease Liability

- A change in the lease term (e.g., exercise or non-exercise of an extension or termination option that the lessee was previously not reasonably certain to take)

- A change in the probability of exercising a purchase option

- A change in the amounts expected to be payable under a residual value guarantee

- A change in an index or rate used to determine variable lease payments

Upon remeasurement, the lessee adjusts the lease liability to reflect the revised lease payments and adjusts the ROU asset by a corresponding amount (unless the carrying amount of the ROU asset is reduced to zero, in which case any remaining adjustment is recognised in profit or loss).

Lease Modifications

A lease modification is a change in the scope of a lease or the consideration for a lease that was not part of the original terms. Depending on whether the modification grants the lessee an additional right of use not included in the original lease and whether it is at a price commensurate with its standalone price, it may be accounted for as a separate new lease or as a modification to the existing lease.

Short-Term and Low-Value Lease Exemptions

Both ASC 842 and IFRS 16 provide practical expedients that allow lessees to avoid recognising an ROU asset and lease liability for certain leases.

Short-Term Lease Exemption (ASC 842 & IFRS 16)

A lessee may elect not to apply the recognition requirements to leases with a lease term of 12 months or less at the commencement date (and no purchase option the lessee is reasonably certain to exercise). If elected, the lessee recognises lease payments in profit or loss on a straight-line basis over the lease term.

The election must be made by class of underlying asset under ASC 842, and by asset class under IFRS 16. Once made, it applies to all qualifying leases within that class and must be disclosed.

Low-Value Asset Exemption (IFRS 16 Only)

IFRS 16 provides an additional exemption for leases of low-value assets, assets with an underlying value of approximately USD 5,000 or less when new, such as tablets, personal computers, and small office furniture. This exemption is available on a lease-by-lease basis and is not available under ASC 842.

IFRS 16 vs ASC 842 Lessee Accounting

While IFRS 16 and ASC 842 share the same fundamental objective, their lessee accounting models differ in important respects that can significantly affect financial statement comparability.

| Topic | ASC 842 (US GAAP) | IFRS 16 |

|---|---|---|

| Lessee classification model | Dual model: operating & finance leases | Single model: all leases treated as finance-type |

| Income statement – operating lease | Single straight-line expense in operating costs | Not applicable, no operating lease category |

| Income statement – finance/all leases | Depreciation + interest (finance leases only) | Depreciation + interest for all leases |

| Low-value asset exemption | Not available | Available (≈ USD 5,000 when new) |

| Discount rate | Rate implicit in lease or IBR | Rate implicit in lease or IBR; subsidiaries of groups may use parent’s rate |

| Subleases | Classified based on underlying asset | Classified based on ROU asset |

| Sale & leaseback | Gain recognition depends on classification | Gain recognition based on proportion of rights transferred |

| EBITDA impact | Operating leases leave EBITDA unchanged (rent = operating expense) | All leases improve EBITDA (depreciation + interest replace rent) |

Disclosure Requirements for Lessees

Both standards require extensive disclosures designed to give financial statement users a basis to assess the effect that leases have on the lessee’s financial position, financial performance, and cash flows. The disclosure objective is paramount, entities must provide qualitative and quantitative information to satisfy it.

Quantitative Disclosures (ASC 842)

- Lease costs (operating, finance, short-term, variable, sublease income)

- Cash paid for lease liabilities (operating and financing activities)

- ROU assets obtained in exchange for new lease liabilities (non-cash investing)

- Weighted average remaining lease term and weighted average discount rate (separately for operating and finance leases)

- Maturity analysis of lease liabilities with annual undiscounted cash flows for each of the next five years and thereafter, reconciled to the carrying amount

Qualitative Disclosures

- General description of the nature of leasing activities

- Basis, terms, and conditions of variable lease payments

- Existence and terms of extension and termination options, and how they are assessed

- Residual value guarantees provided by the lessee

- Restrictions or covenants imposed by leases

- Sale and leaseback transactions

Many regulators have scrutinised lease disclosures for boilerplate language. Disclosures should be entity-specific and reflect the actual risks and economics of the lessee’s lease portfolio rather than reproducing standard language verbatim.

Common Lessee Accounting Errors to Avoid

Lessee accounting is complex in practice, and errors can materially misstate both the balance sheet and income statement. The following are among the most frequently encountered mistakes.

- Failing to identify embedded leases. Service contracts often contain embedded leases (e.g., dedicated equipment in an outsourcing arrangement). A thorough contract review is essential at commencement and upon modification.

- Incorrectly determining the lease term. Non-cancellable periods, extension options reasonably certain of exercise, and termination options must all be considered. Entities often underestimate the lease term by ignoring options that economic incentives suggest will be exercised.

- Using an inappropriate discount rate. The IBR should reflect the lessee’s credit risk and the collateral represented by the leased asset. Using a corporate bond rate without adjustment is a common error.

- Misclassifying leases. Misjudging whether a lease meets the finance lease criteria can lead to incorrect income statement presentation and cash flow classification.

- Failing to reassess at trigger events. Changes in facts and circumstances such as significant lessee improvements to the asset or changes in business plans may require reassessment of the lease term or classification.

- Errors in the maturity analysis. Including variable payments that are excluded from the lease liability, or excluding guaranteed residuals, distorts the maturity schedule disclosed in the notes.

Frequently Asked Questions

What is a right-of-use (ROU) asset in lessee accounting?

What is the incremental borrowing rate (IBR) and how is it determined?

Do all leases need to be recognised on the balance sheet?

How does lessee accounting affect financial ratios?

What happens when a lease is modified?

How is lessee accounting presented in the cash flow statement?

What is the difference between a lease and a service contract?

Lessee Accounting Has Permanently Changed the Balance Sheet Landscape

With ASC 842 and IFRS 16 now fully adopted by public and private entities alike, lessee accounting demands rigorous identification of lease contracts, disciplined determination of the incremental borrowing rate, and careful ongoing monitoring of remeasurement triggers. Mastery of these standards is no longer optional for finance teams, it is a baseline competence for credible financial reporting.

(Qualified) Chartered Accountant – ICAP

Master of Commerce – HEC, Pakistan

Bachelor of Accounting (Honours) – AeU, Malaysia