IFRS 15 illustrative examples help explain how the ‘revenue recognition’ standard (IFRS 15) is applied in real-world accounting scenarios. These examples demonstrate the practical application of the five-step revenue recognition model as well, making complex concepts easier to understand.

IFRS 15 Illustrative Examples – Revenue from Contracts with Customers

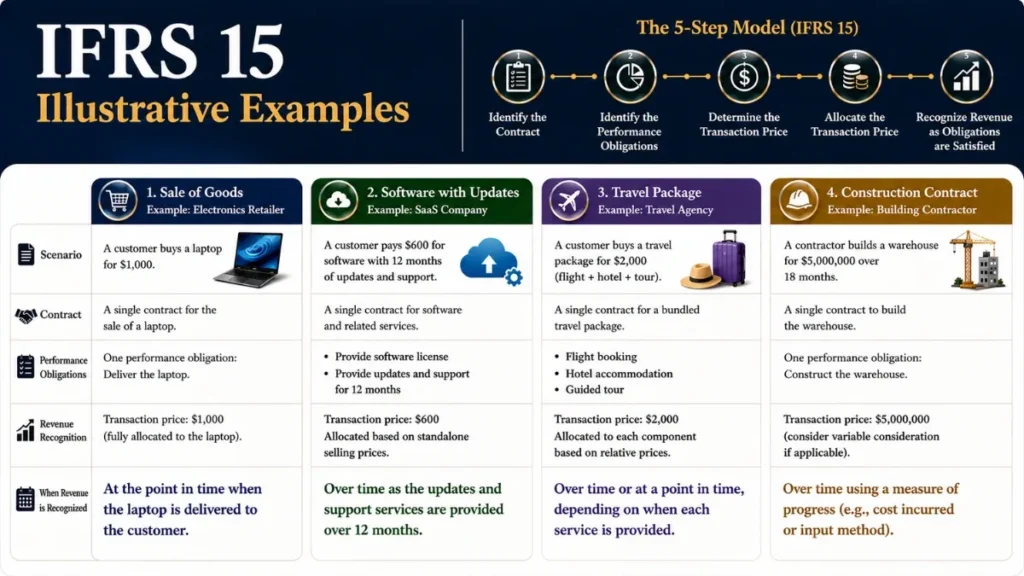

Practical, worked examples of the five-step revenue recognition model under IFRS 15, including journal entries, allocation tables, and industry-specific scenarios.

IFRS 15 Five-Step Revenue Recognition Model

IFRS 15 issued by IASB introduced a single, principles-based framework for recognising revenue from contracts with customers, replacing the fragmented guidance of IAS 18 and IAS 11. At its core lies a sequential five-step model that must be applied to every contract (or portfolio of similar contracts).

Core principle (IFRS 15.IN7): An entity shall recognise revenue to depict the transfer of promised goods or services to customers in an amount that reflects the consideration to which the entity expects to be entitled in exchange for those goods or services.

Step One Identify the Contract with a Customer

A contract exists when five criteria are met simultaneously:

- The parties have approved the contract and are committed to their obligations.

- Each party’s rights regarding the goods or services can be identified.

- Payment terms for the goods or services can be identified.

- The contract has commercial substance (i.e., risk, timing or amount of future cash flows is expected to change).

- It is probable that the entity will collect the consideration.

IFRS 15 Illustrative Examples → Example 1.1 – Software Licensing Agreement

TechCorp Ltd enters into a written agreement with a customer to license enterprise software for 3 years for a fixed fee of $120,000. The customer has a good credit history and the contract is signed by both parties. There is no right of return.

a) Approval & commitment: Both parties signed – criterion met.

b) Rights identified: 3-year software licence clearly described – met.

c) Payment terms: $120,000 fixed fee, payable annually – met.

d) Commercial substance: Cash inflow of $120,000 and IP risk transfer – met.

e) Collectability: Good credit history, no significant doubt – met.

All five criteria are satisfied. A contract with a customer exists under IFRS 15.9. TechCorp proceeds to apply the remaining four steps.

Example 1.2 – Collectability in Doubt

RetailCo sells goods to a new customer on credit for $50,000. The customer has no credit history and operates in a financially distressed sector. Significant doubt exists about whether the customer can pay.

Criteria (a)-(d) are met. However, criterion (e) collectability, is not satisfied because it is not probable that RetailCo will collect $50,000.

Step Two Identify Performance Obligations

A performance obligation is a promise to transfer a distinct good or service (or bundle) to the customer. A good or service is distinct if both conditions are met: (i) the customer can benefit from it on its own or with readily available resources; and (ii) the promise is separately identifiable from other promises in the contract.

IFRS 15 Illustrative Examples → Example 2.1 – Bundled Software Sale (Distinct Obligations)

SoftHouse Ltd agrees to: (1) deliver a software licence, (2) provide implementation services, and (3) supply 12 months of post-implementation support, all for a combined price of $300,000.

Software licence: Customer can benefit from the licence independently (it runs on standard hardware). It is separately identifiable, no significant integration with other services. → Distinct.

Implementation services: These are generic consulting services available from other providers. Customer can benefit without post-implementation support. → Distinct.

Support (12 months): Separately available in the market; customer benefits from it independent of the other deliverables. → Distinct.

Three separate performance obligations are identified. Revenue will be allocated and recognised individually for each obligation.

Example 2.2 – Highly Integrated Services (Not Distinct)

BuildRight Ltd contracts to design and construct a specialised offshore oil platform for $50 million. The design and construction phases are highly interdependent and integrated.

Design and construction are not separately identifiable, each significantly modifies and customises the other. The customer cannot use the design alone without BuildRight’s specialised construction expertise. The services together constitute a single integrated output.

A single performance obligation exists: design-and-construct the offshore platform. Revenue is recognised as this combined obligation is satisfied over time using the percentage-of-completion method.

Step Three Determine the Transaction Price

The transaction price is the amount an entity expects to be entitled to in exchange for transferring goods or services, excluding amounts collected on behalf of third parties. Key considerations include variable consideration, significant financing components, non-cash consideration, and consideration payable to the customer.

IFRS 15 Illustrative Examples → Example 3.1 – Volume Rebate (Variable Consideration)

PharmaDist sells medicines to a hospital group. The list price is $1,000 per unit. If cumulative purchases reach 1,000 units in the year, a 10% retrospective rebate applies. Based on historical data, there is an 80% probability of reaching the threshold.

Two possible outcomes:

Outcome A (80%): 1,000 units × $1,000 × 90% = $900,000

Outcome B (20%): 1,000 units × $1,000 × 100% = $1,000,000

Expected value = (80% × $900,000) + (20% × $1,000,000) = $720,000 + $200,000 = $920,000

Apply the constraint: include variable consideration only to the extent that a significant reversal is not probable. $920,000 passes the constraint test.

Transaction price = $920,000. PharmaDist recognises a refund liability of $80,000 (reflecting the rebate provision) as sales are made.

Example 3.2 – Significant Financing Component

MachineCo sells a specialised machine for cash payment deferred 2 years after delivery. The contract price is $121,000. The customer’s borrowing rate is 10% p.a.

Present value of $121,000 in 2 years at 10%:

PV = $121,000 ÷ (1.10)² = $121,000 ÷ 1.21 = $100,000

Financing component = $121,000 − $100,000 = $21,000

| Date | Account | Dr ($) | Cr ($) |

|---|---|---|---|

| Delivery | Receivable – PV | 100,000 | — |

| Revenue | — | 100,000 | |

| Yr 1 | Receivable (unwinding) | 10,000 | — |

| Finance Income | — | 10,000 | |

| Yr 2 | Receivable (unwinding) | 11,000 | — |

| Finance Income | — | 11,000 | |

| Settlement | Cash | 121,000 | — |

| Receivable | — | 121,000 |

Step Four Allocate the Transaction Price

When a contract contains multiple performance obligations, the transaction price is allocated to each obligation in proportion to its relative standalone selling price (SSP). The SSP is the price at which an entity would sell the good or service separately. Estimation methods include adjusted market assessment, expected cost plus margin, and residual approach.

IFRS 15 Illustrative Examples → Example 4.1 – Telecom Bundle (SSP Allocation)

TeleLink offers a bundle: a handset + 24-month airtime plan for a combined contract price of $720. The handset’s SSP is $480 and the plan’s SSP is $480 (i.e., $20/month × 24 months), giving total SSP of $960.

| Performance Obligation | SSP ($) | SSP % | Allocated Price ($) |

|---|---|---|---|

| Handset (Hardware) | 480 | 50% | 360 |

| Airtime Plan (24 months) | 480 | 50% | 360 |

| Total | 960 | 100% | 720 |

On handset delivery, recognise $360 immediately. The remaining $360 is recognised ratably over 24 months ($15/month) as the airtime plan is provided.

| Event | Account | Dr ($) | Cr ($) |

|---|---|---|---|

| Handset delivery | Cash / Receivable | 720 | — |

| Revenue – Handset | — | 360 | |

| Contract Liability (Deferred) | — | 360 | |

| Each month | Contract Liability | 15 | — |

| Revenue – Airtime | — | 15 |

Example 4.2 – Residual Approach (Highly Variable SSP)

CloudSoft bundles a known SaaS subscription ($200/yr SSP) with a new AI add-on whose SSP is highly variable (sold to different customers at prices ranging from $50 to $500). Bundle price = $380.

Allocate known SSP first: SaaS subscription → $200

Residual allocation to AI add-on = $380 − $200 = $180

Step Five Recognise Revenue Under IFRS 15 When (or As) a Performance Obligation Is Satisfied

Revenue is recognised when control of a promised good or service transfers to the customer, either at a point in time or over time. An obligation is satisfied over time if any one of three criteria is met.

- The customer simultaneously receives and consumes the benefits as the entity performs.

- The entity’s performance creates or enhances an asset that the customer controls as it is created.

- The entity’s performance does not create an asset with an alternative use and the entity has an enforceable right to payment for performance completed to date.

IFRS 15 Illustrative Examples → Example 5.1 – Long-term Construction Contract (Over Time)

ConstructPro Ltd enters a $10 million contract to build a bridge for a municipality over 3 years. Total estimated costs: $8 million. At end of Year 1, costs incurred = $2.4 million. The municipality controls the bridge as it is constructed (criterion ii above).

Percentage complete = $2.4M ÷ $8M = 30%

Revenue to recognise in Year 1 = 30% × $10M = $3,000,000

Gross profit in Year 1 = $3,000,000 − $2,400,000 = $600,000

| Year 1 Entry | Account | Dr ($) | Cr ($) |

|---|---|---|---|

| Costs incurred | Contract Asset (WIP) | 2,400,000 | — |

| Cash / Payables | — | 2,400,000 | |

| Revenue recognition | Receivable / Contract Asset | 3,000,000 | — |

| Revenue | — | 3,000,000 | |

| Cost recognition | Cost of Sales | 2,400,000 | — |

| Contract Asset (WIP) | — | 2,400,000 |

Example 5.2 – Sale of Goods (Point in Time)

AutoParts Ltd ships components to a dealer on DAP (Delivered at Place) terms. The contract price is $250,000. Risk and title transfer when goods are delivered and accepted at the dealer’s warehouse.

Right to payment: Arises upon delivery and acceptance – met at delivery.

Physical possession: Dealer takes possession at their warehouse – met at delivery.

Legal title: Transfers per contract at delivery – met.

Risks & rewards: DAP, risk transfers at delivery – met.

Customer acceptance: Acceptance confirmed on delivery – met.

All control indicators are met at the point of delivery. AutoParts recognises $250,000 revenue when the goods are delivered and accepted at the dealer’s premises.

Variable Consideration Examples Under IFRS 15

Variable consideration arises from discounts, rebates, refunds, credits, price concessions, incentives, performance bonuses, penalties, or contingencies. IFRS 15 requires variable consideration to be estimated using either: (a) the expected value method or (b) the most likely amount method, whichever better predicts the amount.

Example 6.1 – Performance Bonus (Most Likely Amount)

DataPro Ltd agrees to implement an ERP system for $500,000, with a $50,000 bonus if the system goes live within 6 months. DataPro has successfully delivered 9 of its last 10 ERP projects on time. There are only two possible outcomes: earn the bonus or not.

With a binary outcome and strong track record, the most likely amount method applies. Most likely outcome = bonus earned ($50,000). Constraint test: given the 90% success rate, a significant revenue reversal is not probable.

Transaction price = $500,000 + $50,000 = $550,000

DataPro includes the $50,000 bonus in the transaction price and recognises $550,000 of revenue over the implementation period. If the bonus becomes unlikely, the transaction price is revised downward.

Example 6.2 – Right of Return

FashionRetail sells 1,000 shirts at $80 each ($80,000 total). Based on historical data, 5% (50 shirts) will be returned within 30 days. Cost per shirt is $50.

Revenue = 950 shirts × $80 = $76,000

Refund liability = 50 × $80 = $4,000

Return asset (inventory recovery) = 50 × $50 = $2,500

Cost of sales = 950 × $50 = $47,500

| Entry | Account | Dr ($) | Cr ($) |

|---|---|---|---|

| Sale | Cash | 80,000 | — |

| Revenue | — | 76,000 | |

| Refund Liability | — | 4,000 | |

| COGS | Cost of Sales | 47,500 | — |

| Return Asset | 2,500 | — | |

| Inventory | — | 50,000 |

IFRS 15 Licensing Examples

IFRS 15 distinguishes between two types of IP licence, each with different revenue recognition timing:

Example 7.1 – Film Franchise Licence

MediaGiant licenses its film franchise IP to a toy manufacturer for 3 years for $3 million. MediaGiant will continue to produce new films and market the franchise throughout the licence period, significantly affecting the IP’s value.

MediaGiant’s ongoing activities (new films, marketing) are expected to significantly affect the IP. The customer has a right to access the IP as it evolves. → Right to access licence.

Recognise $1,000,000 per year over the 3-year licence term (straight-line, unless another systematic basis better reflects the pattern of transfer).

Example 7.2 – Static Software Licence

LegacySoft grants a perpetual licence to use version 4.2 of its accounting software for a one-time fee of $50,000. No ongoing updates or support are included. The vendor has no plans to update version 4.2.

The customer obtains the right to use the software as it exists at the grant date. LegacySoft’s activities will not affect the customer’s use of version 4.2. Recognise $50,000 at the licence grant date.

Contract Cost Examples Under IFRS 15

IFRS 15 also addresses the treatment of costs incurred to obtain and fulfil contracts. Incremental costs of obtaining a contract are capitalised as an asset if they are expected to be recovered; practical expedient allows immediate expensing if the amortisation period would be 12 months or less.

Example 8.1 – Sales Commissions Capitalised

CloudSub pays a sales agent $6,000 commission upon signing a new customer to a 3-year SaaS contract worth $72,000. The commission would not have been paid had the contract not been obtained. The company also incurs $1,500 in legal fees to review the contract.

Sales commission ($6,000): Incremental cost (would not be incurred without the contract) and expected to be recovered → Capitalise and amortise over 3 years.

Legal fees ($1,500): Not incremental to obtaining the contract (would have been incurred regardless) → Expense as incurred.

| Entry | Account | Dr ($) | Cr ($) |

|---|---|---|---|

| Contract signing | Contract Cost Asset | 6,000 | — |

| Legal Fees Expense | 1,500 | — | |

| Cash | — | 7,500 | |

| Each year (×3) | Amortisation Expense | 2,000 | — |

| Contract Cost Asset | — | 2,000 |

Practical Expedient (IFRS 15.94): An entity may expense incremental costs of obtaining a contract immediately if the amortisation period would be 12 months or less, a useful simplification for short-cycle contracts.

(Qualified) Chartered Accountant – ICAP

Master of Commerce – HEC, Pakistan

Bachelor of Accounting (Honours) – AeU, Malaysia