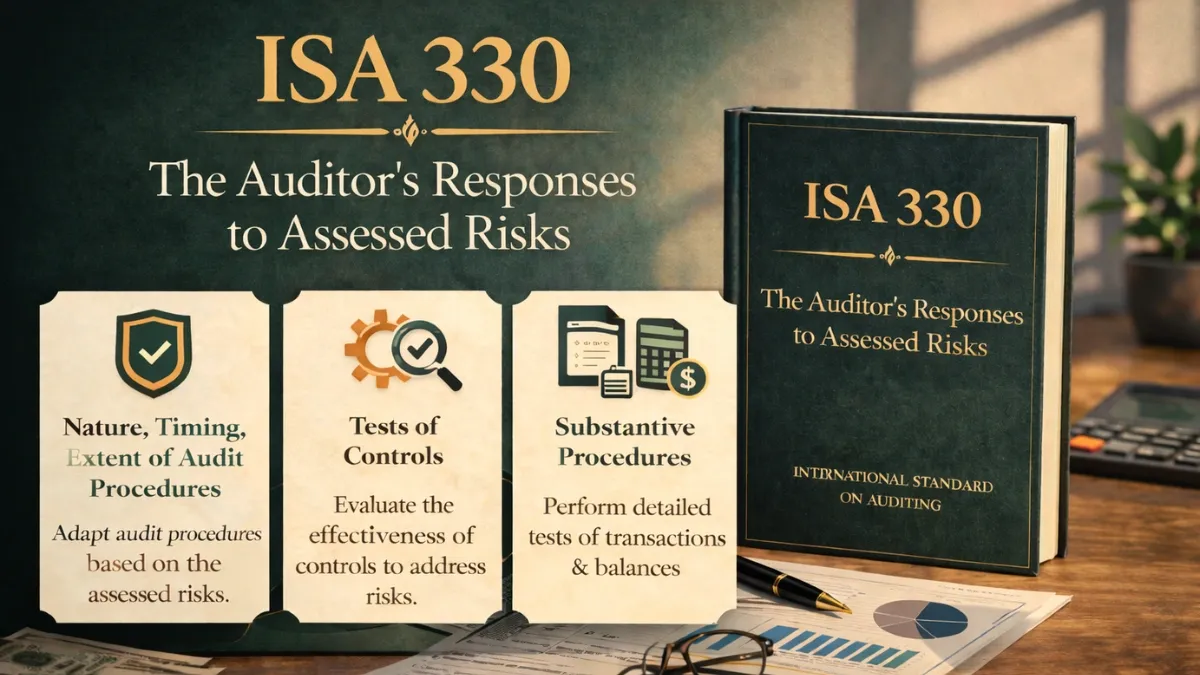

ISA 330 – The Auditor’s Responses to Assessed Risks

ISA 330 focuses on how auditors ‘design’ and ‘implement’ procedures to address identified risks in financial statements. It requires appropriate responses through tests of controls and substantive procedures to obtain sufficient audit evidence. Understanding ISA 330 is essential for improving audit effectiveness, risk management, and overall audit quality. International Standards … Read More