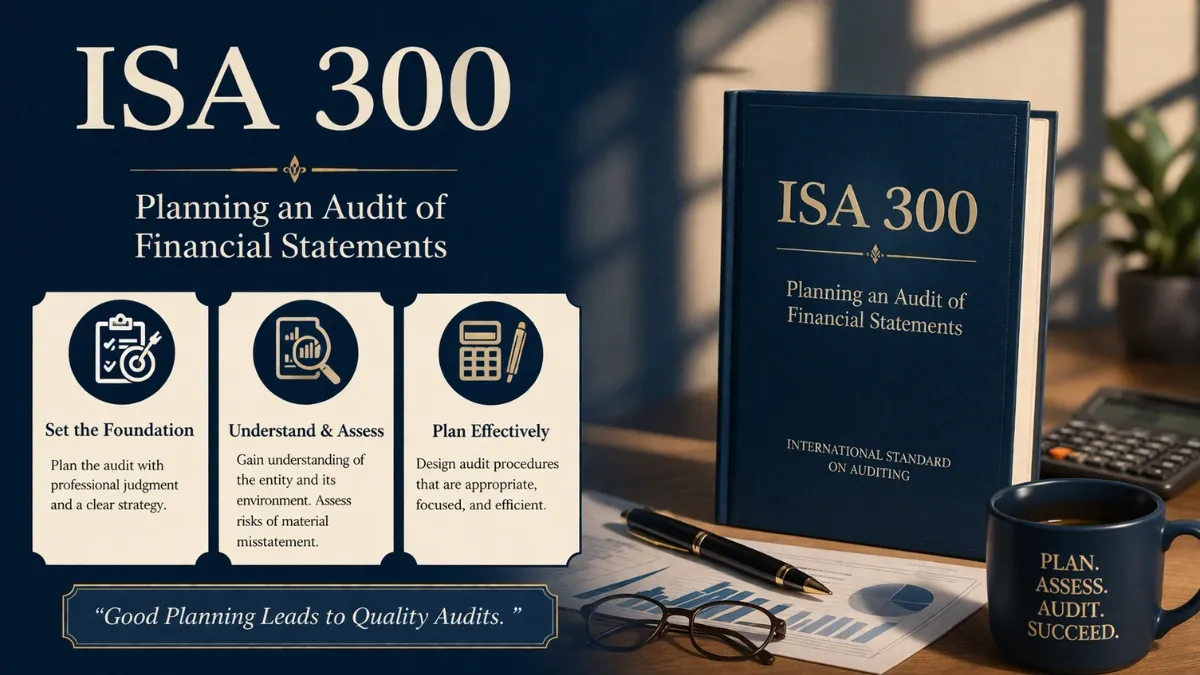

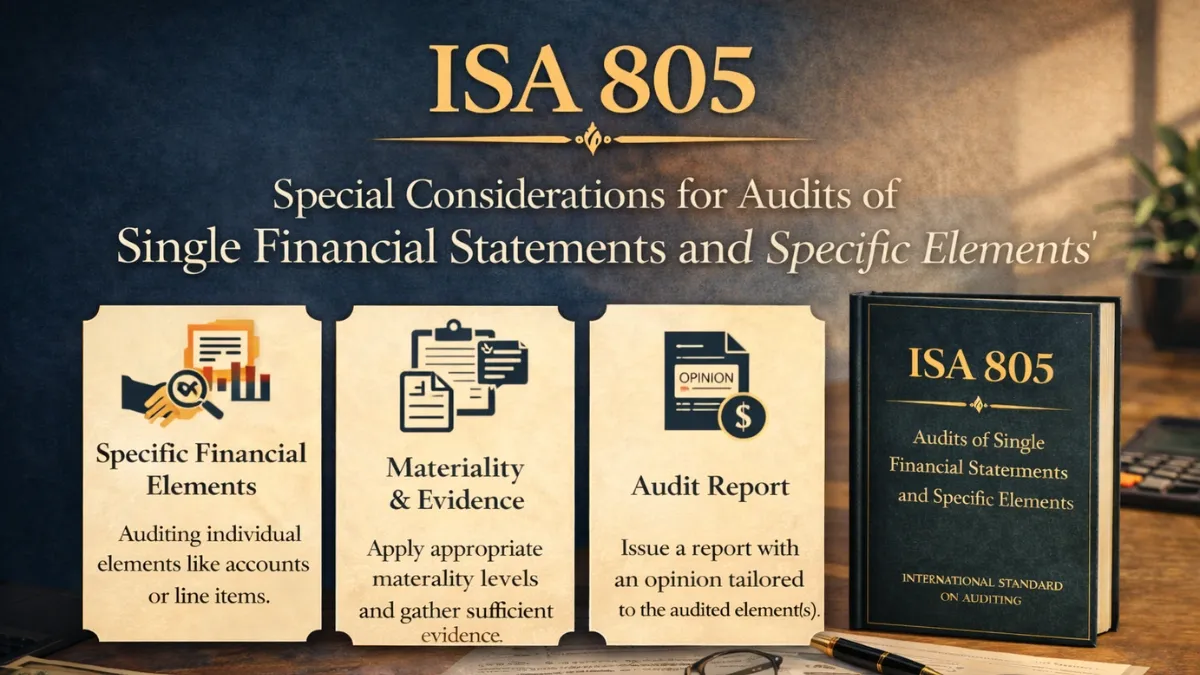

ISA 805 (Revised) – Special Considerations: Audits of Single Financial Statements and Specific Elements, Accounts or Items of a Financial Statement

ISA 805 (Revised) deals with special considerations in the application of ISAs 100-700 to an audit of a ‘single financial statement’ or of a ‘specific element’, ‘account’ or ‘item’ of a financial statement. International Standards on Auditing ISA 805 – Special Considerations Audits of Single Financial Statements and Specific Elements, … Read More