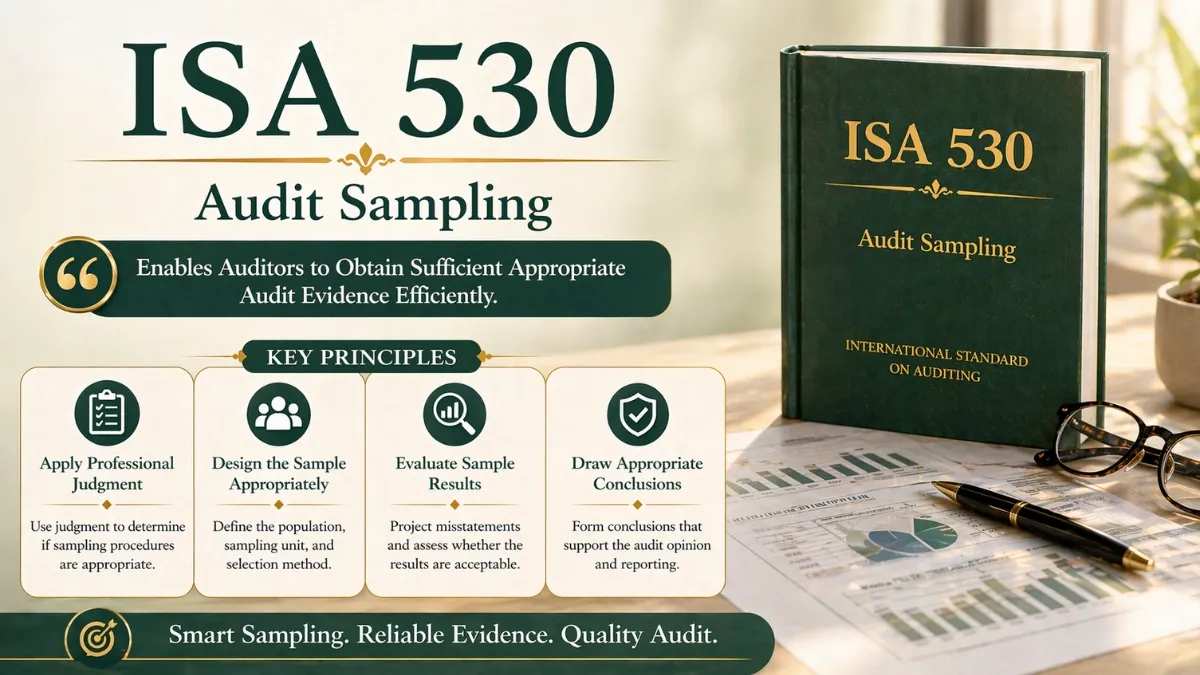

ISA 530 – Audit Sampling

ISA 530 applies when the auditor has decided to use “audit sampling” in performing audit procedures. Home › Audit › ISA 530 International Standard on Auditing ISA 530Audit Sampling A practitioner-level guide covering sample design, size determination, selection methods, projecting misstatements, and evaluating results, everything auditors need to apply ISA … Read More