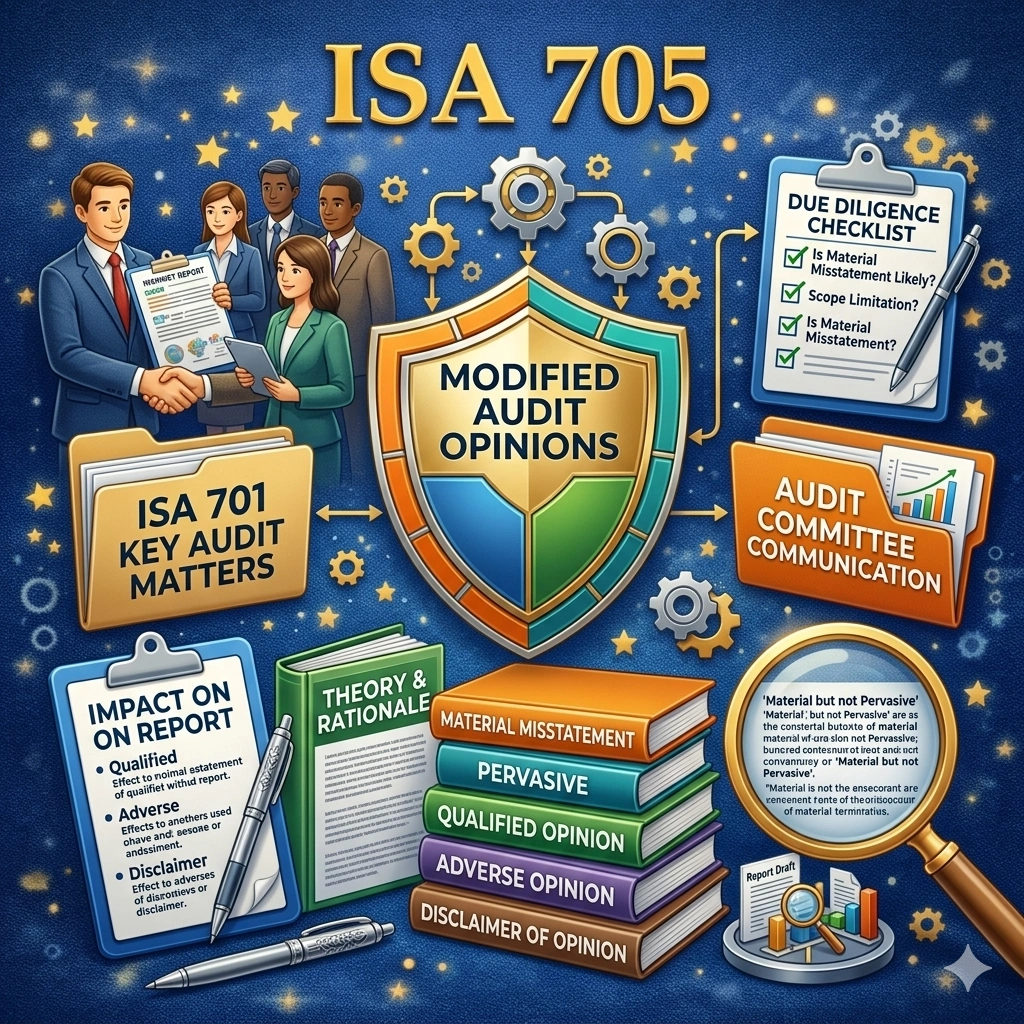

ISA 260 (Revised) – Communication With Those Charged With Governance

ISA 260 (Revised) DEALS with the auditor’s responsibility to COMMUNICATE with those charged with governance in an ‘Audit‘ of Financial Statements. International Standard on Auditing Issued By IAASB (IFAC) Revised 2016 (Revised) Applies To All Audits of Financial Statements Related Standards ISA 265, ISA 700, ISA 705 Contents Overview Objectives … Read More