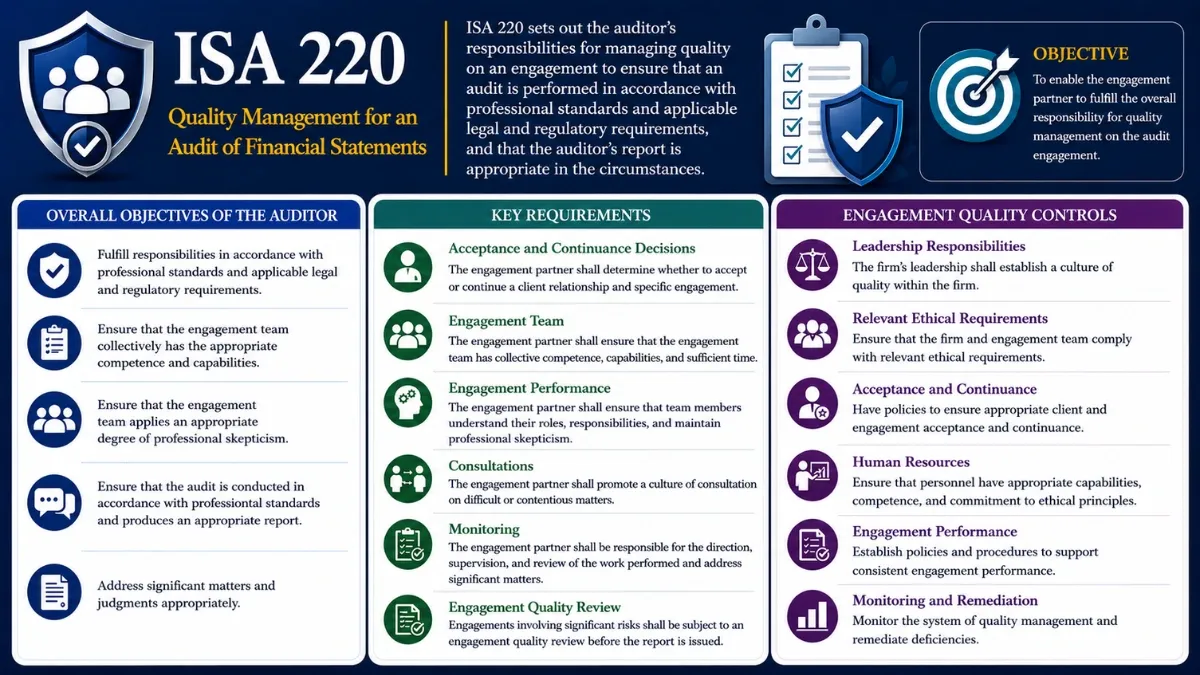

ISA 220 (Revised) – Quality Management for an Audit of Financial Statements

ISA 220 (Revised) deals with the specific responsibilities of the auditor regarding ‘quality management’ for an audit of financial statements. International Standards on Auditing · IAASB · Quality Management Series International Standard on Auditing ISA 220 – Quality Management for an Audit of Financial Statements A definitive guide to understanding … Read More