The objective of IAS 40 is to prescribe the accounting treatment for investment property and related disclosure requirements.

IAS 40 – Investment Property

A definitive guide to IAS 40: understanding its scope, recognition criteria, measurement models, transfers, and disclosure requirements under International Financial Reporting Standards.

1. What is IAS 40?

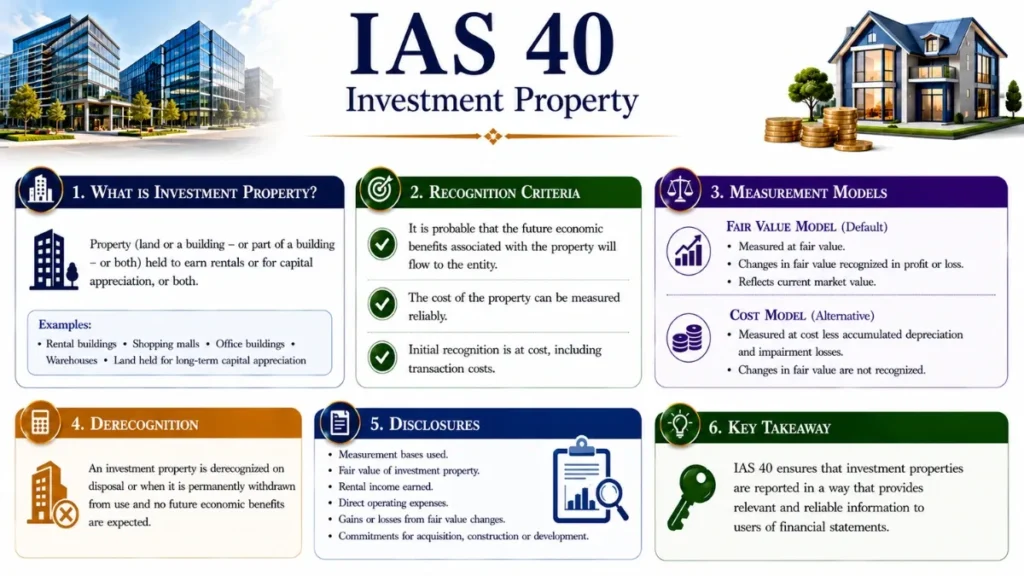

IAS 40 – Investment Property is an International Financial Reporting Standard issued by the International Accounting Standards Board (IASB). It prescribes the accounting treatment for investment property and the related disclosure requirements. The standard was first issued in 2000 (effective 2001) and significantly revised in 2003 (effective 2005), with subsequent amendments tied to IFRS 16 and IFRS 15.

The primary distinction IAS 40 draws is between property held to generate rental income or capital appreciation (investment property) and property used in the ordinary course of business (owner-occupied property covered by IAS 16). This distinction matters greatly because IAS 40 permits fair value accounting with gains and losses recognised in profit or loss, a treatment not available under IAS 16.

2. Objective & Core Principle of IAS 40

The objective of IAS 40 is to prescribe the accounting treatment for investment property and the related disclosure requirements. It aims to ensure that financial statements provide relevant and faithfully representative information about an entity’s investment properties.

Investment property shall be recognised as an asset when it is probable that the future economic benefits associated with the property will flow to the entity and the cost of the property can be measured reliably.

The standard acknowledges that investment property generates cash flows largely independently from other assets, making it fundamentally different from owner-occupied property, hence the need for a separate standard and distinct measurement approaches.

3. Scope & Definitions

IAS 40 applies to the recognition, measurement, and disclosure of investment property held by all entities that prepare financial statements under IFRS.

Definition of Investment Property

Under IAS 40, investment property is land or a building or part of a building or both, held by the owner or by the lessee as a right-of-use asset to earn rentals or for capital appreciation or both, rather than for:

✓ Qualifies as Investment Property

- Land held for long-term capital appreciation

- Land held for undecided future use

- Building leased out under operating lease

- Vacant building held for future operating lease

- Property being constructed for future use as IP

- Right-of-use asset (lease) used as IP

✕ Does NOT Qualify (use IAS 16 / IFRS 5)

- Owner-occupied property (use IAS 16)

- Property for sale in the ordinary course (IAS 2)

- Property being constructed for third parties (IFRS 15)

- Forest and similar biological assets (IAS 41)

- Mineral rights and mineral reserves

- Assets held for sale (IFRS 5)

Investment Property vs Owner-Occupied Property

IAS 40.14 acknowledges that some properties have a dual nature. An entity must use judgement to determine if the property qualifies as investment property. If portions of a property can be sold or leased independently, they are accounted for separately. If they cannot be separated, the property is investment property only if the owner-occupied portion is insignificant.

Hotels operated under management contracts are typically classified as owner-occupied under IAS 16, not investment property, because the entity provides significant ancillary services. However, if a hotel is leased to a third-party operator, it may qualify as investment property.

4. Recognition Criteria Under IAS 40

Investment property is recognised as an asset when two conditions are met simultaneously:

- Probable Future Economic Benefits

It is probable that the future economic benefits associated with the investment property will flow to the entity.

- Reliable Measurement of Cost

The cost of the investment property can be measured reliably.

Initial Measurement

Investment property is initially measured at cost, including transaction costs. The cost comprises the purchase price plus any directly attributable expenditure such as:

- Professional fees (legal, survey)

- Property transfer taxes

- Borrowing costs (if IAS 23 qualifying asset)

Start-up costs, abnormal waste, and general administrative overheads are excluded from the cost of investment property. Costs incurred before the property is ready for its intended use (pre-opening costs) are expensed as incurred.

5. Measurement of Investment Property: Fair Value Model vs Cost Model

After initial recognition, IAS 40 allows an entity to choose between two accounting policies. The chosen policy must be applied consistently to all investment property.

| Feature | Fair Value Model | Cost Model |

|---|---|---|

| Measurement Basis | Fair value at each reporting date | Cost less accumulated depreciation & impairment |

| Gains/Losses | P&L Recognised in profit or loss | Indirect Via depreciation & impairment |

| Depreciation | Not required | Required (per IAS 16 principles) |

| Impairment | Not applicable (FV captures decline) | Required per IAS 36 – Impairment of Assets |

| Fair Value Disclosure | On the face of the statement | Must still disclose fair value in notes |

| Prevalence | More common in real estate entities | Less common; chosen for simplicity |

| Change of Policy | Rare Only if change results in more relevant information (IAS 8) | |

6. IAS 40 Fair Value Model Explained

Under the fair value model, an entity measures investment property at its fair value at each reporting date. Fair value is defined in IFRS 13 as the price that would be received to sell an asset in an orderly transaction between market participants at the measurement date (an exit price).

Hierarchy of Fair Value Evidence

IAS 40 encourages (but does not require) entities to determine fair value based on evidence from external, independent valuers with recognised and relevant professional qualifications and recent experience in the location and category of property. The IFRS 13 hierarchy applies:

- Level 1 – Quoted Prices

Identical assets in active markets. Rarely available for unique investment properties.

- Level 2 – Observable Inputs

Prices for similar assets; recent market transactions adjusted for differences.

- Level 3 – Unobservable Inputs

Discounted cash flow models using management assumptions about rental yields, capitalisation rates, and vacancy rates. Most investment properties fall here.

Inability to Determine Fair Value Reliably

IAS 40 presumes that fair value can always be determined reliably on a continuing basis for investment property. The standard acknowledges that in exceptional cases, and only at initial recognition an entity may conclude that it cannot determine fair value reliably. In such cases, the property is measured using the cost model until disposal, and must disclose why fair value cannot be determined.

Scenario: Entity A owns a commercial office tower in London valued at £50 million at 31 December 2024. At 31 December 2025, an independent valuer determines fair value is £54 million.

Journal Entry (Fair Value Model):

Cr Gain on Fair Value (P&L) £4,000,000

The £4m gain flows through profit or loss, not OCI. No depreciation is charged in the year.

7. IAS 40 Cost Model Explained

Under the cost model, investment property is measured at cost less accumulated depreciation and any accumulated impairment losses, essentially the same treatment as IAS 16 Property, Plant and Equipment. However, it is critically important to note that even under the cost model, an entity must disclose the fair value of its investment property in the notes to the financial statements.

Whether an entity chooses the fair value model or the cost model, IAS 40 requires fair value disclosure for all investment property. The difference is only in whether fair value changes hit the balance sheet and income statement directly.

Depreciation Under the Cost Model

Depreciation is applied following IAS 16 principles. The depreciable amount (cost less residual value) is allocated over the useful life of the asset on a systematic basis. Common approaches include:

- Straight-line method – equal annual charges over useful life (most common)

- Diminishing balance method – higher charges in early years

- Note: Land is not depreciated as it has an indefinite useful life

8. Transfers to and from Investment Property

Transfers to or from investment property classification are made when, and only when, there is a change in use evidenced by specific events. Six transfer scenarios are defined in IAS 40.57:

| # | Evidence of Change | Transfer Direction |

|---|---|---|

| 1 | Owner commences owner-occupation | IP → IAS 16 (Owner-Occupied Property) |

| 2 | Commencement of development with intent to sell | IP → IAS 2 (Inventories) |

| 3 | End of owner-occupation | IAS 16 → IP |

| 4 | Commencement of operating lease to another party | IAS 2 → IP |

| 5 | End of construction / development (fair value model) | IAS 16 (construction) → IP |

| 6 | Third-party operating lease commences | IAS 2 (developer) → IP |

Accounting for Transfer of Investment Property (Fair Value Model)

When transferring from owner-occupied property to investment property (measured at fair value), any difference between the carrying amount (IAS 16 net book value) and fair value at transfer date is treated as a revaluation under IAS 16, increases go to OCI (revaluation surplus); decreases go to P&L.

When transferring to investment property from inventories, the difference between fair value and carrying amount at transfer date is recognised in profit or loss.

9. Disposal and Derecognition of Investment Property Under IAS 40

Investment property is derecognised on disposal or when it is permanently withdrawn from use and no future economic benefits are expected from its disposal. The gain or loss arising from derecognition is the difference between:

Gain/(Loss) = Net Disposal Proceeds − Carrying Amount at Derecognition Date

Under the fair value model, since the carrying amount will already reflect fair value, the gain or loss on disposal will be relatively small (primarily reflecting transaction costs or price negotiation differences). Under the cost model, the gain or loss will reflect cumulative market appreciation not captured on the balance sheet.

IAS 40.71 requires that gains or losses arising from disposal of investment property are recognised in profit or loss in the period of derecognition (unless IFRS 16 requires otherwise for sale-and-leaseback transactions).

10. Disclosure Requirements Under IAS 40

IAS 40 has extensive disclosure requirements intended to help users of financial statements understand the nature and extent of investment property and the accounting policies applied.

General Disclosures (All Entities)

- Whether the fair value or cost model is applied

- Criteria used to distinguish investment property from owner-occupied property and property held for sale

- Methods and significant assumptions applied in determining fair value

- Extent to which fair value is based on a valuer’s assessment

- Rental income and operating expenses recognised

- Restrictions on realisability of investment property or remittance of income

- Contractual obligations to purchase, construct, develop or repair investment property

Additional Disclosures – Fair Value Model

- Reconciliation of the carrying amount at beginning and end of period (additions, disposals, fair value gains/losses, transfers, FX differences)

- When a property cannot be reliably measured at fair value, additional disclosure about the property, reason, range of estimates, and carrying amount

Additional Disclosures – Cost Model

- Depreciation methods and useful lives used

- Gross carrying amount, accumulated depreciation, and impairment at beginning and end of period

- Fair value of investment property (required even under cost model)

- Reconciliation of carrying amounts

11. Frequently Asked Questions

(Qualified) Chartered Accountant – ICAP

Master of Commerce – HEC, Pakistan

Bachelor of Accounting (Honours) – AeU, Malaysia