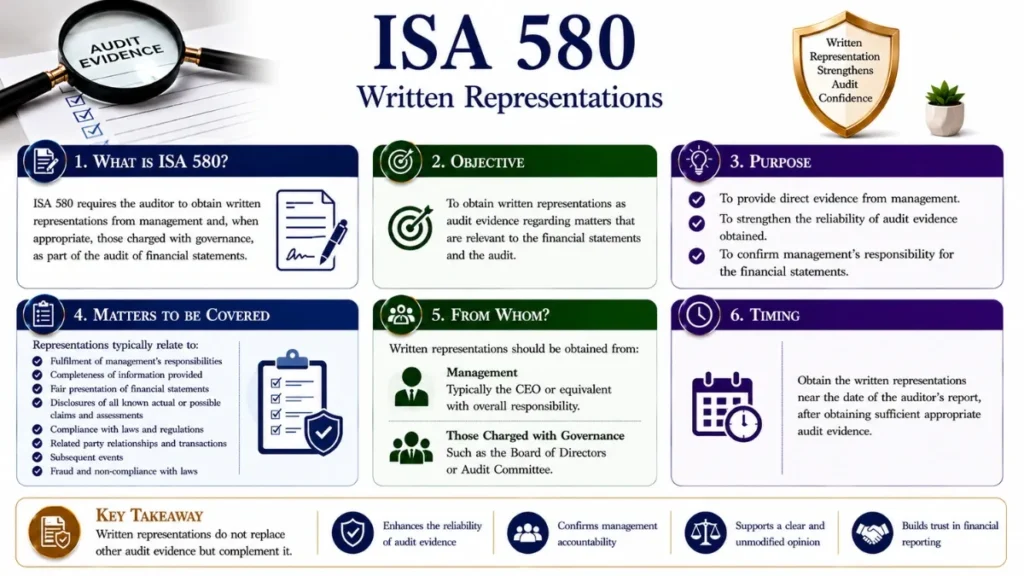

ISA 580 deals with the auditor’s responsibility to obtain written representations from management and where appropriate, those charged with governance in an ‘audit‘ of financial statements.

ISA 580 – Written Representations

A comprehensive guide to the auditor’s obligations and management’s responsibilities under ISA 580, covering the nature, form, content, and consequences of written representations in audit engagements.

What Is ISA 580?

ISA 580 – Written Representations, is one of the International Standards on Auditing issued by the International Auditing and Assurance Standards Board (IAASB). It establishes the auditor’s responsibilities with respect to written representations obtained from management and, where appropriate, those charged with governance, as part of a financial statement audit.

The standard recognises that management bears primary responsibility for the preparation and fair presentation of financial statements and for providing the auditor with complete and accurate information. Written representations serve as a formal, documented acknowledgement of this responsibility and as audit evidence, albeit a particular kind that must be evaluated carefully.

The auditor shall request management to provide written representations that it has fulfilled its responsibility for the preparation and fair presentation of the financial statements in accordance with the applicable financial reporting framework.

ISA 580, paragraph 10

ISA 580 is part of the broader ISA framework governing audit evidence and applies to all audits of financial statements conducted in accordance with International Standards on Auditing. It works in conjunction with ISA 200 (Overall Objectives of the Independent Auditor), ISA 500 (Audit Evidence), and ISA 260 (Communication with Those Charged with Governance).

Standard Issued By

International Auditing and Assurance Standards Board (IAASB), a standard-setting body under IFAC.

Primary Purpose

Obtain formal acknowledgement from management confirming key assertions and completeness of information provided.

Applicability

All audits of financial statements regardless of size, entity type, or complexity of the engagement.

Objectives of ISA 580

ISA 580 establishes two complementary objectives for the auditor in relation to written representations:

To obtain written representations from management (and, where appropriate, those charged with governance) that management believes it has fulfilled its responsibility for preparing the financial statements and for the completeness of information provided to the auditor.

To support other audit evidence relevant to the financial statements or specific assertions within those statements, where the auditor has determined that written representations are necessary or required by other ISAs.

These objectives recognise a dual function: written representations are both a confirmation of management’s acknowledged responsibilities and a supplementary form of evidence that corroborates information obtained from other procedures. Crucially, they are necessary but not sufficient, they must always be considered alongside other audit evidence.

The objectives under ISA 580 do not extend to requiring the auditor to seek representations as a substitute for other, more persuasive evidence that can reasonably be expected to exist. Written representations supplement the audit record, they do not replace substantive procedures.

Key Definitions & Terminology

ISA 580 uses a number of technical terms that must be understood in their precise context. The following definitions are drawn from the standard itself and its application guidance:

Management Responsibilities Under ISA 580

Management is responsible for the preparation and fair presentation of the financial statements and for the adequacy of internal controls. Written representations formalise management’s acknowledgement of these responsibilities.

The Premise Underlying an Audit

ISA 580 is closely linked to the concept of the “premise” established in ISA 210 (Agreeing the Terms of Audit Engagements). That premise requires management to acknowledge and understand that it:

- Is responsible for the preparation and fair presentation of financial statements in accordance with the applicable financial reporting framework;

- Is responsible for such internal controls as management determines is necessary to enable the preparation of financial statements that are free from material misstatement; and

- Has provided the auditor with all information relevant to the preparation and presentation of the financial statements, as well as any additional information requested, and unrestricted access to persons within the entity from whom the auditor determines it necessary to obtain audit evidence.

Written representations under ISA 580 serve as the formal record of management’s acknowledgement of these obligations at the time the audit concludes.

Who Should Sign the Representation Letter?

The representation letter should be signed by management members with the appropriate authority and knowledge. The standard indicates that, ordinarily, this means the Chief Executive Officer and the Chief Financial Officer (or their equivalents), because these individuals are best placed to confirm the completeness and accuracy of information provided to the auditor.

In some entities, those charged with governance such as an audit committee or non-executive directors may also be asked to provide written representations, particularly on matters such as fraud, related-party transactions, or governance arrangements, where they have specific oversight responsibilities.

Auditor Responsibilities Under ISA 580

ISA 580 imposes several specific requirements on the auditor. These requirements are mandatory in all audits conducted under International Standards on Auditing.

Mandatory Written Representations – Always Required

The auditor shall request management to provide written representations regarding:

- Fulfilment of its responsibility for the preparation and fair presentation of the financial statements in accordance with the applicable financial reporting framework;

- Confirmation that management has provided the auditor with all relevant information and access as agreed in the terms of the audit engagement;

- Confirmation that all transactions have been recorded and are reflected in the financial statements;

- Management’s belief that the effects of uncorrected misstatements (if any) are immaterial, individually and in aggregate, to the financial statements as a whole.

Other Written Representations Required by ISAs

Numerous other ISAs require the auditor to obtain written representations on specific matters. These include, but are not limited to:

| ISA Reference | Topic | Nature of Representation Required |

|---|---|---|

| ISA 240 | Fraud | Management has disclosed all information relevant to fraud or suspected fraud; management has no knowledge of fraud. |

| ISA 250 | Laws & Regulations | Management has disclosed all known instances of non-compliance or suspected non-compliance with laws and regulations. |

| ISA 450 | Uncorrected Misstatements | Management believes the effects of uncorrected misstatements are immaterial, individually and in aggregate. |

| ISA 501 | Inventory & Litigation | Completeness of all claims and litigation that may affect the financial statements has been disclosed. |

| ISA 540 | Accounting Estimates | Reasonableness of significant assumptions used in making accounting estimates. |

| ISA 550 | Related Parties | All related-party relationships and transactions have been disclosed and properly accounted for. |

| ISA 560 | Subsequent Events | All events occurring subsequent to the balance sheet date have been adjusted for or disclosed as required. |

| ISA 570 | Going Concern | Management’s plans for future actions relevant to going concern have been disclosed. |

Form and Content of Representation Letters

ISA 580 contains specific requirements regarding the form, dating, and content of written representations that the auditor must observe carefully.

Form

Written representations shall be in the form of a representation letter addressed to the auditor. Where law or regulation requires management to make written public statements about its responsibilities for example, in a directors’ report and the auditor determines that such statements are equivalent to written representations, the auditor need not request a separate letter in respect of those matters, but must assess whether those statements satisfy the requirements of ISA 580.

Date

The representation letter must be dated as near as practicable to, but not after, the date of the auditor’s report. This requirement is critical: the representations must cover the entire period of the audit and must reflect management’s knowledge at the time the auditor is about to issue the report.

Representations dated after the auditor’s report do not comply with ISA 580. The standard explicitly requires the representation letter to be dated no later than the audit report date. A representation letter dated earlier than the report date introduces a gap that the auditor must consider carefully for example, whether subsequent events representations remain valid.

Period Covered

Written representations shall cover all financial statements and periods referred to in the auditor’s report. If comparative financial statements are presented, representations should address those comparative periods as well.

Content Requirements

The content of the representation letter must at minimum address the mandatory representations set out in paragraphs 10 and 11 of ISA 580, plus any other representations required by specific ISAs or determined necessary by the auditor given the circumstances of the engagement.

Well-drafted representation letters are entity-specific and engagement-specific. Auditors are encouraged to tailor the letter to the significant matters arising from the audit rather than relying on generic templates that may fail to capture the particular circumstances of the entity.

Reliability of Written Representations as Audit Evidence

ISA 580 addresses candidly the limitations of written representations as audit evidence. Understanding these limitations is fundamental to their correct use within the audit.

Written Representations Are Necessary But Not Sufficient

Although written representations provide necessary audit evidence, they do not provide sufficient appropriate audit evidence on their own about any of the matters with which they deal. The auditor cannot substitute a written representation for more reliable audit evidence where such evidence can reasonably be expected to exist.

The inherent reliability of written representations is limited by the fact that they are internal to the entity, they are provided by management rather than obtained independently. The hierarchy of audit evidence under ISA 500 places internally-generated evidence below externally-corroborated or independently-obtained evidence in terms of reliability.

Evaluating Written Representations

The auditor is required to consider whether representations are consistent with other audit evidence obtained. If a written representation is inconsistent with other audit evidence, the auditor must investigate the inconsistency and consider its implications for the reliability of both the representation and other audit evidence.

Consistent Representations

Where representations are consistent with other evidence obtained, they provide useful corroboration and fulfil a necessary documentary role in the audit file.

Inconsistent Representations

Inconsistency between a written representation and other evidence may indicate management bias, error, or a misunderstanding requiring further investigation and reconsideration of assessed risks.

Unverifiable Representations

Representations on matters that cannot be corroborated such as management’s intentions, require the auditor to evaluate consistency with the overall audit picture and known facts.

Auditor Actions When Doubts Arise About Written Representations

ISA 580 requires the auditor to take specific action if there is concern about the reliability of written representations received from management. Such doubt may arise from various circumstances discovered during the audit.

Circumstances Giving Rise to Doubt

- Evidence obtained during the audit contradicts a representation made by management;

- The auditor has reason to believe management lacks the requisite knowledge to make an informed representation on a particular matter;

- Representations are inconsistent with the auditor’s understanding of the entity and its environment;

- Information comes to light suggesting that management is not forthcoming in providing information requested by the auditor;

- Management provides representations that are qualified or conditional in ways not anticipated.

Required Response

Where doubt arises about any written representation, the auditor shall:

Raise concerns directly with management to seek clarification and resolve the apparent inconsistency or concern.

Consider whether the doubt about the representation affects the auditor’s assessment of management’s integrity and the reliability of representations obtained throughout the audit.

Assess whether unreliable representations require additional audit procedures to obtain sufficient appropriate evidence on the matters in question.

Where doubt cannot be resolved, assess whether a modification to the audit opinion is necessary under ISA 705 (Modifications to the Opinion in the Independent Auditor’s Report).

Consequences of Refusal to Provide Written Representations Under ISA 580

ISA 580 treats a refusal by management to provide required written representations as a serious matter with direct consequences for the auditor’s report.

Refusal as a Scope Limitation

If management does not provide one or more of the required written representations, the auditor shall:

- Discuss the matter with management and, where appropriate, those charged with governance;

- Re-evaluate the integrity of management and evaluate the effect that this may have on the reliability of representations (oral or written) and audit evidence in general;

- Determine the impact on the audit opinion, a refusal to provide mandatory representations constitutes a limitation on the scope of the audit;

- Either issue a qualified opinion or disclaim an opinion on the financial statements, as appropriate;

- Withdraw from the engagement where withdrawal is possible under applicable law or regulation, and communicate the reasons to those charged with governance.

ISA 580 is explicit: if management refuses to provide the representations required by paragraphs 10 and 11 (the mandatory general representations), the auditor shall disclaim an opinion on the financial statements, not merely qualify it. This reflects the fundamental nature of those representations and without them, the auditor cannot form an opinion at all.

If management does not provide the written representations required by paragraphs 10 and 11, the auditor shall disclaim an opinion on the financial statements in accordance with ISA 705.

ISA 580, paragraph 21

Practical Application of ISA 580 – Specimen Written Representation Letter

The following is a simplified specimen of the structure and content of a written representation letter. This is illustrative only and must be adapted to the specific circumstances of each engagement. Auditors should refer to Appendix 2 of ISA 580 for illustrative examples provided by the IAASB.

[Letterhead of Entity]

[Date – same as or before date of auditor’s report]

To: [Name of Audit Firm]

Dear [Audit Partner],

This letter of representations is provided in connection with your audit of the financial statements of [Entity Name] for the year ended [Date], for the purpose of expressing an opinion on whether the financial statements give a true and fair view in accordance with [Applicable Framework].

We confirm, to the best of our knowledge and belief, and having made such enquiries as we considered necessary for the purpose of appropriately informing ourselves:

Financial Statements

- We have fulfilled our responsibilities for the preparation and fair presentation of the financial statements in accordance with [Applicable Framework].

- All transactions have been recorded and are reflected in the financial statements.

- We have provided you with all information and access as agreed in the terms of the audit engagement.

Completeness of Information

- We have disclosed to you all known instances of non-compliance or suspected non-compliance with laws and regulations whose effects should be considered when preparing the financial statements.

- We have disclosed to you all information relevant to fraud or suspected fraud affecting the entity of which we are aware.

- All related-party relationships and transactions have been appropriately accounted for and disclosed.

Uncorrected Misstatements

- We believe that the effects of the uncorrected misstatements summarised in the attached schedule are immaterial, both individually and in the aggregate, to the financial statements taken as a whole.

Subsequent Events

- All events subsequent to [balance sheet date] that require adjustment to, or disclosure in, the financial statements have been adjusted or disclosed.

Yours faithfully,

___________________________ ___________________________

[Chief Executive Officer] [Chief Financial Officer]

[Entity Name] [Entity Name]

ISA 580 in the Context of Related Auditing Standards

ISA 580 does not operate in isolation. Understanding its relationship with other ISAs helps auditors apply it correctly and appreciate how the written representations obtained contribute to the overall audit conclusion.

| Standard | Primary Focus | Relationship to ISA 580 |

|---|---|---|

| ISA 200 | Overall Objectives of the Auditor | Establishes the premise that management is responsible for the financial statements, the foundation on which ISA 580 representations rest. |

| ISA 210 | Agreeing the Terms of Audit Engagements | Management’s acknowledgement in the engagement letter of its responsibilities is reinforced through written representations at the end of the audit. |

| ISA 500 | Audit Evidence | Classifies written representations as audit evidence and sets the overarching sufficiency and appropriateness criteria that ISA 580 representations must meet. |

| ISA 540 | Accounting Estimates | Requires specific representations on the reasonableness of significant assumptions underpinning accounting estimates. |

| ISA 570 | Going Concern | Requires representations on the completeness of management’s plans regarding going concern where relevant. |

| ISA 705 | Modifications to the Opinion | Governs the type of modification required (qualified, adverse, or disclaimer) when ISA 580 representations are not provided or are unreliable. |

Frequently Asked Questions

(Qualified) Chartered Accountant – ICAP

Master of Commerce – HEC, Pakistan

Bachelor of Accounting (Honours) – AeU, Malaysia