Reversal of impairment loss is increasing the value of a previously impaired asset when there is a change in circumstances indicating that the impairment loss is no longer necessary.

Reversal of Impairment Loss

When assets recover value; understanding the rules, ceilings, restrictions, and accounting treatment under International Standards.

What Is Reversal of Impairment Loss?

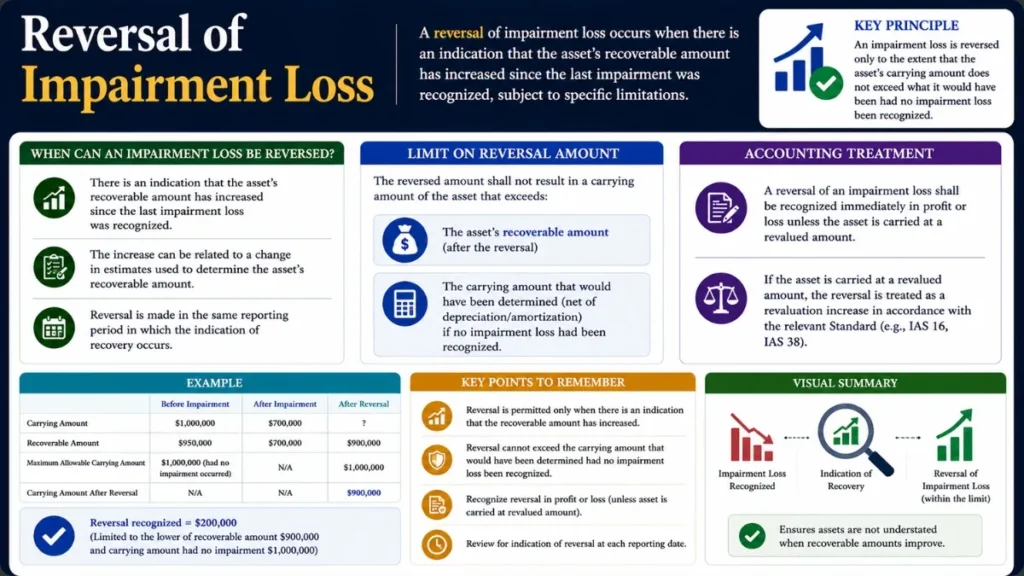

A reversal of impairment loss occurs when there is an increase in the recoverable amount of an asset previously written down, allowing the carrying amount to be increased back up, subject to a defined ceiling.

– IAS 36: Impairment of AssetsUnder IAS 36 – Impairment of Assets issued by the International Accounting Standards Board (IASB), entities are required not only to recognise impairment losses when an asset’s carrying amount exceeds its recoverable amount, but also to reassess at each reporting date whether conditions that led to impairment have changed. If circumstances improve, the reversal of a previously recognised impairment loss may be required.

When Can an Impairment Loss Be Reversed?

IAS 36 paragraph 110 requires that an entity assess at the end of each reporting period whether there is any indication that a previously recognised impairment loss may no longer exist or may have decreased. Indicators are grouped into external and internal sources.

External Indicators of Potential Reversal

Rise in Market Value

The asset’s market value has increased significantly beyond normal expectations during the period.

Favourable Environment

Significant positive changes in technology, market, economic, or legal environment where the asset operates.

Interest Rate Decline

Decreases in market interest rates that increase the value in use via a lower discount rate.

External Market Data

Observable market data indicates an increase in the asset’s recoverable amount since last impairment.

Internal Indicators of Potential Reversal

Operational Improvement

Significant positive changes in how the asset is used or expected to be used in the business.

Better-than-Expected Cash Flows

Actual economic performance of the asset is significantly better than originally budgeted or forecasted.

Capital Expenditure

During the period, the entity spent cash to enhance or restore the asset’s standard of performance.

Revised Internal Reports

Internal reporting indicates the asset’s economic performance is better than budgeted.

The Reversal Ceiling under IAS 36 – How Much Can Be Reversed?

A reversal of impairment loss is not unlimited. IAS 36 paragraph 117 sets a clear ceiling: the carrying amount after reversal cannot exceed what the carrying amount would have been had no impairment loss ever been recognised, taking into account normal depreciation or amortisation.

= Carrying Amount Had No Impairment Been Recognised

(i.e., Cost – Accumulated Depreciation based on original schedule)

Reversal Amount = min(Recoverable Amount, Ceiling) – Current Carrying Amount

This ceiling prevents entities from reversing more than the original impairment and effectively bans the recognition of internally generated goodwill through the back door of impairment reversal.

Goodwill Impairment Reversal Rules

This is one of the most important and often-tested rules under IAS 36. Even if all the conditions for reversal are met and the recoverable amount of the cash-generating unit containing goodwill has increased, the goodwill impairment cannot be reversed.

Why Is Goodwill Reversal Prohibited?

The rationale lies in the nature of goodwill. Any increase in the recoverable amount of a CGU after goodwill impairment is attributable to either:

- An increase in the value of the purchased goodwill itself – which cannot be verified objectively, or

- An increase in the value of internally generated goodwill – which IAS 38 explicitly prohibits from recognition.

Since neither scenario allows recognition, IAS 36 takes the conservative approach: once goodwill is impaired, it stays impaired.

How to Calculate Reversal of Impairment Loss (Step-by-Step Reversal Process)

Identify Reversal Indicators

At each reporting date, assess internal and external sources for indicators that a prior impairment may have partially or fully reversed.

Estimate the Recoverable Amount

Calculate the recoverable amount as the higher of (a) fair value less costs of disposal and (b) value in use.

Compare with Carrying Amount

If recoverable amount exceeds current carrying amount, a reversal is potentially required.

Apply the Ceiling Test

Calculate the carrying amount that would have existed had no impairment been recognised, accounting for normal depreciation. This is the maximum post-reversal carrying amount.

Determine the Reversal Amount

Reversal = min(Recoverable Amount, Ceiling) minus current Carrying Amount.

Record the Journal Entry

Debit the asset and credit profit or loss (or OCI if originally charged to OCI under a revaluation model).

Adjust Depreciation Prospectively

Recalculate and update the annual depreciation charge based on the new higher carrying amount over the remaining useful life.

Journal Entries for Reversal of Impairment Loss

Standard Treatment (Cost Model)

When an asset is carried under the cost model (IAS 16), the reversal is taken to profit or loss:

| Account | Dr / Cr | Amount |

|---|---|---|

| Asset Account (e.g., Property, Plant & Equipment) | DR | XXX |

| Reversal of Impairment Loss (Profit or Loss) | CR | XXX |

Revaluation Model Treatment

When an asset is carried at revalued amount under IAS 16 and the original impairment was charged to other comprehensive income (OCI), the reversal is credited to OCI (revaluation surplus), not profit or loss:

| Account | Dr / Cr | Amount |

|---|---|---|

| Asset Account | DR | XXX |

| Revaluation Surplus – OCI | CR | XXX |

Reversal of Impairment Loss Example

Manufacturing Machine – Reversal After 2 Years

Background: Apex Ltd. owns a machine purchased on 1 January 2020 for $500,000. Useful life: 10 years. Straight-line depreciation with zero residual value.

Impairment (31 Dec 2021): At the end of year 2, the recoverable amount was estimated at $280,000. Carrying amount was $400,000. Impairment loss of $120,000 was recognised.

Post-Impairment Depreciation: Remaining life = 8 years. New annual depreciation = $280,000 ÷ 8 = $35,000/year.

Reversal (31 Dec 2023): Two years later, recoverable amount rises to $260,000. Current carrying amount = $280,000 − ($35,000 × 2) = $210,000.

Step 1 – Calculate the Ceiling

Depreciation 2020-2023 (4 yrs): $500,000 ÷ 10 × 4 = $200,000

Hypothetical CA (no impairment): $500,000 − $200,000 = $300,000

Step 2 – Reversal Amount

Ceiling: $300,000

Lower of two: $260,000

Current CA: $210,000

Reversal = $260,000 − $210,000 = $50,000

Step 3 – Journal Entry

| Account | Dr / Cr | Amount ($) |

|---|---|---|

| Machine (PPE) | DR | 50,000 |

| Reversal of Impairment Loss (P&L) | CR | 50,000 |

Step 4 – New Depreciation Going Forward

Remaining useful life: 6 years (10 − 4)

New Annual Depreciation = $260,000 ÷ 6 = $43,333/year

Cash-Generating Units (CGU) Reversal of Impairment Loss

When impairment was originally allocated across a CGU and its assets, reversal follows a specific allocation order. IAS 36 paragraph 122 requires that the reversal be allocated to the assets of the unit pro rata on the basis of their carrying amounts.

Allocation Rules for CGU Reversal

- Allocate the reversal to each asset in the CGU (excluding goodwill) on a pro-rata basis.

- The reversal for each asset is capped at its own ceiling (i.e., what its carrying amount would have been without the impairment).

- If a ceiling applies to one asset, the excess is reallocated to other assets.

- Goodwill impairment within the CGU is never reversed.

Disclosure Requirements for Impairment Reversal

IAS 36 paragraphs 126–133 require extensive disclosures whenever impairment losses or reversals are material. Entities must disclose for each class of assets:

- The amount of impairment losses reversed in the period and recognised in profit or loss.

- The amount reversed in OCI (other comprehensive income).

- The line items in the statement of profit or loss in which these reversals are included.

- The events and circumstances that led to the reversal.

- The recoverable amount, and whether it is fair value less costs of disposal or value in use.

- If recoverable amount is fair value: the valuation technique and key assumptions used.

- If recoverable amount is value in use: the discount rate(s) applied in the current and prior estimate.

IAS 36 (IFRS) vs US GAAP Impairment Reversal

| Aspect | IAS 36 (IFRS) | US GAAP (ASC 360 / 350) |

|---|---|---|

| Impairment Reversal (Non-Goodwill) | ✓ Permitted & Required | ✕ Not Permitted |

| Goodwill Reversal | ✕ Prohibited | ✕ Prohibited |

| Test Approach | One-step: Recoverable Amount vs CA | Two-step (or simplified one-step) |

| Basis of Recoverable Amount | Higher of FVLCOD and VIU | Fair Value only (no VIU concept) |

| Ceiling on Reversal | ✓ Yes – hypothetical CA cap | N/A – reversals not allowed |

| Annual Goodwill Test Required | ✓ Annually (CGU level) | ✓ Annually (reporting unit) |

Frequently Asked Questions

No. IAS 36 paragraph 124 strictly prohibits the reversal of goodwill impairment. Any subsequent increase in recoverable amount of a CGU containing goodwill is treated as internally generated goodwill, which cannot be recognised under IAS 38.

The carrying amount after reversal cannot exceed what the carrying amount would have been (net of depreciation/amortisation) had no impairment loss been recognised in prior periods. This hypothetical figure acts as the ceiling. The reversal is the lower of the recoverable amount and this ceiling, less the current carrying amount.

It is mandatory. IAS 36 requires that if there is an indication that the recoverable amount has increased, the entity must estimate the recoverable amount. If it exceeds the carrying amount (subject to the ceiling), the reversal must be recognised. Entities cannot choose to suppress a reversal to be conservative.

For assets under the cost model, the reversal is recognised in profit or loss. For assets under the revaluation model where the original impairment was charged against OCI (revaluation surplus), the reversal is credited to OCI. If the original impairment exceeded the revaluation surplus, the excess reversal goes to profit or loss.

At the end of every reporting period. IAS 36 paragraph 110 requires that entities assess at each balance sheet date whether there is any indication that a previously recognised impairment loss may have decreased or no longer exist. This is an ongoing obligation, not a one-time review.

No. Under US GAAP (ASC 360 for long-lived assets, ASC 350 for goodwill and intangibles), once an impairment loss is recognised, it establishes a new cost basis. Subsequent recovery of value cannot be recognised. This is a significant difference from IFRS under IAS 36.

Quick Reference & Key Takeaways

- Reversal is mandatory if indicators exist, not optional.

- Goodwill impairment reversal is strictly prohibited under IAS 36.

- The ceiling caps reversal at the hypothetical carrying amount.

- Depreciation must be updated prospectively after reversal.

- CGU reversals are allocated pro rata (excluding goodwill).

- US GAAP prohibits all asset impairment reversals.

(Qualified) Chartered Accountant – ICAP

Master of Commerce – HEC, Pakistan

Bachelor of Accounting (Honours) – AeU, Malaysia