Accounting entries for acquisition of subsidiary involve recording the purchase consideration, identifiable assets and liabilities, and any resulting goodwill or gain on bargain purchase.

Accounting Entries for Acquisition of Subsidiary

A step-by-step guide to journal entries, goodwill calculation, consolidation adjustments, and disclosure requirements when a parent company acquires a controlling interest in another entity.

What Is a Subsidiary Acquisition?

A subsidiary acquisition occurs when one entity (the parent or acquirer) obtains control over another entity (the subsidiary or acquiree), typically by purchasing more than 50% of its voting equity, or by otherwise gaining the power to direct its relevant activities. Upon acquisition, the parent must prepare consolidated financial statements that combine the financial results of both entities.

Control under IFRS 10: An investor controls an investee when it has power over the investee, exposure or rights to variable returns from its involvement, and the ability to use its power to affect those returns.

The accounting treatment for subsidiary acquisitions is governed by IASB issued IFRS 3 Business Combinations (internationally) and ASC 805 (under US GAAP). Both frameworks mandate the acquisition method of accounting, which replaced the pooling-of-interests method.

Accounting entries arise at two distinct levels: (1) in the parent’s individual (separate) financial statements, where the investment is recorded at cost; and (2) in the consolidated financial statements, where the assets, liabilities, income, and expenses of both entities are combined and intercompany items eliminated.

Acquisition Method under IFRS 3

Under the acquisition method, the acquirer must complete four key steps on the acquisition date, the date on which it obtains control:

- Identify the acquirer

Determine which entity is the acquirer, typically the one that transfers cash or other assets, incurs liabilities, or issues equity as consideration.

- Determine the acquisition date

Usually the date the parent legally transfers the consideration and obtains control, this is when accounting entries are recognised.

- Recognise and measure identifiable assets and liabilities

All of the subsidiary’s identifiable assets, liabilities, and contingent liabilities must be recognised at their fair value on the acquisition date including intangible assets not previously recognised by the acquiree.

- Recognise goodwill or bargain purchase gain

The difference between the consideration paid (plus NCI fair value) and the net fair value of identifiable assets and liabilities is recognised as goodwill (or as a gain if negative).

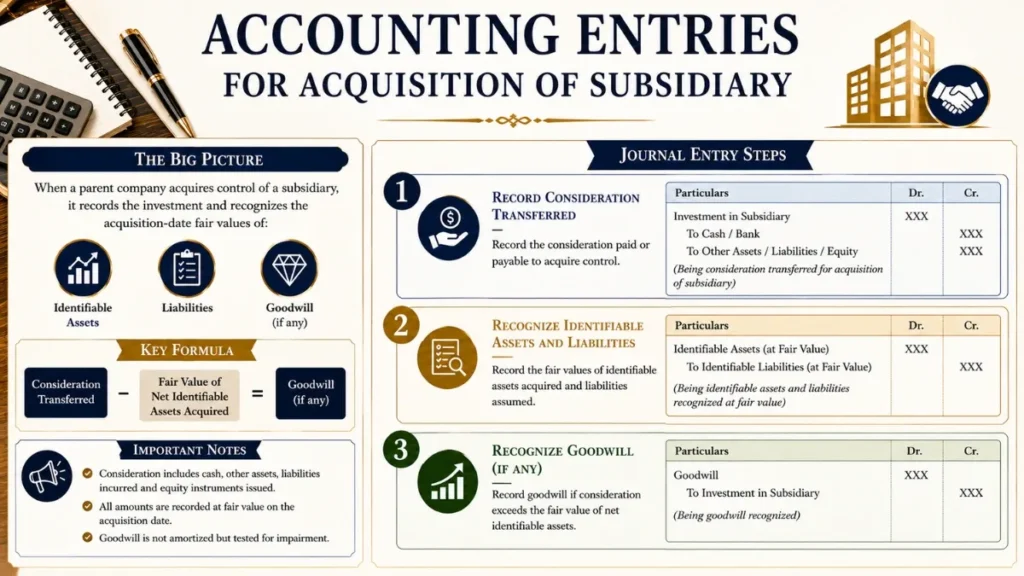

Initial Accounting Entries for Acquisition of Subsidiary

3.1 In the Parent’s Separate Financial Statements

In the parent’s own books, the acquisition is recorded as a simple investment at cost. The parent does not consolidate in its own statements, that happens at the group level.

| Account | Dr ($) | Cr ($) | Narration |

|---|---|---|---|

| Investment in Subsidiary | XXX | — | Cost of acquisition |

| Cash / Bank | — | XXX | Cash consideration paid |

| Being investment in subsidiary recorded at cost on acquisition date. | |||

3.2 Acquisition via Share Exchange

If the parent issues its own shares as consideration (a share-for-share exchange), no cash flows but the parent still records the investment at the fair value of the shares issued:

| Account | Dr ($) | Cr ($) | Narration |

|---|---|---|---|

| Investment in Subsidiary | XXX | — | FV of shares issued |

| Share Capital | — | XXX | Nominal value of shares |

| Share Premium | — | XXX | Excess over nominal value |

| Being investment in subsidiary recorded at fair value of equity instruments issued. | |||

3.3 Acquisition Costs

| Account | Dr ($) | Cr ($) | Narration |

|---|---|---|---|

| Acquisition Costs Expense (P&L) | XXX | — | Legal, advisory fees etc. |

| Cash / Accounts Payable | — | XXX | Amount paid / accrued |

| Being direct acquisition costs expensed as incurred per IFRS 3 para 53 / ASC 805-10-25-23. | |||

Goodwill Calculation & Journal Entry

Goodwill arises when the total consideration paid for a subsidiary exceeds the fair value of its net identifiable assets and liabilities. It represents the premium paid for synergies, brand value, workforce, market position, and other unrecognised intangibles.

+ FV of Non-Controlling Interest (NCI)

+ FV of Previously Held Equity Interest

− FV of Net Identifiable Assets & Liabilities

| Account | Dr ($) | Cr ($) | Narration |

|---|---|---|---|

| Net Assets of Subsidiary (at FV) | XXX | — | All identifiable assets/liabilities at FV |

| Goodwill | XXX | — | Excess cost over net assets |

| Investment in Subsidiary | — | XXX | Cost in parent’s books (eliminated) |

| Non-Controlling Interest (NCI) | — | XXX | NCI at fair value |

| Pre-acquisition Reserves of Subsidiary | — | XXX | Subsidiary’s equity eliminated |

| Being elimination of parent’s investment against subsidiary’s equity and recognition of goodwill at acquisition date. | |||

Subsequent Measurement of Goodwill

Once recognised, goodwill is never amortised under IFRS or US GAAP (for public entities). Instead, it must be tested for impairment at least annually. If the recoverable amount of the cash-generating unit (CGU) to which goodwill is allocated falls below its carrying amount, an impairment loss is recognised immediately:

| Account | Dr ($) | Cr ($) | Narration |

|---|---|---|---|

| Impairment Loss – Goodwill (P&L) | XXX | — | Loss to profit or loss |

| Goodwill (Balance Sheet) | — | XXX | Reduction in carrying amount |

| Being impairment loss on goodwill recognised per IAS 36. Once impaired, goodwill cannot be reversed. | |||

Non-Controlling Interest (NCI) Accounting with Entries

When the parent acquires less than 100% of the subsidiary, the remaining equity held by outside shareholders is the Non-Controlling Interest (NCI). NCI is presented within equity in the consolidated statement of financial position, separately from the parent’s equity.

NCI Measurement Methods

| Method | Measurement Basis | Goodwill Attributed To | Permitted Under |

|---|---|---|---|

| Full Goodwill | Fair value of NCI’s equity (e.g. market price × NCI shares) | Both parent and NCI | IFRS 3 & ASC 805 |

| Proportionate (Partial) Goodwill | NCI’s proportionate share of net identifiable assets | Parent’s share only | IFRS 3 (not ASC 805) |

Post-Acquisition NCI Share of Profit

| Account | Dr ($) | Cr ($) | Narration |

|---|---|---|---|

| Profit Attributable to Parent (P&L) | XXX | — | Total group profit reclassified |

| Profit Attributable to NCI (P&L) | — | XXX | NCI % × subsidiary’s profit |

| NCI – Equity (Balance Sheet) | — | XXX | NCI’s share of retained earnings increases |

Consolidation Elimination Entries

When preparing consolidated financial statements, the group must eliminate all transactions and balances between the parent and its subsidiaries. These are purely consolidation adjustments, they do not alter the individual entity’s books.

6.1 Elimination of Intercompany Balances

| Account | Dr ($) | Cr ($) |

|---|---|---|

| Intercompany Payable (Subsidiary’s books) | XXX | — |

| Intercompany Receivable (Parent’s books) | — | XXX |

| Being elimination of intercompany balances on consolidation. | ||

6.2 Elimination of Intercompany Sales

| Account | Dr ($) | Cr ($) |

|---|---|---|

| Intercompany Sales Revenue | XXX | — |

| Intercompany Cost of Sales | — | XXX |

6.3 Unrealised Profit in Inventory

| Account | Dr ($) | Cr ($) | Narration |

|---|---|---|---|

| Cost of Sales / Retained Earnings | XXX | — | Unrealised profit removed |

| Inventories | — | XXX | Inventory reduced to cost to group |

| Being elimination of profit on intercompany inventory sales not yet sold to third parties. If subsidiary sold to parent, NCI share is also adjusted. | |||

Acquisition of Subsidiary Illustrative Example

Parent Co. Acquires 80% of Sub Co. for $4,800,000

On 1 January 2026, Parent Co. acquired 80% of the ordinary shares of Sub Co. for cash of $4,800,000. At the acquisition date, the following information is available:

Step 1 – Goodwill Calculation

| Item | $ |

|---|---|

| Consideration transferred | 4,800,000 |

| NCI at proportionate share (20% × $4,800,000) | 960,000 |

| Total (A) | 5,760,000 |

| FV of net identifiable assets (B) | (4,800,000) |

| Goodwill (A − B) | 960,000 |

Step 2 – Journal Entries in Parent’s Separate Books

| Account | Dr ($) | Cr ($) |

|---|---|---|

| Investment in Sub Co. | 4,800,000 | — |

| Cash | — | 4,800,000 |

| Being 80% investment in Sub Co. at cost. | ||

Step 3 – Consolidation Adjustments

| Account | Dr ($) | Cr ($) |

|---|---|---|

| Intangible Asset – Brand Name | 300,000 | — |

| Pre-Acquisition Retained Earnings (Sub Co.) | — | 300,000 |

| Being uplift of Sub Co.’s brand to fair value on consolidation. | ||

| Account | Dr ($) | Cr ($) |

|---|---|---|

| Share Capital (Sub Co.) | 1,000,000 | — |

| Retained Earnings – Pre-acquisition (Sub Co.) | 3,800,000 | — |

| Brand Name (FV uplift already booked) | — | — |

| Goodwill | 960,000 | — |

| Investment in Sub Co. | — | 4,800,000 |

| Non-Controlling Interest (NCI) | — | 960,000 |

| Being elimination of investment and subsidiary equity; recognition of goodwill $960,000 and NCI $960,000 on consolidation. | ||

Bargain Purchase Gain Accounting (Negative Goodwill)

A bargain purchase arises when the fair value of the net identifiable assets acquired exceeds the total consideration transferred. This results in a gain on bargain purchase, which must be recognised immediately in profit or loss.

| Account | Dr ($) | Cr ($) | Narration |

|---|---|---|---|

| Net Identifiable Assets (at FV) | XXX | — | All assets minus liabilities at FV |

| Consideration Transferred | — | XXX | Cash / shares / deferred |

| NCI | — | XXX | NCI at measurement election |

| Gain on Bargain Purchase (P&L) | — | XXX | Excess – recognised in profit or loss |

| Being recognition of gain on bargain purchase per IFRS 3 para 34 after reassessment of all identified assets and liabilities. | |||

Post-Acquisition Consolidation Entries

9.1 Dividend Received from Subsidiary

In the parent’s separate financial statements, dividends received from the subsidiary are recognised as income:

| Account | Dr ($) | Cr ($) |

|---|---|---|

| Cash / Dividend Receivable | XXX | — |

| Dividend Income (P&L) | — | XXX |

| In consolidation, intercompany dividends are eliminated entirely. | ||

9.2 Fair Value Adjustments – Depreciation

Where fair value adjustments were made to the subsidiary’s depreciable assets, additional depreciation must be charged in the consolidated financial statements each year on the uplifted amount:

| Account | Dr ($) | Cr ($) |

|---|---|---|

| Depreciation Expense (P&L) | XXX | — |

| Accumulated Depreciation | — | XXX |

| FV uplift ÷ remaining useful life = annual additional depreciation charge. | ||

IFRS vs US GAAP Acquisition Accounting

| Topic | IFRS 3 | US GAAP (ASC 805) |

|---|---|---|

| NCI Measurement | Full goodwill or proportionate share (policy choice) | Full goodwill method only |

| Goodwill Amortisation | No amortisation; annual impairment test (IAS 36) | No amortisation for public entities; private companies may elect amortisation |

| Goodwill Impairment Reversal | Not permitted | Not permitted |

| In-process R&D | Capitalised as an intangible asset at FV | Capitalised as an intangible asset at FV |

| Contingent Consideration | Remeasured at FV through P&L post-acquisition | Remeasured at FV; equity instruments not remeasured |

| Step Acquisitions | Previously held interest remeasured to FV; gain/loss in P&L | Same as IFRS |

| Acquisition Costs | Expensed as incurred | Expensed as incurred |

| Bargain Purchase Gain | Recognised in P&L after reassessment | Recognised in P&L after reassessment |

Disclosure Requirements under IFRS 3

IFRS 3 (paras 59–63) and ASC 805 require extensive disclosures in the notes to the financial statements for the reporting period in which the acquisition occurs. The objective is to enable users to evaluate the nature and financial effect of the business combination.

Key Disclosures Include:

- Name and description of the acquiree

- Acquisition date and percentage of voting equity acquired

- Primary reasons for the business combination and description of how control was obtained

- Qualitative description of the factors that make up the goodwill recognised

- Fair values of each major class of consideration transferred (cash, equity, contingent)

- Amounts recognised at acquisition for each major class of assets and liabilities

- Details of contingent consideration arrangements and indemnification assets

- Revenue and profit or loss of the acquiree included in the consolidated P&L since acquisition

- Pro-forma revenue and profit as if the acquisition had occurred on the first day of the period

- Goodwill expected to be deductible for tax purposes

Frequently Asked Questions

- What journal entry is made when a parent acquires a subsidiary?The parent debits Investment in Subsidiary at acquisition cost and credits Cash or other consideration paid. On consolidation, this investment is eliminated against the subsidiary’s equity, with goodwill or a bargain purchase gain recognised for any difference versus the fair value of net identifiable assets.

- How is goodwill calculated?Goodwill = Consideration Transferred + Fair Value of NCI + Fair Value of Previously Held Equity Interest − Fair Value of Net Identifiable Assets at acquisition date. If net assets exceed total consideration, the excess is a bargain purchase gain recognised in profit or loss.

- Is goodwill amortised under IFRS?No. Under IFRS 3 and IAS 36, goodwill is not amortised but must be tested for impairment at least annually, or more frequently if indicators exist. Any impairment loss is charged immediately to profit or loss and cannot be reversed in later periods.

- What is the difference between the full goodwill and partial goodwill methods?Under the full goodwill method, NCI is measured at fair value, so goodwill is attributed to both the parent and NCI. Under the partial (proportionate) method, goodwill is recognised only on the parent’s share and NCI is measured at its proportion of net identifiable assets. US GAAP mandates full goodwill; IFRS 3 permits both as a per-transaction policy choice.

- How are intercompany balances eliminated on consolidation?All intercompany receivables/payables, revenues and expenses, and unrealised profits on transferred assets must be fully eliminated. Where the subsidiary sold goods to the parent, any unrealised profit in closing inventory (PURP) is eliminated and if the subsidiary is the seller, the NCI’s share of the adjustment is also deducted from NCI equity.

- Can acquisition costs be capitalised into goodwill?No. Both IFRS 3 (para 53) and ASC 805 require that acquisition-related costs; legal fees, due diligence, advisory be expensed as incurred. They cannot be added to the cost of investment or included in goodwill.

Key Takeaways – Accounting Entries for Acquisition of Subsidiary

- The acquisition method is mandatory under both IFRS 3 and ASC 805; the pooling-of-interests method is no longer permitted.

- In the parent’s separate books, an investment is simply recorded at cost (Dr Investment / Cr Cash).

- On consolidation, the investment is eliminated against the subsidiary’s equity, with goodwill recognised for any excess consideration over net FV assets.

- All subsidiary assets and liabilities are remeasured to fair value at the acquisition date, including previously unrecognised intangibles.

- Goodwill is not amortised, it is subject to annual impairment testing and any write-down is permanent.

- Acquisition costs (legal, advisory) must always be expensed, never capitalised.

- NCI can be measured at fair value (full goodwill) or proportionate share under IFRS; US GAAP mandates fair value only.

- All intercompany transactions, balances, and unrealised profits must be eliminated in full on consolidation.

(Qualified) Chartered Accountant – ICAP

Master of Commerce – HEC, Pakistan

Bachelor of Accounting (Honours) – AeU, Malaysia