IFRIC 1 applies to changes in the measurement of any existing ‘decommissioning, restoration or similar liability’ that is both:

- recognized as part of the cost of PPE under IAS 16 or as part of the cost of a right of use (RoU) asset as per IFRS 16; and

- recognized as liability under IAS 37.

IFRS Interpretations · IFRIC 1 · ASC Analogues

Changes in Decommissioning,

Restoration & Similar Liabilities

A practitioner’s guide to accounting for revisions in cost estimates, discount rates, and risk adjustments under IAS 16, IAS 37, and IFRIC 1

This guide has been authored by Jhanzayb (ACA), a Qualified Chartered Accountant with specialist expertise in IFRS financial reporting, provisions accounting, and asset decommissioning obligations. The content reflects current IASB guidance and professional practice as recognised under IAS 37 and IAS 16. For full credentials and areas of expertise, visit the author profile page.

Quick Reference

- IssuedMay 2004

- Effective1 Sep 2004

- Key StandardIAS 37

- RelatedIAS 16, IAS 36

- Change typeEstimate (IAS 8)

- RetrospectiveNo

What Is IFRIC 1?

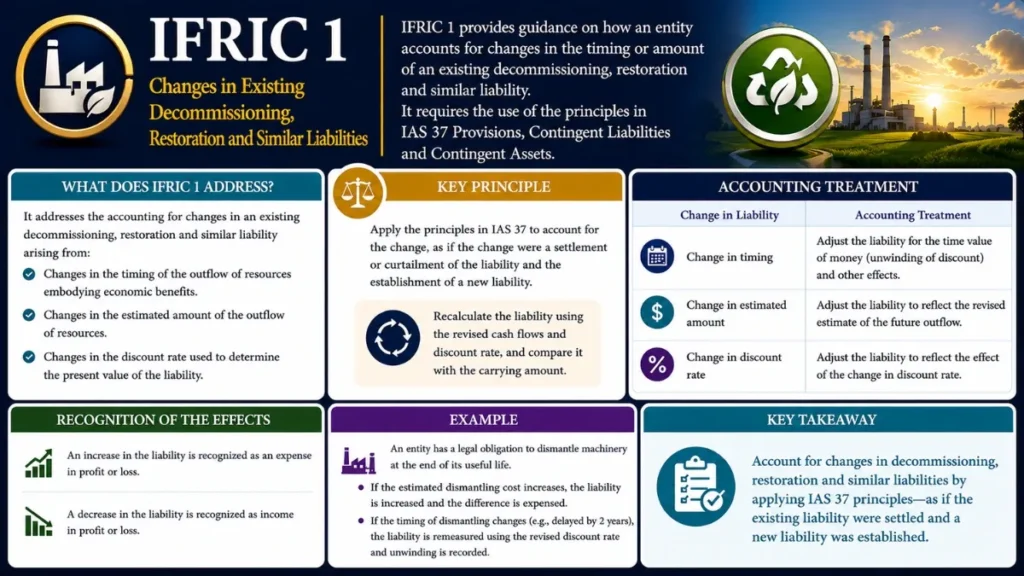

IFRIC 1 issued by the International Accounting Standards Board (IASB) in May 2004 provides crucial guidance on how to account for changes in the measurement of an existing decommissioning, restoration, or similar liability that has been included in the cost of an asset under IAS 16 Property, Plant and Equipment or IAS 2 Inventories.

When an entity holds a legal or constructive obligation to decommission an asset, restore a site, or perform similar remediation work, it must recognise a provision under IAS 37. That provision is simultaneously capitalised as part of the cost of the related asset. Over time, however, the estimated cash outflows change due to revisions in the scope of work, inflation, technology improvements, updated regulatory requirements, or fluctuations in the discount rate. Without specific guidance, entities might handle such changes inconsistently, either expensing them immediately or capitalising them in ways that distort asset carrying amounts.

IFRIC 1 resolves this ambiguity by prescribing a clear, consistent treatment that links changes in the liability directly to the carrying amount of the related asset and, where the asset is already fully depreciated, to profit or loss.

IFRIC 1 applies to changes in the measurement of an existing decommissioning or restoration provision recognised under IAS 37. It does not address the initial recognition of such provisions, which is governed by IAS 37 and IAS 16.16(c).

Background and Purpose

Decommissioning liabilities arise across multiple industries: oil & gas (plugging and abandonment of wells, platform removal), mining (site rehabilitation), nuclear power (decommissioning reactors), and telecommunications (removal of towers and cables). These obligations can span decades and involve enormous uncertainty in both timing and amount.

The Pre-IFRIC 1 Problem

Before IFRIC 1 was issued in May 2004, the interaction between IAS 37 and IAS 16 left a significant gap. Both standards acknowledged that a provision may initially be capitalised as part of PP&E cost but neither explicitly addressed what to do when that provision changes in subsequent periods. Practice diverged: some entities charged changes to profit or loss; others adjusted the asset cost; others recorded the effects in other comprehensive income. IFRIC 1 standardised this treatment globally.

Relationship to Other Standards

| Standard | Role in Decommissioning Accounting | IFRIC 1 Interaction |

|---|---|---|

| IAS 37 | Initial recognition and measurement of the provision; best estimate of settlement cost; discount rate selection | IFRIC 1 amends the provision in line with IAS 37 changes; the updated liability follows IAS 37 measurement rules |

| IAS 16 | Capitalisation of decommissioning cost into PP&E carrying amount; depreciation of that cost over asset life | IFRIC 1 adjusts the asset’s carrying amount (increasing or decreasing it) to match changes in the provision |

| IAS 36 | Impairment testing; recoverable amount of PP&E | An IFRIC 1 increase to asset carrying amount may trigger an IAS 36 impairment review |

| IAS 8 | Accounting policies, estimates, and errors | Changes under IFRIC 1 are changes in estimate (prospective treatment) not changes in policy |

| IFRS 1 | First-time adoption of IFRS | Contains a specific exemption allowing first-time adopters to measure IFRIC 1 amounts at transition date rather than retrospectively |

Scope of IFRIC 1

IFRIC 1 applies when all three of the following conditions are met:

- 01Existing provision recognised A decommissioning, restoration, or similar liability has already been recognised under IAS 37 in a prior period.

- 02Capitalised as part of asset cost The provision was included in the cost of the related item of PP&E (IAS 16.16(c)) or in the cost of inventory (IAS 2).

- 03A change in measurement arises There is a change in the estimated outflows required to settle the obligation, or a change in the current discount rate, or a change in the risk adjustment included in the measurement.

IFRIC 1 does not address changes arising from the mere unwinding of the discount (interest accretion on the provision). Unwinding is treated as a borrowing cost under IAS 23 or as finance cost not as a change in estimate under IFRIC 1. IFRIC 1 is also silent on provisions not related to PP&E (e.g., standalone legal provisions).

IFRIC 1 Accounting Treatment Explained

The principle underlying IFRIC 1 is straightforward: changes in the liability are capitalised into the related asset’s cost, subject to a ceiling (the asset’s carrying amount cannot be negative) and with any excess recognised in profit or loss.

“The amount deducted from or added to the cost of the asset should not exceed the carrying amount of the asset. If a decrease in the liability exceeds the carrying amount of the asset, the excess shall be recognised immediately in profit or loss.” — IFRIC 1, Paragraph 5

Assets Carried Under the Cost Model

When the related PP&E item is carried at cost (the most common approach), the treatment is:

- 01Remeasure the provision Apply the revised best estimate of future cash flows and, if applicable, the new pre-tax discount rate per IAS 37.

- 02Adjust the asset’s cost Add (increase) or deduct (decrease) the change in the provision from the carrying amount of the related asset. This restates the historical cost component attributable to decommissioning.

- 03Recalculate depreciation prospectively The adjusted cost is depreciated over the remaining useful life of the asset. No retrospective restatement of past depreciation is required (IAS 8 – change in estimate).

- 04Test for impairment if an increase Where the liability increases, conduct an IAS 36 impairment review to ensure the asset is not written up above its recoverable amount.

- 05Recognise excess in P&L if a decrease If the decrease in liability exceeds the asset’s carrying amount, immediately recognise the excess in profit or loss as a gain.

Assets Carried Under the Revaluation Model

When the PP&E item is carried at fair value (revaluation model under IAS 16.31), the treatment differs:

Decrease in Liability

- Recognised in Other Comprehensive Income (OCI)

- Increases the revaluation surplus in equity

- Exception: reverses a previous revaluation decrease previously charged to P&L, recognised in P&L as a gain

Increase in Liability

- Recognised as an expense in profit or loss

- Exception: reverses a previous revaluation surplus, reduces OCI / revaluation reserve in equity

- May trigger full IAS 16 revaluation of the class of assets

Under the revaluation model, the entity must also consider whether the change in liability would, in practice, trigger a new formal revaluation of the entire class of assets.

Summary: Cost Model vs Revaluation Model

| Event | Cost Model Treatment | Revaluation Model Treatment |

|---|---|---|

| Liability increases | Add to asset cost; depreciate prospectively; IAS 36 test | Charge to profit or loss (unless reversing prior OCI credit) |

| Liability decreases (within asset CA) | Deduct from asset cost; depreciate prospectively | Recognise in OCI; increase revaluation surplus |

| Liability decreases (excess over asset CA) | Excess immediately to profit or loss (gain) | Excess to profit or loss (gain) |

Measurement Requirements Under IAS 37

Understanding why the provision changes is essential to applying IFRIC 1 correctly. IAS 37 requires decommissioning provisions to be measured at the best estimate of the expenditure required to settle the present obligation, discounted when the time value of money is material.

Drivers of Change

| Driver | Description | Impact Direction |

|---|---|---|

| Revised cost estimates | Updated engineering studies, regulatory changes, technology cost deflation, inflation in labour/materials | Either way |

| Discount rate change | Movement in risk-free rates; change in entity-specific credit risk; updated risk adjustments | Rate up → liability down; Rate down → liability up |

| Timing revision | Asset life extended or shortened, changing the present value of cash flows | Either way |

| New legal requirements | New environmental legislation expands scope or cost of remediation | Typically increases liability |

| Risk adjustment | Changes to the probability-weighted estimate or risk premium included in the rate | Either way |

Discount Rate: A Critical Input

IAS 37 requires use of a pre-tax rate that reflects current market assessments of the time value of money and the risks specific to the liability. In practice, entities use one of two approaches:

Risk-Adjusted Rate Approach

- Uses undiscounted best-estimate cash flows

- Risk premium embedded in the discount rate

- Widely used in oil & gas sector

- Discount rate changes affect liability significantly

Expected-Value Approach

- Uses probability-weighted cash flows

- Discounted at risk-free or near risk-free rate

- More common in nuclear / utilities sector

- Risk captured in the cash flow estimate

Regardless of approach, any change in the discount rate or the probability-weighted cash flows triggers a remeasurement and therefore an IFRIC 1 adjustment. Entities must document their chosen methodology consistently and disclose it, as it materially affects the magnitude of IFRIC 1 adjustments.

IFRIC 1 Journal Entries and Illustrative Examples

Example 1 – Cost Model: Increase in Liability

Year 1: MinesCo installs a processing plant (useful life 20 years). Initial decommissioning provision recognised: $4,000,000 (present value). This amount is capitalised into PP&E and depreciated straight-line over 20 years. By Year 5, accumulated depreciation attributable to decommissioning component = $1,000,000; carrying amount of decommissioning component = $3,000,000.

Year 5 revision: New environmental regulations expand scope of remediation. Revised provision = $5,500,000. Increase = $1,500,000.

- Add $1,500,000 to the carrying amount of PP&E.

- New decommissioning component carrying amount: $3,000,000 + $1,500,000 = $4,500,000.

- Remaining life = 15 years. New annual depreciation on this component: $4,500,000 ÷ 15 = $300,000/year (vs. $200,000/year previously).

- Conduct IAS 36 impairment review of the cash-generating unit.

Example 2 – Cost Model: Decrease in Liability (No Excess)

Year 10: TowerCo reviews its telecom tower removal provision. Rising interest rates push the discount rate higher. Revised present value of provision drops by $800,000. Carrying amount of decommissioning component of PP&E at Year 10 = $2,200,000 (well above $800,000).

- Deduct $800,000 from PP&E carrying amount.

- No gain recognised in P&L (decrease is within carrying amount).

- Remaining useful life = 8 years. Revised annual depreciation recalculated prospectively.

Example 3 – Cost Model: Decrease Exceeding Asset Carrying Amount

Year 18: PipelineCo’s asset is nearly fully depreciated. Carrying amount of the decommissioning PP&E component = $120,000. A revised engineering study reduces the estimated decommissioning cost by $400,000 (present value).

- Deduct $120,000 from asset carrying amount (bringing it to nil, asset cannot go negative).

- Remaining $280,000 ($400,000 − $120,000): recognised immediately as a gain in profit or loss.

Example 4 – Revaluation Model: Decrease in Liability

Year 7: PowerCo carries nuclear plant under the revaluation model. Decommissioning provision decreases by $2,000,000 due to improved decommissioning technology. There is no prior revaluation decrease previously charged to P&L.

- Recognise $2,000,000 in OCI (increase in revaluation surplus in equity).

- No gain in profit or loss.

- Depreciation is not adjusted separately, the asset is carried at fair value reassessed at next revaluation date.

Disclosure Requirements

IFRIC 1 itself does not add extensive new disclosure requirements, it relies on disclosures mandated by the underlying standards. However, the interaction of standards creates a comprehensive disclosure framework:

Under IAS 37 – Provisions

- →Reconciliation of opening to closing provision balance (increases, releases, unwind of discount, effect of changes in discount rate)

- →Description of nature of the obligation and expected timing of outflows

- →Uncertainties affecting amount and timing; major assumptions regarding future events

- →Amount of expected reimbursement (if any)

Under IAS 16 – Property, Plant and Equipment

- →Reconciliation of PP&E carrying amounts, including additions and disposals arising from IFRIC 1 adjustments

- →Capitalised decommissioning costs included in cost of PP&E (for assets measured at cost)

- →Useful lives and depreciation methods used

Recommended Best Practice Disclosures

- The discount rate(s) used and sensitivity analysis showing the effect of a 1% change in discount rate

- The inflation rate applied to nominal future cash flows

- The expected timing of major decommissioning expenditures

- Whether the cost model or revaluation model is applied

- Amounts of gains or losses recognised in P&L under IFRIC 1 in the period

- Nature and amount of any changes arising from new or amended regulations

Common Practical Issues in Applying IFRIC 1

1. Unitisation of PP&E

Many entities treat an entire facility (e.g., an oil platform) as a single asset. However, a decommissioning liability may attach to individual components. Applying IFRIC 1 rigorously may require tracking the decommissioning component separately within the PP&E roll-forward, sometimes referred to as component accounting. Entities that have not implemented component accounting may struggle to isolate the decommissioning cost component of the asset’s carrying amount.

2. Fully Depreciated Assets with Remaining Obligations

Where an asset has been fully depreciated but the decommissioning obligation still exists, any increase in the provision must be recognised directly in profit or loss as an expense. There is no asset carrying amount to absorb the increase. This scenario arises frequently for legacy assets in mining and oil & gas. Conversely, a decrease in the provision produces an immediate gain in P&L.

3. Assets Approaching End of Life

As an asset nears the end of its useful life, the depreciation base for the decommissioning component diminishes. Even modest IFRIC 1 increases can push the asset carrying amount towards the IAS 36 ceiling of recoverable amount, triggering impairment. Practitioners must be alert to this interaction and model the recoverable amount alongside the provision estimate.

4. Determining the Appropriate Discount Rate

IAS 37 requires a pre-tax risk-free rate with adjustments for liability-specific risks. In practice, entities use government bond yields of appropriate maturity, matched to the expected timing of decommissioning. Where decommissioning will not occur for 30–50 years, there may be limited market data for ultra-long maturities. Entities must exercise significant judgement and document their rate-setting methodology.

5. Change in Estimate vs. Change in Policy

All IFRIC 1 adjustments are treated as changes in accounting estimate under IAS 8 and applied prospectively. There is no restatement of comparative periods. However, if an entity changes the method of estimating the liability (e.g., switching from a single best-estimate to an expected-value probability-weighted approach), this may constitute a change in accounting policy, requiring retrospective application under IAS 8.

6. Joint Operations and Decommissioning

In jointly operated assets (common in oil & gas), each operator recognises its proportionate share of the decommissioning liability and applies IFRIC 1 to its share. If the operator’s interest changes through acquisition or disposal, the IFRIC 1 adjustments follow the change in interest.

Industry Applications of IFRIC 1

| Industry | Typical Obligations | Key IFRIC 1 Considerations |

|---|---|---|

| Oil & Gas | Well plugging & abandonment; platform removal; pipeline decommissioning; onshore facility restoration | Highly material provisions; long time horizons (20–40 years); significant exposure to discount rate changes; Asset Retirement Obligation tracking per field |

| Mining | Mine closure; tailings dam rehabilitation; heap leach pad remediation; acid mine drainage treatment | Evolving regulatory requirements frequently revise cost estimates; bond/guarantee requirements can signal quantum of liability |

| Nuclear Power | Reactor decommissioning; spent fuel management; site remediation | Extremely long time horizons (50-100 years); state involvement; use of nuclear decommissioning funds may reduce net liability |

| Utilities / Telecoms | Tower removal; cable extraction; substation decommissioning | Large number of relatively small obligations; portfolio approach to estimation; active second-hand equipment markets affect net cost |

| Retail / Property | Leasehold dilapidations; store fit-out reinstatement obligations | The same IFRIC 1 principles apply; ROU asset (IFRS 16) may be the related asset rather than owned PP&E |

First-Time Adoption Exemption

IFRS 1 First-time Adoption of International Financial Reporting Standards includes a specific optional exemption in Appendix C that addresses the retrospective application of IFRIC 1. Without this exemption, a first-time adopter would theoretically need to reconstruct all historical IFRIC 1 adjustments since the asset was first recognised, an onerous and sometimes impossible task.

How the Exemption Works

Under the IFRS 1 exemption (IFRIC 1, Appendix C), a first-time adopter may elect to:

- 01Measure the liability at transition date Estimate the liability at the IFRS transition date using the current best estimate and current discount rate.

- 02Estimate the historical cost component Estimate what the capitalised decommissioning cost would have been at the date the liability first arose by discounting the liability back to that date using a historical estimate of the discount rate.

- 03Calculate accumulated depreciation Compute depreciation on that estimated historical amount up to the transition date, applying the entity’s IFRS depreciation policy.

This exemption significantly reduces the burden on first-time adopters with long-standing decommissioning obligations, while still producing a reasonable approximation of the IFRIC 1 carrying amounts.

Frequently Asked Questions

Key Takeaways From IFRIC 1

What IFRIC 1 Establishes

- Changes in decommissioning provisions adjust the related asset’s carrying amount

- Cost model: adjustments change asset cost, depreciated prospectively

- Revaluation model: increases to P&L; decreases to OCI

- Excess of decrease over asset carrying amount → P&L gain

- All changes treated as estimates (prospective under IAS 8)

What Practitioners Must Remember

- Unwinding of discount is finance cost, not IFRIC 1

- Fully depreciated assets absorb no further increases → direct P&L

- IAS 36 impairment review triggered by liability increases

- Significant judgement in discount rate selection and documentation

- IFRS 1 exemption available for first-time adopters

IFRIC 1 ensures that the economic burden of revised decommissioning estimates is reflected in the asset’s carrying amount and ultimately in the depreciation charge rather than creating distortions through immediate income statement recognition. — Principle Underlying IFRIC 1

(Qualified) Chartered Accountant – ICAP

Master of Commerce – HEC, Pakistan

Bachelor of Accounting (Honours) – AeU, Malaysia