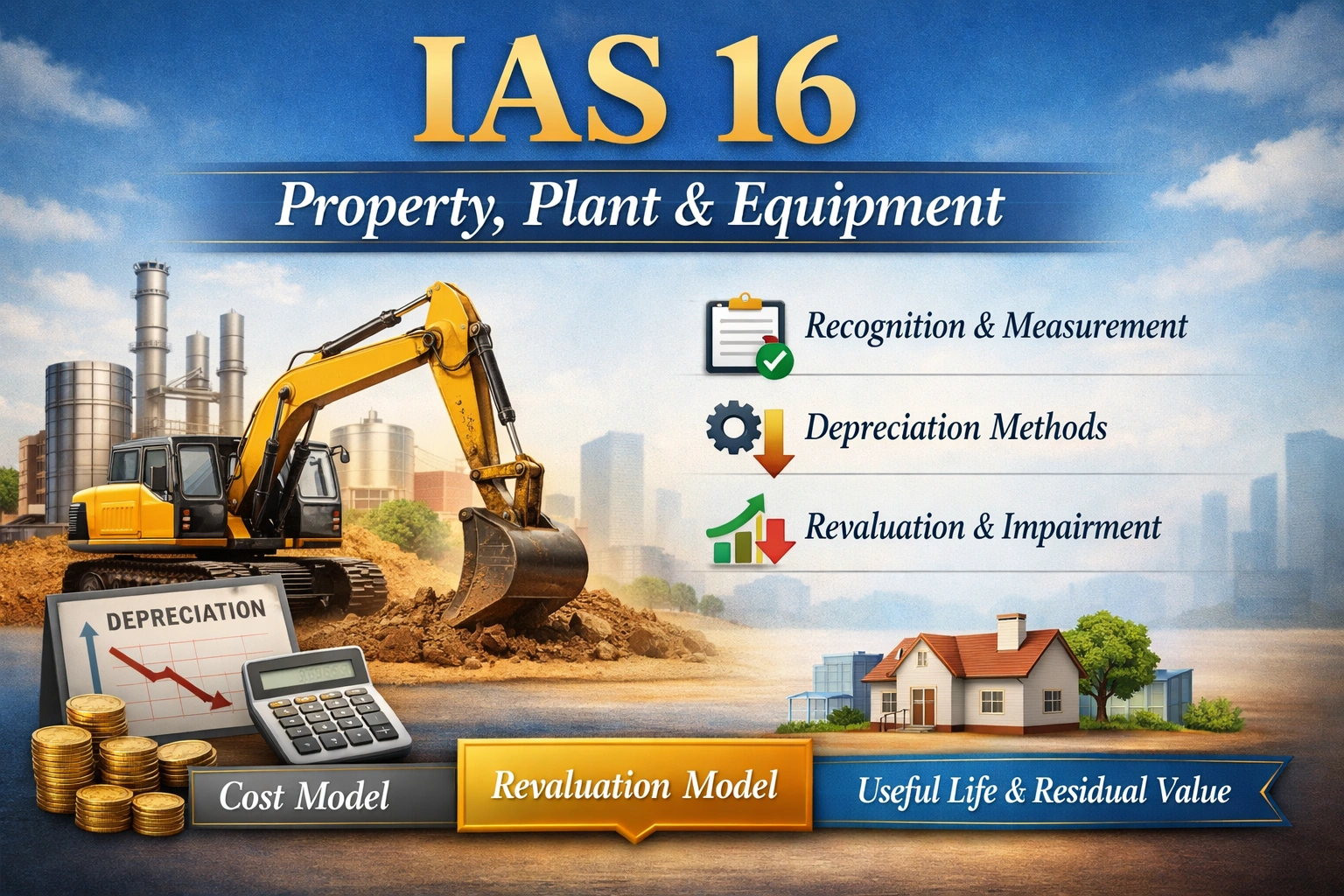

IAS 16 – Property, Plant and Equipment

IAS 16 STATES that Property, plant and equipment is Initially Measured at its cost, Subsequently Measured either using a ‘cost or revaluation model‘, and depreciated so that its depreciable amount is allocated on a systematic basis over its useful life. International Accounting Standard 16 📘 IAS 16 🌐 IFRS · IASB … Read More