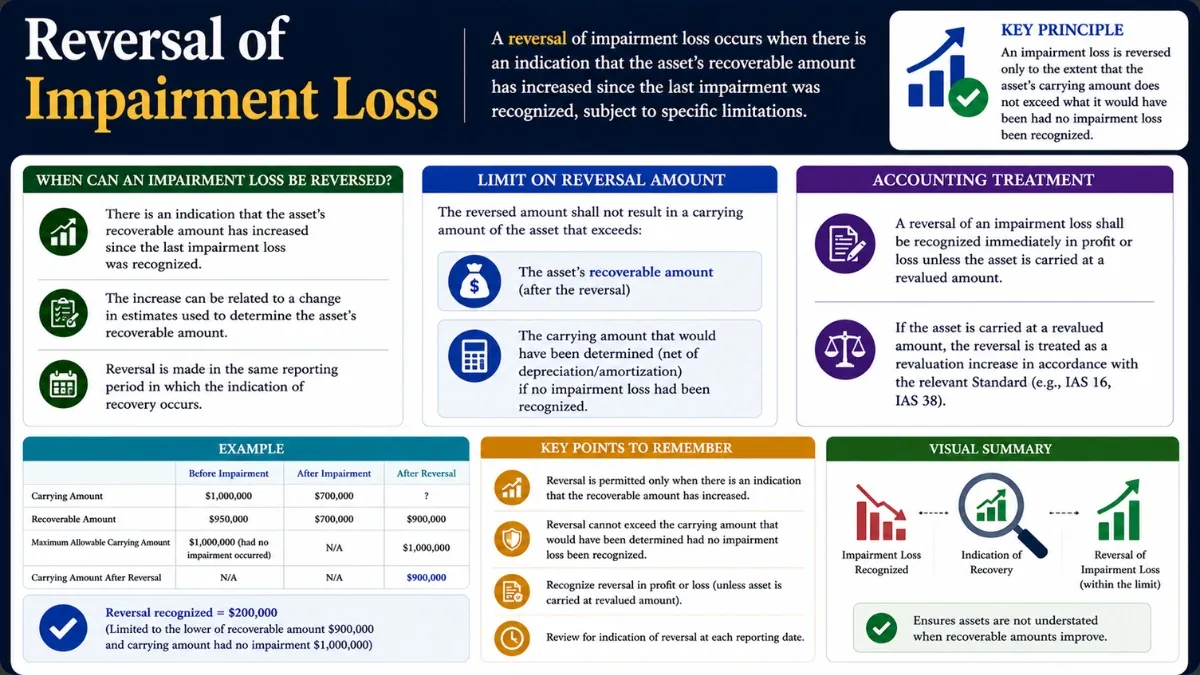

Reversal of Impairment Loss Explained with Example (IAS 36)

Reversal of impairment loss is increasing the value of a previously impaired asset when there is a change in circumstances indicating that the impairment loss is no longer necessary. Home Accounting Reversal of Impairment Loss IAS 36 – Impairment of Assets · Reference Guide Reversal of Impairment Loss When assets … Read More