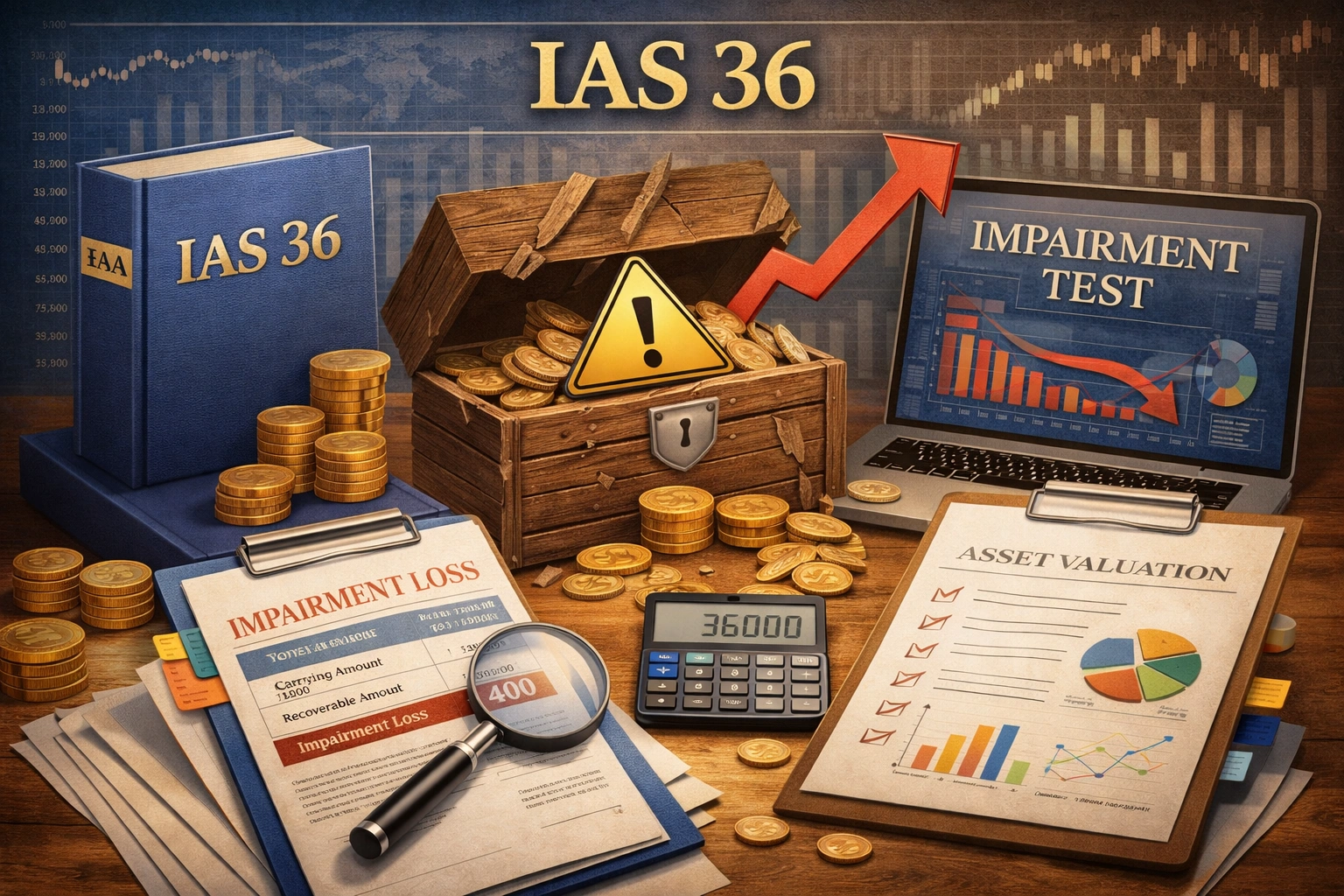

Reversal of Impairment Loss | IAS 36

Reversal of Impairment Loss is INCREASING the value of a previously Impaired asset when there is a change in circumstances indicating that the ‘Impairment Loss’ is NO longer necessary. IAS 36 · IFRS · Financial Reporting Table of Contents What Is Reversal of Impairment Loss? Conditions for Reversal The Reversal … Read More