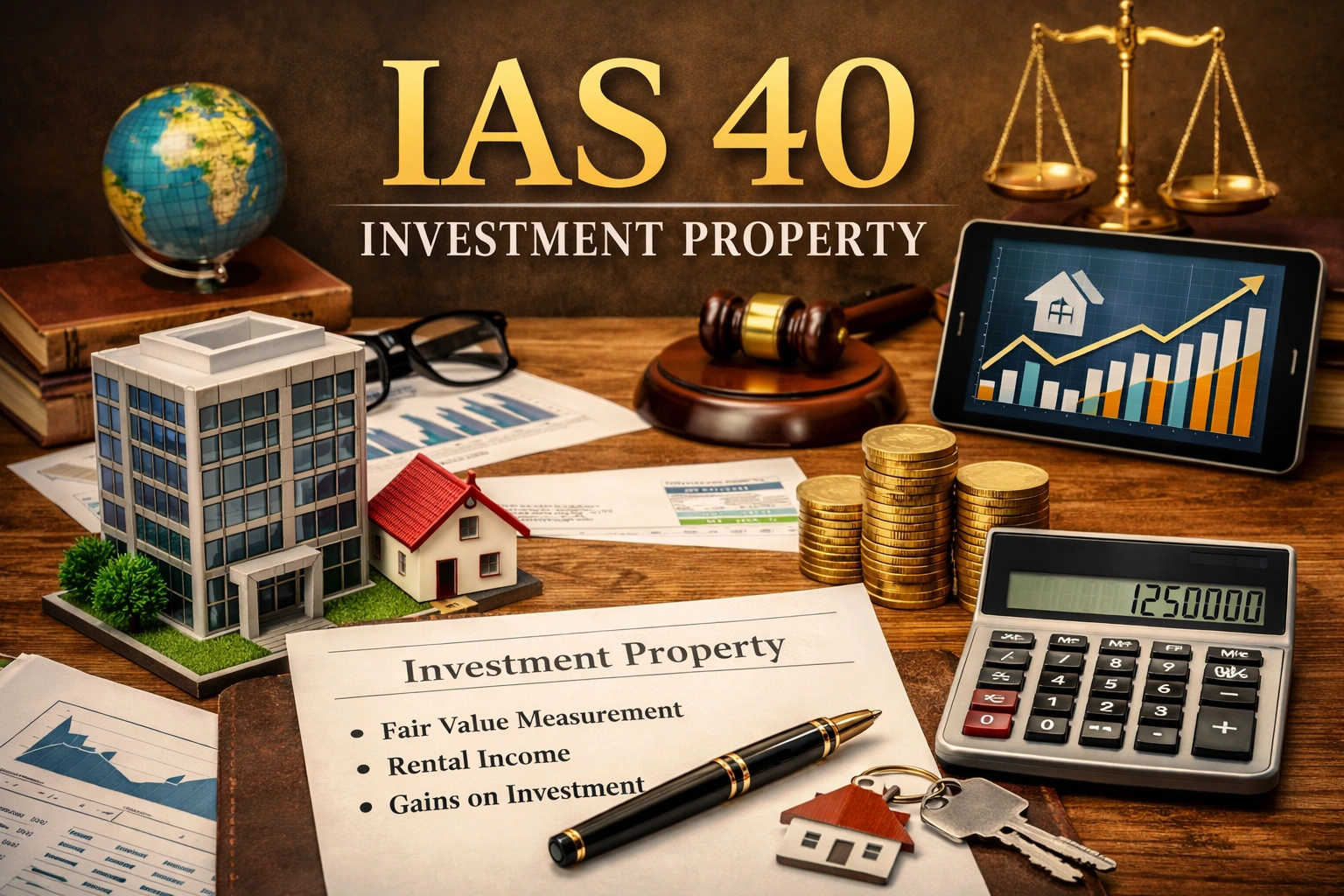

IAS 40 – Investment Property

The ‘OBJECTIVE’ of IAS 40 is to prescribe the accounting treatment for Investment Property and related disclosure requirements. IFRS Standard Issued by: IASB Effective: 1 January 2005 Last Revised: 2016 Supersedes: IAS 25 📋 Table of Contents What is IAS 40? Objective & Core Principle Scope & Definitions Recognition Criteria Measurement: Fair … Read More